In This Issue:

- USDA June Supply/Demand Report Tightens Market

- Washington DC Update

- USPRA Social Media Campaign in China Kicks Off

|

|

USDA June Supply/Demand Report Tightens Market |

|

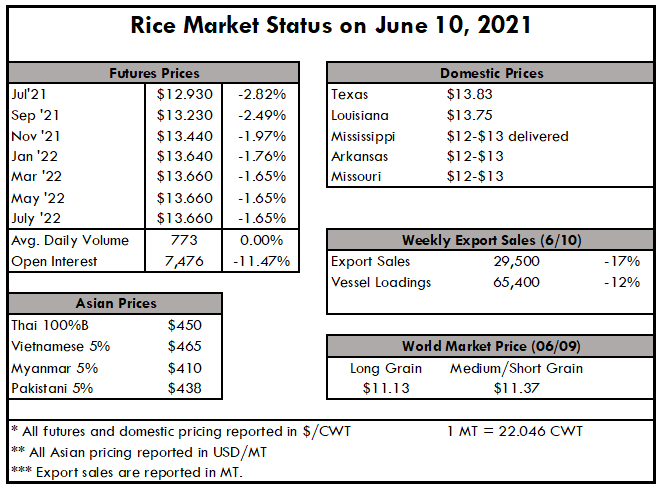

The June WASDE report was released by the USDA this week, and there were some notably bullish factors to discuss. First, the carryover stocks of USDA’s number came in at 30.1 million cwts, 3 million cwt below the trade estimate of 33.1 million cwt. A similar revision took place last year as well at the June report, in which the USDA June WASDE number came in at 28.8 million cwt, which was 3 million cwt below the trade estimate of 31.8 cwt. This is a bullish factor that will highlight the short-crop situation the long grain industry is moving into this year. The 2021/22 all rice beginning stocks are reduced 2.0 million cwt to 40.9 million, due to a combination of lower imports and higher exports for 2020/21. All rice 2020/21 imports are lowered 1.0 million cwt to 34.7 million on reduced volumes from Asia in recent months. The 2021/22 all rice season-average farm price is unchanged at $14.20 per cwt, compared to $13.90 for 2020/21, which is also unchanged this month.

For medium grain, the USDA shaved 500,000 cwts from the balance sheet on reduced demand outside of the Northeast Asian region. Ultimately, the USDA will likely be forced to lower exports a little further once the actual acre situation comes to light. Although the USDA currently forecasts ending stocks to reach a 3-year high, no one in the medium-grain industry anticipates a similar outcome on account of the drought in California.

The market itself remains fairly dormant, with no new noteworthy milled business on the horizon. Mexico has been a steady paddy customer, but business from Iraq or Haiti is still the shot-in-the-arm the market needs to ignite any cash prices on the ground as well. Planting is essentially complete across all rice-producing states and is progressing as would be expected with the wet weather in Louisiana, and the dry weather in CA. As a whole, the industry is pegged at 75% in the Good to Excellent condition for rice, and only 25% in the Fair to Poor categories.

Export sales and shipments, reported this week ending June 3 showed weaker sales but larger exports. Sales of 29,500 MT were up 21 percent from the previous week, but down 36 percent from the prior 4-week average. Increases primarily for Haiti (15,200 MT), Mexico (6,400 MT), Honduras (5,100 MT), Canada (1,400 MT), and Belgium (400 MT), were offset by reductions for Costa Rica (100 MT). Exports of 65,400 MT were up 92 percent from the previous week and 27 percent from the prior 4-week average. The destinations were primarily to Mexico (25,200 MT), Costa Rica (17,400 MT), Haiti (15,700 MT), Japan (2,200 MT), and Canada (1,900 MT).

In Asia, it’s a similar story this week with Thai exports waning based on high freight rates and the Thai Bhat strengthening against the US Dollar. Viet prices are still higher than Thai prices though, and despite that disparity, is still capturing the lion’s share of the Philippine business. However, there is speculation that this may be changing as the purchasing arm for the Philippine government will be sourcing cheaper rice, which points directly to India. The Philippines is expected to be the world’s second-largest rice importer this year, falling in behind China who is once again, projected to be the largest. The FAO does project that both global rice production and utilization will reach new peaks in the coming year, as countries seek to become more self-sufficient as well as find ways to fill the demand for what appears to be insatiable Chinese demand.

Despite the bullish revisions to the long grain balance sheet, rice futures edged lower this week. The nearby contract lost more than $0.30 per cwt from the beginning of the week. Average open interest was up down 11% from last week while average volume was up 75%. Declining open interest with declining prices may suggest that the downtrend may continue longer or that the selling climax is right around the corner. Either way, the market can expect increased volatility in the days ahead.

|

|

WATERS OF THE US

On June 9, 2021, the Environmental Protection Agency and Department of the Army (the agencies) announced their intent to establish a new definition of “Waters of the United States.” The agencies are seeking to better protect vital water resources that support public health, environmental protection, agricultural activity, and economic growth. In addition, the Department of Justice is filing a motion requesting remand of the 2020 Navigable Waters Protection Rule (NWPR) in the District Court of Massachusetts today.

Executive Order 13990 on “Protecting Public Health and the Environment and Restoring Science to Tackle the Climate Crisis” directs EPA and the Army to review and, as appropriate and consistent with applicable law, take action to revise or replace the NWPR defining “Waters of the United States.” EPA and the Army have completed this review and determined that they have concerns with the NWPR, including that it is causing significant, ongoing, and irreversible environmental damage.

The agencies’ new regulatory effort will be guided by:

- Protecting water resources and our communities consistent with the Clean Water Act

- Considering the latest science and the effects of climate change on our waters

- Emphasizing effective implementation

- Reflecting the experience of landowners, the agricultural community that fuels and feeds the world, states, tribes, environmental organizations, and community organizations

The agencies intend to pursue a new rulemaking process to replace the NWPR with a durable definition of “waters of the United States.” In the interim, the NWPR is still in effect across the country. Further details of the agencies’ plans, including opportunities for public participation, will be conveyed in a forthcoming action later this summer.

This information is provided by the EPA and the Army Corps of Engineers regarding their intention to revise the definition of Waters of the US (WOTUS) rule issued in 2020.

It is not clear what changes to the current rule the agencies will be proposing. A new rulemaking process is intended. This announcement is associated with the agencies requesting courts that are currently confronting various legal challenges to the 2020 rule to remand the rule to the agencies for revision.

EU AG DOMESTIC SUPPORT--OVERVIEW AND COMPARISON TO US

The Report highlights several policy trends that have emerged in the EU and the United States, including the following:

Traditionally, the United States uses less overall trade-distorting support (OTDS) than the EU, although the EU has made substantial reductions in the volume of OTDS. Since 2011, OTDS outlays (as notified to the World Trade Organization [WTO]) for the EU and United States have been near parity.

In both the EU and the United States, support for less-distorting noncommodity-type programs (e.g., conservation, rural development, agroforestry, nutrition, and climate) has increased substantially.

When measured by producer subsidy equivalent (PSE) as a share of total gross farm receipts, support has been trending lower for both the EU and the United States. As of 2019, the EU’s share (19%) remained above the U.S. share (12%).

U.S. consumers have received net benefits from agriculture-based support programs (including domestic food aid), whereas EU consumers generally have transferred more support to agricultural producers than they have received in offsetting benefits—that is, the EU’s consumer subsidy estimate (CSE) is negative— although the net transfer has been declining over time as a share of gross farm receipts.

The report is intended to provide information to policy makers because the United States and the EU figure prominently in the development and use of global agricultural policy. Information comparing their farm support programs may be of interest to Congress as the United States considers reauthorization of the domestic farm bill by 2023 and engages in international trade negotiations.

|

|

USPRA Social Media Campaign in China Kicks Off |

|

The first post of U.S. rice on China’s top social media networks, WeChat and Weibo, went live last week. Social media platforms Weibo, China’s version of Twitter, and WeChat, with almost a billion monthly users, have become China’s top social media platforms. Implemented with USDA/FAS ATP program funding, USRPA manages official accounts on both platforms, allowing the U.S. rice industry to target China’s masses in a cost-effective manner, with the potential to achieve exposures in the millions. The account name is created with a catchy phrase in Chinese which literally means “Beautiful life originated from USA,” as the word "rice" is pronounced very similarly to “beautiful/good” in Mandarin.

Bi-weekly posts will continue for the rest of the year, which will entail key product characteristics, such as U.S. rice growing cycles, farming practices, health benefits, and applications as well as recipes to engage with potential consumers across China.

|

|

Central American Rice Farmers Fear Bankruptcy |

For the Central American Rice Federation, the bankruptcy of more than 62 thousand rice farmers in Central America and the Dominican Republic is imminent, due to the abolition of import tariffs, a measure that is part of the implementation of the DR-CAFTA Free Trade Agreement.

Representatives of the sector consider that if the commercial liberalization of rice cultivation continues, there will be an increase in unemployment and poverty in their agricultural areas, since more than 265,000 people depend directly on this crop and approximately 990,000 people indirectly, and foresee serious social, economic and political implications due to the effects of the Treaty.

|

|

|

|

|

Cornerstone

Trade Update

|

|

|

|

Food & Ag Regulatory

and Policy Roundup

|

|

|

|

|

The Colombian Ministry of Agriculture estimates economic losses of more than USD 700 million, due to road blockages and raw material shortages impacting the production and transport of food.

|

|

|

|

The ongoing economic impact of COVID-19 on Costa Rica has been significant. Consumers have been changing their shopping behavior in ways that could shape future purchasing patterns, there are good market prospects for U.S. consumer-oriented products, even with the pandemic situation. These U.S. products have seen impressive growth in recent years, reaching $295 million in U.S. exports to Costa Rica in 2020.

|

|

|

|

|

World Agricultural Production |

|

|

|

Grain: World Markets

and Trade

|

|

|

|

|

Regional Crop Reports

Despite Delays, Crop Making Progress Across All Regions

|

|

|

|

|

|

|

|

|

LSU AgCenter Acadia Parish and South Farm Rice Field Day |

|

|

|

Horizon Ag Field Tour, Richard Farms, LA

For info call: 866-237-6167

|

|

|

|

University of Arkansas Rice Agricultural Sustainability Virtual Field Trip |

|

|

|

Texas A&M AgriLife Field Day, Eagle Lake |

|

|

|

LSU AgCenter H. Rouse Caffey Rice Research Station Field Day |

|

|

|

Rice Market & Technology Convention |

|

|

|

Texas A&M AgriLife Field Day, Beaumont, TX |

|

|

|

LSU AgCenter Row Rice Field Day |

|

|

|

University of Arkansas Rice Field Day (tentative) |

|

|

|

University of Arkansas Rohwer Field Day |

|

|

|

California Rice Experiment Station Field Day (tentative) |

|

|

|

University of Arkansas Virtual Rice and Soybean Field Day |

|

25722 Kingsland Blvd.

Suite 203

Katy, TX 77494

p. (713) 974-7423

f. (713) 974-7696

e. info@usriceproducers.com

www.usriceproducers.org

|

|

We Value Your Input!

Send us updates, photos, questions or comments!

|

|

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender, religion, age, disability, political beliefs, or marital/family status. Persons with disabilities who require alternative means for communication of information (such as Braille, large print, sign language interpreter) should contact USRPA at 713-974-7423 |

|

|

|

|

|

|