Gordon T Long Research exclusively located at MATASII.com

|

|

UnderTheLens - MARCH 2022 |

UKRAINE PLACES FOCUS ON A FAILING US ENERGY POLICY DIRECTION

I had no problems with the US committing to Policy Goals of:

- US power grid to run on 100% clean energy by 2035,

- US to be a Net-Zero Carbon contributor by 2050 .

I did however have serious reservations of how this was to be met without massive financial sacrifice by an unsuspecting American consumer. This is because the implementation approach is blatantly irresponsible, naïve and unmanaged with regard to any sense of reality.

|

|

|

It is an academic ideal without any practical implementation planning created by politicians!

Unfortunately this concerning situation has been made worse by the Ukraine conflict. What I plan to share in this newsletter is:

NEWSLETTER HIGHLIGHTS - A Rapid Outline

- Why Economic Sanctions Will Not Deter Russia nor achieve meaningful results,

- Who actually gets hurt (besides innocent Ukrainians)?

- Russia's Achilles Heel is Energy,

- How Energy Policy Must Be Used to Stop Russian aggression and its aspersions for global power,

- Why US Climate Change Policy & its Unintended Consequences of US energy dependence is impeding the ending of the slaughter in the Ukraine,

- Global Credit Cracks are quickly becoming more than just cracks as further unintended consequences and contagion take hold!

- Why inaction & ineffective Western leadership will potentially lead to a US Recession in 2023 or earlier!

|

|

1- US SANCTIONS WILL NOT DETER RUSSIA

The US administration has chosen to restrict the US policy prescription for stopping Russian aggression and the slaughter in the Ukraine to the long term, and likely ineffective use of economic sanctions.

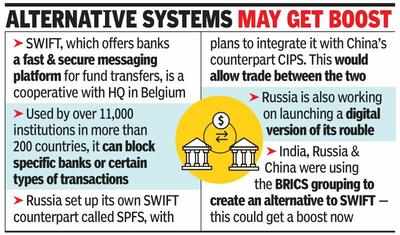

Russia, China, Iran and North Korea are well prepared for and fully expecting Sanctions to be the first policy reaction of the US. The use of sanctions has been used for over a decade as the US has effectively weaponized the US dollar through economic sanctions. The primary response of the US and G7 of removal of Russia from the SWIFT System is almost laughable, since the alternative Chinese CIPS System has quickly become a defacto alternative as a barrier to US economic sanctions.

SANCTIONS: A POTEMKIN FACADE

RUSSIA PREPARED FOR INCREASED SANCTIONS

- SPFS + CIPS.

- Russia sold ALL of its US Treasury Holdings in 2018.

- Russia moved its financial assets to Gold Reserves, Liquid Non-Dollar Short Term FX Holdings, Domestic holdings and aligned BRIC sovereign countries.

- Established European Dependency on Russian Energy Flows.

- Established trade relations with countries limiting trade exposure to the US and its Weaponization of the US Dollar.

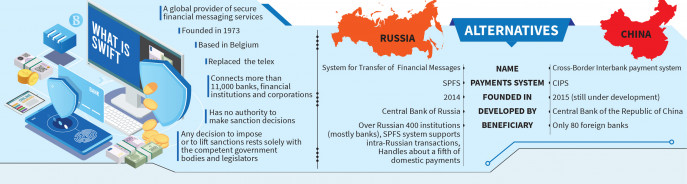

1- SPFS + CIPS versus SWIFT + CHIPS

The move by the US, the UK and the EU to cut some Russian banks' access to SWIFT accelerates the usage of China's rival CHIPS as a payments system for global trade and finance, and thereby reduce the international clout of SWIFT and the dollar.

SWIFT & CHIPS

- The Society for Worldwide Interbank Financial Telecommunication, or SWIFT, is a global messaging system that relays instructions from one bank to another. Based in Belgium and overseen by the central banks of a Group of 10 countries, SWIFT was established in 1973 connecting about 11,000 financial institutions around the world. It is not a payment system as such, but a secure platform to communicate cross-border payment instructions among banks. At present, SWIFT is used by 200 countries and territories.

- On the other hand, CHIPS or the Clearing House Interbank Payments System, is a 43-member private club of financial institutions. Members of CHIPS settle $1.8 trillion in claims every day with the help of a pre-funded account at the Federal Reserve. CHIPS is subject to US law.

|

|

CIPS & SPFS

CHINA'S CIPS

- In order to shrug off the power of CHIPS and SWIFT, China had established the Cross-Border Interbank Payment System, or CIPS, in 2015. CIPS settles international claims through the independent international yuan payment and clearing system. It has the potential to run its own messaging network, although it has been using the SWIFT as its communication channel since 2016.

- After its launch in 2015, 19 banks, including Standard Chartered, Deutsche Bank, HSBC and Citibank, had signed up for phase one of CIPS. In January 2022, CIPS had 1,280 users across 103 countries as reported by the South China Morning Post.

RUSSIA'S SPFS

- In 2014, after the invasion of Crimea, the Central Bank of Russia established its own messaging system called the System for Transfer of Financial Messages (SPFS). As of 2020, SPFS had over 400 registered financial institutions. Unlike the SWIFT which works 24/7, SPFS operations are conducted during operational hours. The system also limits the size of messages to 20 kilobytes.

When Russian banks were banned from using the US dollar-based SWIFT in response to the Ukraine invasion, Chinese media said the CIPS would work with SPFS to counter the restrictions.

|

|

|

"The SWIFT ban does not prevent Russia from continuing international trade and clearance, but makes SPFS or CIPS more viable as a new choice"

Dong Xiaopeng, Deputy Editor-in-Chief of China’s Securities Daily

|

|

|

|

“CIPS and SPFS systems are still smaller than SWIFT in terms of the number of participants and users, but over the long run, it is not impossible that the duo or one of them will grow into an important regional or even global infrastructure with considerable influence,”

Dong Xiaopeng, Deputy Editor-in-Chief of China’s Securities Daily

|

|

|

|

SANCTIONS STOP WITH CHINA'S CIPS WORKING WITH SPFS

WHERE IS CHINA'S SUPPORT OF THE ENTIRE WORLD'S OUTRAGE??

|

|

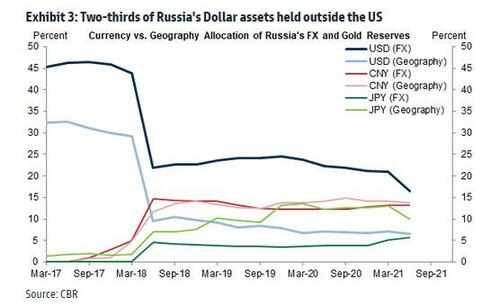

2- RUSSIA LEFT US$ FX RESERVES IN 2018 IN PREPARATION

3- GOLD RESERVES: Russia moved its financial assets to Gold Reserves, Liquid Non-Dollar Short Term FX Holdings, Domestic holdings and aligned BRIC sovereign countries.

As the graphic to the right illustrates, Russia after selling all its US Treasury Holdings in 2018 moved to Chinese and Euro holdings (held in select aligned countries).

4- RUSSIAN ENERGY DEPENDENCY: Russia has established European Dependency on Russian Energy Flows.

Over the past decade Russia has become the unquestioned dominant supplier of energy to Europe. Recent shortages from Wind and Solar have added to dependency as well as the decommissioning of Nuclear facilities in Germany.

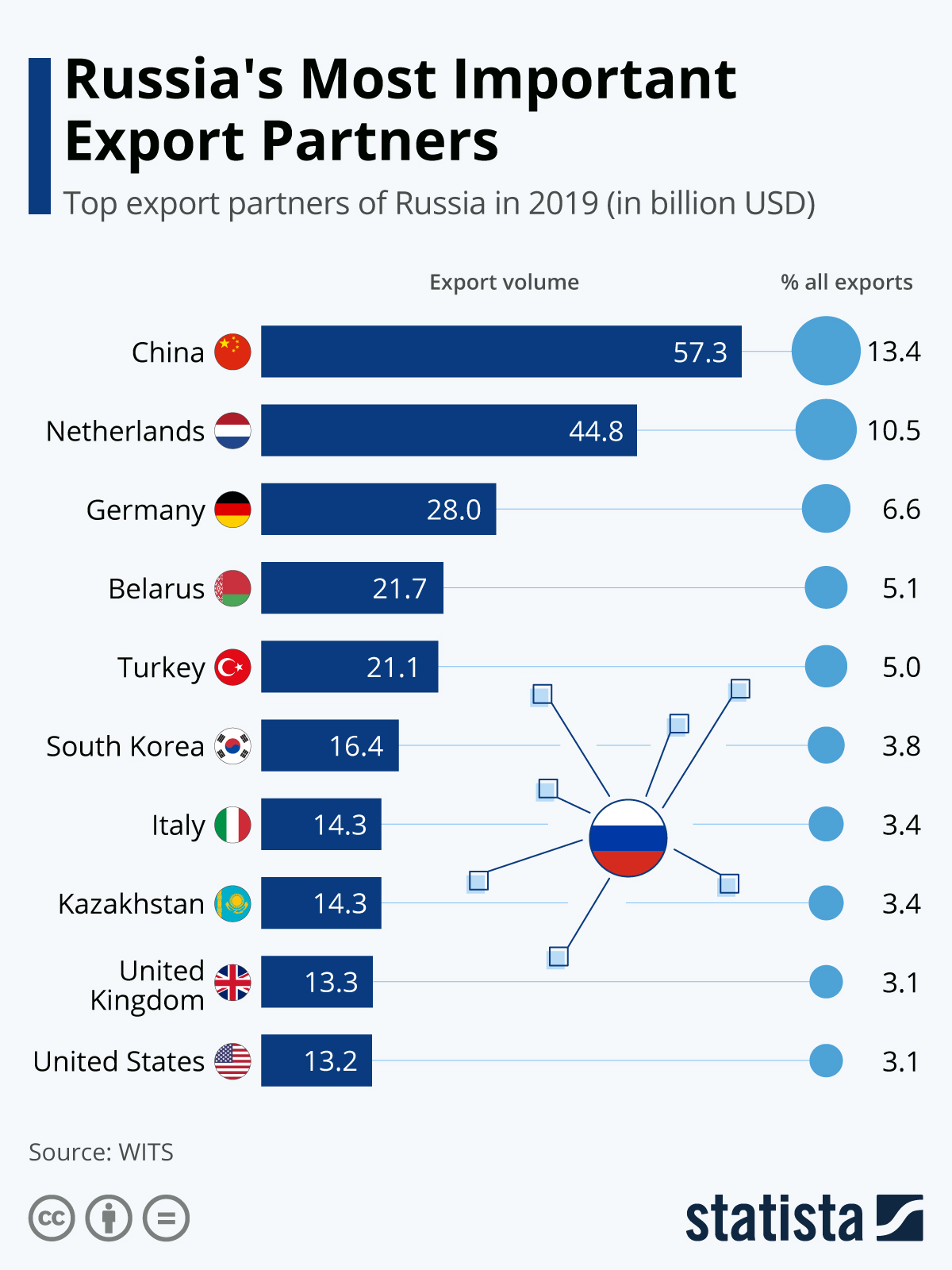

5- TRADE RELATIONS: Russia has established trade relations with countries limiting trade exposure to the US and its Weaponization of the US Dollar.

In our 2018 Thesis Paper - "De-Dollarization" we lay out the 13 major countries impacted by US sanctions who have moved away from US Dollar FX reserves. These have become major trading partners for Russia. Where Russia has large trading relations with non-aligned countries, it is because they are dependent on Russian products (Grains, Fertilizer, Minerals, etc.)

|

|

2- WHO ACTUALLY GETS HURT

There is no doubt Russia is being hurt but they were prepared for it and it is not as a result of Sanctions.

RUSSIA

- Russian Ruble has collapsed. Down over 50%.

- Russian Bonds have become almost "Worthless" Collateral.

- Russia basically is presently giving away their oil to find sufficient buyers. It is being forced to sell its oil at a $28.50 discount to Brent.

- Russian stock values have simply disappeared.

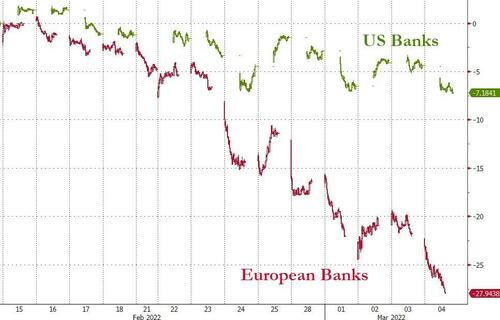

EUROPE & THE WORLD

- European Banks are in trouble. France and Italy are major holders of Russian Debt.

- National Average Gas prices at the pump have exploded higher to well over $4/gallon from $1.80 just over a year ago.

- Commodity prices both hard (miners) and soft (food) have exploded higher.

Effectively US Economic Sanctions are likely to only prove too little, too late! It is also likely that the world is going to be hurt more as a result of the fall out from the Sanctions (and their unintended consequences) and may be "shooting itself in the foot!" The dramatic rise in Commodity & Energy prices are cases in point.

|

|

RUSSIAN SANCTIONS MAY BACKFIRE & MATERIALLY IMPACT GLOBAL CREDIT

The News York Times is warning that US Sanctions against Russia could have far-reaching and indirect consequences, because Russia is a major exporter of staples like natural gas and wheat. It conducts business with companies and countries around the world. As middlemen, banks typically handle those transactions. Severe economic penalties could disrupt global trade flows if banks are forced to stop processing payments for goods and services going in and out of Russia, according to the Institute of International Finance, a trade association that represents global banks.

“The issue here is not just the immediate impact on the financial markets, but the fact that it’s almost impossible in the near term to disentangle Russia from global trade.

There is room for contagion.”

Elina Ribakova, Deputy Chief Economist, Institute of International Finance

Sanctions could also spread economic instability worldwide by raising prices for key commodities that Russia produces — including oil, gas, fertilizer and palladium — and spur inflation in countries that import those products, landing a fresh blow just as the world emerges from the pandemic. Russia’s own economy could be relatively protected from the full impact of sanctions. Its external debt and ties to other advanced economies have waned since the 2014 Crimea crisis, insulating its economy from efforts to cut it off from the global financial system, as noted by economists at Capital Economics noted. They predicted that the most likely sanctions measures could shave around 1 percent from Russia’s gross domestic product. The country’s economy has long been dominated by domestic lenders, which only grew in prominence after the 2014 sanctions. European banks, including Raiffeisen Bank and UniCredit Bank, account for most of the 6.3 percent of assets held by foreign lenders in Russia’s banking sector, while U.S. banks hold less than 1 percent, according to the Institute of International Finance.

“Russia has a more insulated and isolated economy today than it did a decade ago. This makes it less vulnerable to certain types of sanctions, but its increasing economic isolationism is hurting the country’s growth prospects in the long term.”

Clay Lowery, Executive Vice President, Institute of International Finance

|

|

3- RUSSIA'S ACHILLES HEEL: ENERGY EXPORT REVENUE

RUSSIA IS TURNING ITS WEAKNESS INTO ITS DEFENSIVE

The Russian economy is heavily reliant on energy exports for the financing of its economy.

The EU is heavily reliant on Russian oil and gas. The European Union imports about 40% of its natural gas from Russia and 25% of its oil. Europe is reliant on gas to heat homes, generate electricity and supply industries like fertilizer producers.

Russia is the world's second largest gas producer, after the United States, producing 761 billion cubic meters in 2021, or 18% of the world's gas output.

Russia was the largest supplier of both petroleum oils and natural gas to the EU last year. Total imports of crude oil equaled 440 Mtoe. Much of the oil imported to the European Union is refined into products and then exported — and Russian oil accounted for more than 25 percent, at 113 Mtoe. The European Union is more dependent on imports for oil (69.8 percent of total E.U). In 2021 Russia was the largest exporter of oil and natural gas to the European Union.

In 2017, energy products accounted for around 60% of the EU's total imports from Russia. Russia also supplies a significant volume of fossil fuels to eastern and central Europe. For North Macedonia, Moldova, Bosnia and Herzegovina, Russia was the only source of natural gas supply in 2019. Among other European countries highly dependent on Russian gas were Finland and Latvia, where Russian imported gas occupied over 90 percent of the total in 2020.

The rising price of energy for oil and gas is only further aiding Russia and helping fund its aggression.

|

|

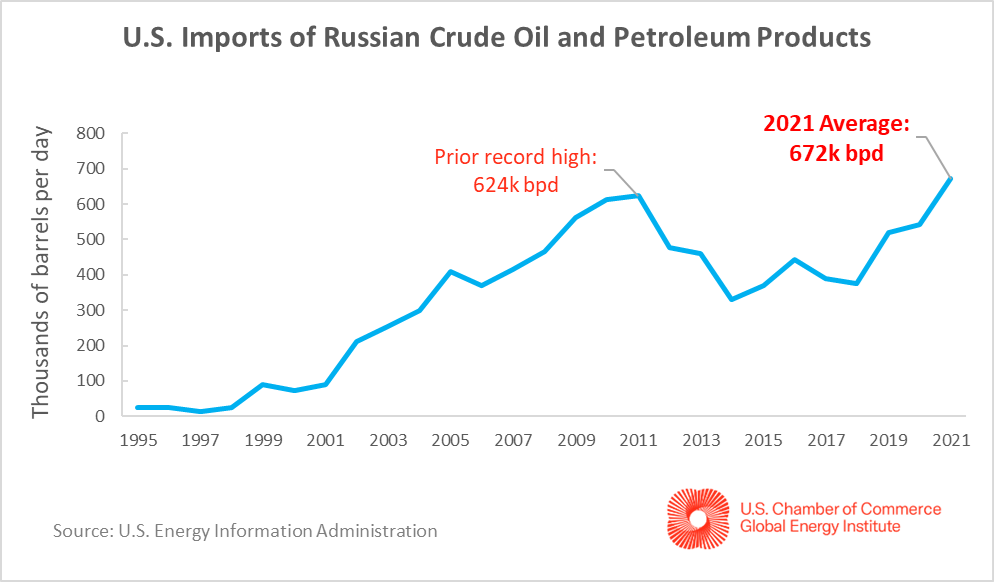

5- US ACHILLES HEEL: ENERGY IMPORT DEPENDENCE

The Energy Information Administration (EIA) tabulated U.S. energy consumption in 2019 and 2020, and determined that for both full years, counting all energy sources, we were energy independent. Even though U.S. energy production declined by 5% in 2020, energy consumption also declined by 3% as the pandemic impacted the economy. So, our energy independence was shrinking during the Covid pandemic. However, once the full year of 2021 has been accounted for, we will have lost our energy independence for the year. For example in 2021, the US imported an average of 209,000 barrels per day (bpd) of crude oil and 500,000 bpd of other petroleum products from Russia, according to the American Fuel and Petrochemical Manufacturers (AFPM) trade association.

The reasons for this are primarily the climate policies of the new administration. After merely one month in office, the Biden Administration had already had a profound impact on the oil and gas industry. Having promised to prioritize climate change on the campaign trail, President Biden took immediate action by signing executive orders aimed at everything from curbing emissions to environmental justice. While the Biden Administration’s 1) 60-day halt on new oil and gas leases on federal lands and 2) the cancellation of the Keystone XL Pipeline received the majority of press coverage, the administration’s actions also had both direct and indirect impacts on oil and gas companies. These actions include: 3) an order directing federal agencies to eliminate subsidies for fossil fuels, 4) reversing the Trump Administration’s rollback on methane regulations, and 5) staffing the SEC in preparation to mandate ESG and climate disclosures. While these changes primarily aim to reduce the nation’s carbon footprint, they will also add an additional layer of regulations for oil and gas operations. Since then the Biden Administration has been ruthless in implementing its 25 steps to "end the era of fossil fuel production, and #BuildBackFossilFree".

BIDEN’S EXECUTIVE ACTION BLUEPRINT

|

|

US MUST USE ENERGY AS BOTH A WEAPON AND FOR DEFENSE

US MUST IMMEDIATELY RESUME THE PATH IT WAS ON 15 MONTHS AGO

IN BECOMING A DOMINANT GLOBAL ENERGY SUPPLIER

|

|

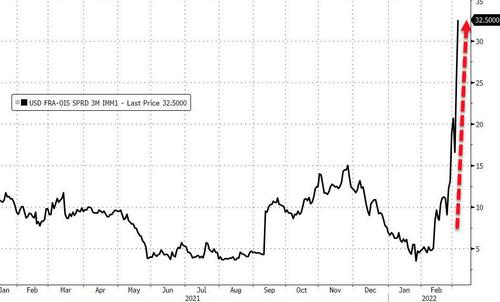

6- CREDIT CRACKS WORSENING

Further to our last two newsletters on Credit, serious s tresses are now starting to show in the financial system with FRA/OIS spreads blowing out (chart to the right).

- What is FRA? A Forward Rate Agreement (FRA) is a deal to swap future fixed interest payments for variable ones, or vice versa. The key rate for U.S. markets is the three-month London interbank offered rate, or Libor, in U.S. dollars. The benchmark is derived by major banks submitting rates based on transactions that are compiled to establish benchmark for five different currencies across seven different loan periods. Those benchmarks underpin interest rates on trillions of dollars of financial instruments and products from student and car loans to mortgages and credit cards.

- What is OIS? The Overnight Index Swap (OIS) rate is calculated from contracts in which investors swap fixed- and floating-rate cash flows. Some of the most commonly used swap rates relate to the Federal Reserve’s main interest-rate target which are regarded as proxies for where markets see U.S. central bank policy headed at various points in the future.

|

|

But why does the FRA-OIS spread matter in practice?

Well, it’s regarded as the markets’ measure of how expensive or cheap it will be for banks to borrow in the future, as shown by Libor, relative to a risk-free rate, the kind that’s paid by highly rated sovereign borrowers such as the U.S. government. The FRA-OIS spread therefore provides another snapshot of how the market is viewing credit conditions because of the fact that traders are betting on where Libor-OIS, its underlying spread, will be.

There are typically 3 reasons why it would blow out:

- The risk premium for uncertainty of US monetary policy,

- Recently elevated credit spreads (CDS) of banks, and

- Demand for funds in preparation for market stress.

While FRA-OIS exploded to 80bps in March 2020, at the peak of the Covid crash, it is currently at just half that level. Never before has funding stress been so high with a Fed balance sheet near $9 trillion and with some $1.6 trillion in the Fed's overnight reverse repo facility (i.e., excess liquidity). In other words, when adjusted for the statutory level of record liquidity in the market, which we don't need to tell subscribers is at an all time high, the FRA-OIS would almost certainly be at all time highs.

Whatever the reasons, a blow out in FRA/OIS means that dollar funding is becoming increasingly problematic. Absent a sharp tightening in the Libor-OIS and FRA-OIS spread, while bank credit concerns may not have been the catalyst for the sharp spike, it will be banks that are eventually impacted by what is increasingly emerging as an acute tightening in short-term funding markets and/or a global dollar shortage.

|

|

7- A US RECESSION

All of the above along with an ineffective political response to the Ukraine conflict.....

WILL PUSH THE US INTO RECESSION IN 2023 ..or earlier!

Not every recession is led by a 50% rise in crude.

But every 50% rise in crude has led a recession.

|

|

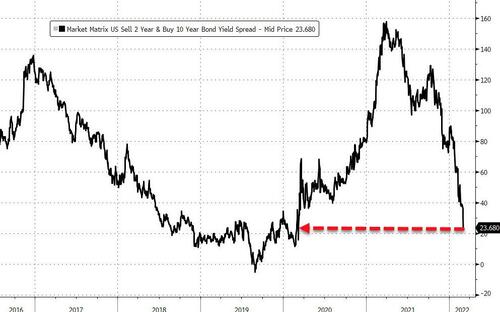

Yield Curve is now Flat and Nearing Inversion |

|

CURRENT MARKET PERSPECTIVE |

|

COMMODITIES SHOWN AS REAL VALUE |

|

ENERGY & COMMODITIES EXPLODING HIGHER!!

FEAR IS EVERYWHERE!

When fear is in the air, it is often times when the most money is made. As famed investor Warren Buffet says:

"Buy when there is blood in the street".

The question is: what is being overdone and what is justified!?

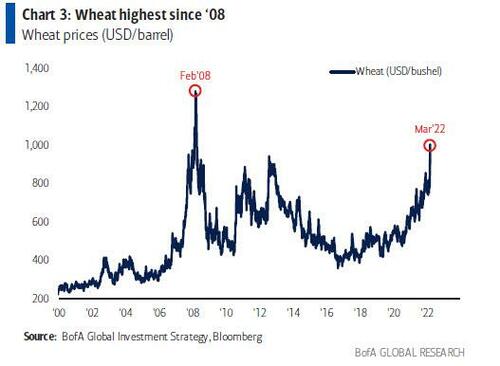

As shown below, grains, and specifically Wheat, were on a tear before the Ukraine conflict hit the news. Ukraine as a Wheat producer and Russia as a Wheat exporter are only going to exacerbate an already bad situation. In addition, Russia is a primary supplier of Fertilizer which is soon to be in further short supply for farmers!

Often the time then is to accumulate on pull-backs.

|

|

FOOD RPICES ARE RISING BECAUSE OF UNDERLYING SHORTAGES

This was happening before Ukraine was even a news item -

WHICH MAKES MATTERS EVEN WORSE!!!

|

|

YOUR DESK TOP / TABLET / PHONE ANNOTATED CHART

NOTE: Any Problems with this Chart: E-Mail lcmgroupe2@comcast.net

|

|

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

|

|

MATASII'S STRATEGIC INVESTMENT INSIGHTS |

|

2020 VIDEOS OUTLINING THE COMING RISE IN INFLATION & COMMODITY PRICES |

|

UnderTheLens - MARCH 2022 |

|

RELEASED - 02-23-22

VIDEO: 18 Minutes with 50 supporting slides.

|

|

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES |

|

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

|

|

The Most Insightful Macro Analytics On The Web |

|

PO Box 1224,

Norton, MA 02766

(508) 285 2213

|

|

|

|

|

|

|

|