|

Greetings!

February homes sales in Metro Vancouver continued the recent slower than average trend with a volume of sales 10% lower than February 2025 and 28.7% below the 10 year seasonal average.

The total home supply in Metro Vancouver in February 2026 is up 6.3% over February 2025 and that is 37% above the 10 year seasonal average.

These Metro Vancouver stats get a lot of press and are distinct from the west side market stats but we usually face similar trends here on the west side.

Westside home sales, when compared to the 10-year averages, are down by 18% for detached homes, down 33% for apartments and down by 8% for townhomes.

Compared to the 10-year average, supply is up 8% for Westside detached homes, while apartment supply is up 23%, and townhomes are up 56%.

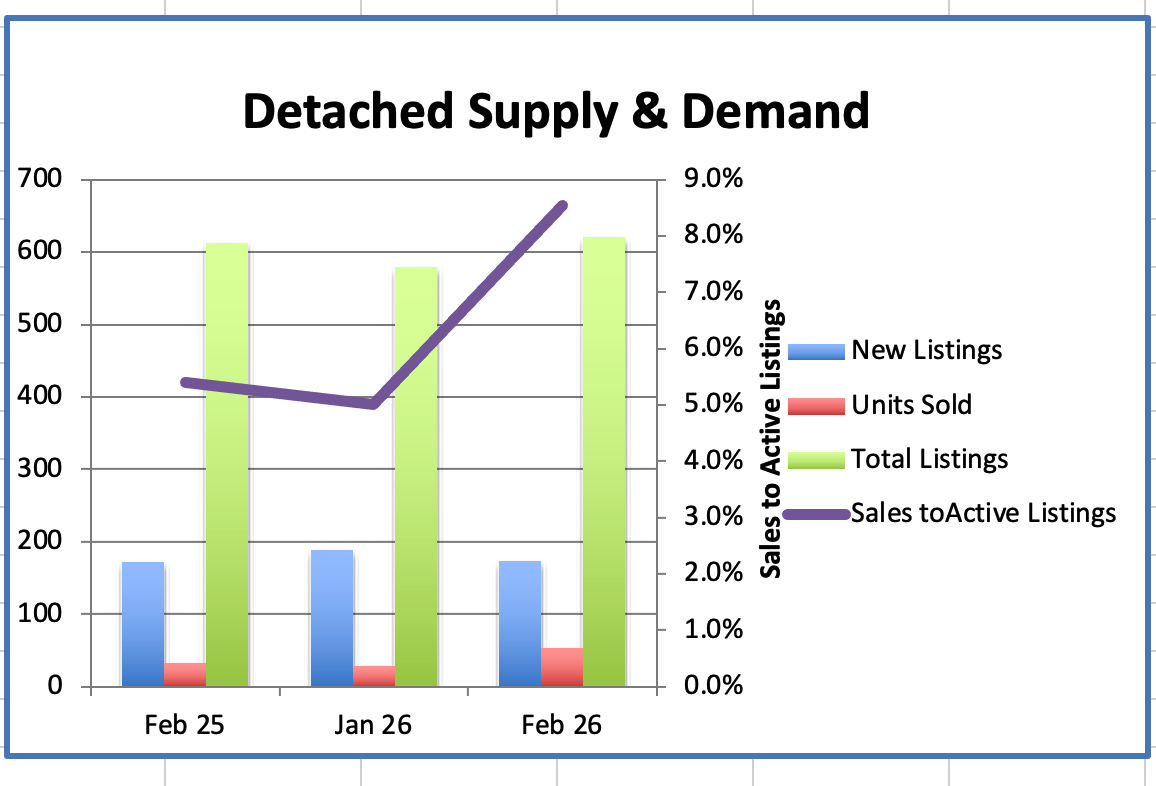

We had 53 Westside Detached home sales in February 2026, up 60%, compared to 33 sales in February 2025.

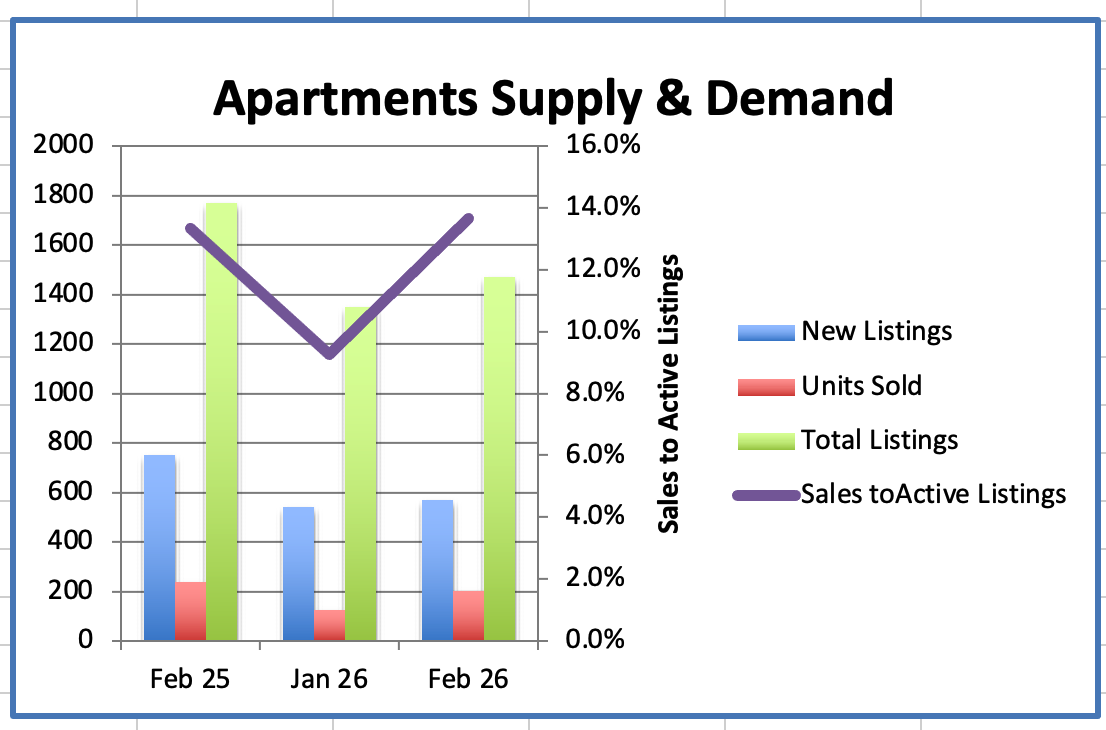

We had 201 Westside Apartment sales in February 2026, down 15% compared to 236 sales in February 2025.

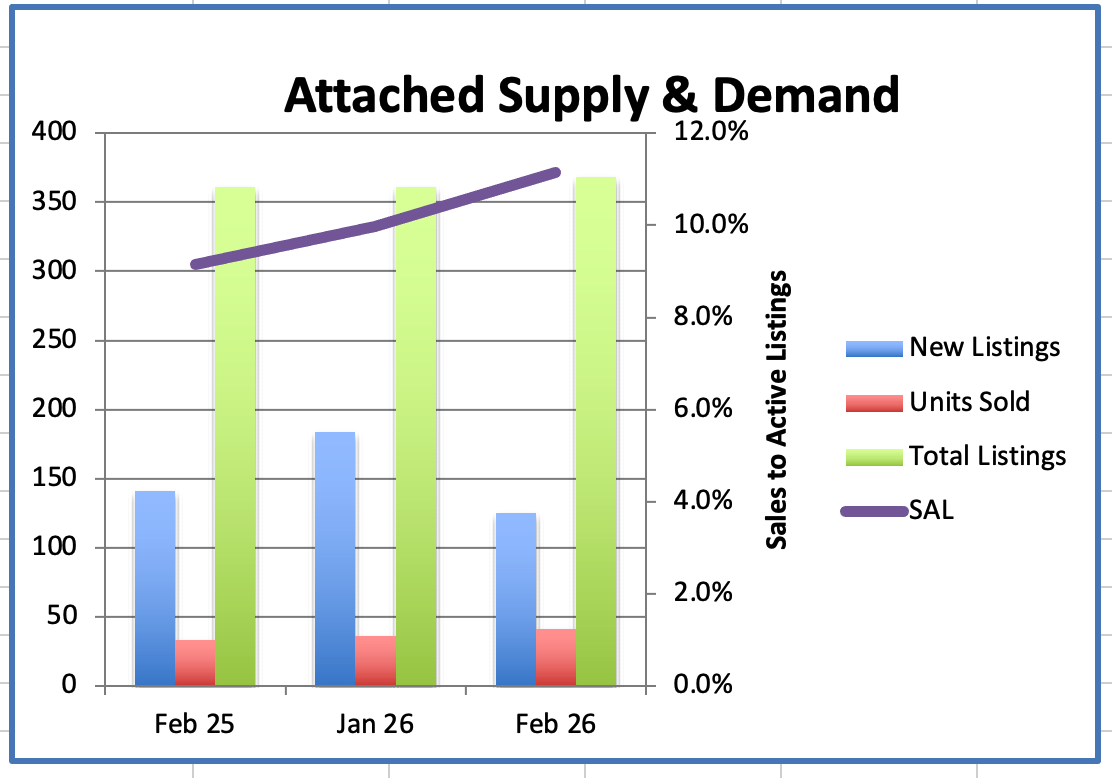

We had 41 Westside Attached home sales in February 2026, up 24% compared to 33 sales in February 2025.

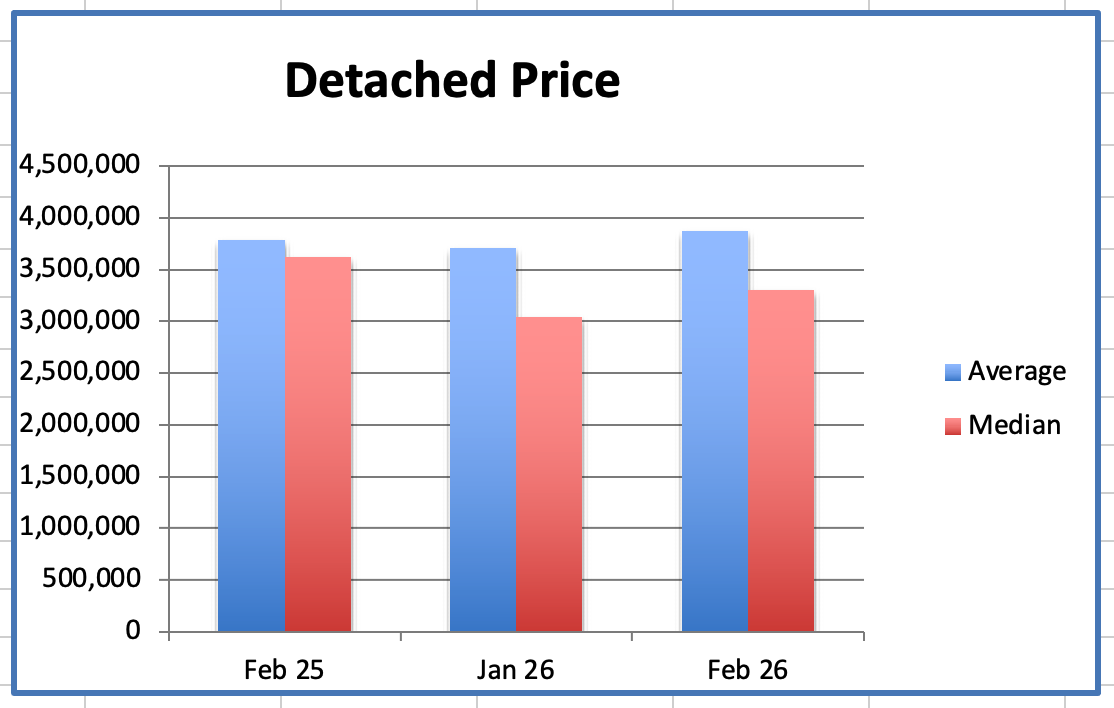

In February the Westside Detached Home average price was $3.868M, down 19% from $4.744M, the peak, in August 2023.

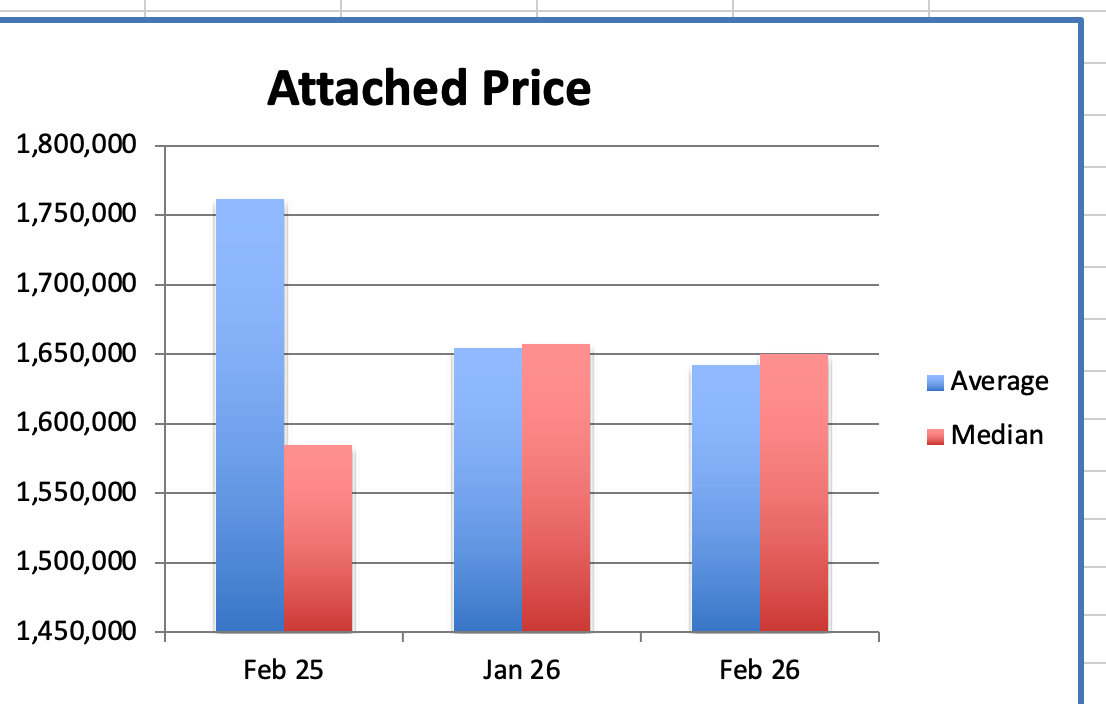

The Attached home average price was $1.642M, down 13% from $1.885M, the peak, in Dec 2024.

The Apartment average price was $896K, down 25% from $1.199M, the peak, in January 2018.

The Sales to Active Listings ratio (SALR) is a key indicator of market balance and it helps determine whether the market favours Buyers or Sellers. The range between 12% and 20% is considered a balanced market and prices are sustained.

Generally, downward pressure on home prices occurs when the ratio dips below 12% for a period of time. Upward pressure on home prices occurs when the ratio surpasses 20% over several months.

Currently the SALR for westside Detached homes is 9%, Attached homes is 11% and Apartments is 14%.

Market conditions are dynamic and can change rapidly due to various economic factors & the ratio can vary significantly depending on the property type.

Historically, the market has cycled up in the spring, slowed down in summer, revived a bit in the fall and become quiet in the winter. Currently the seasonal cycle has been disrupted by economic uncertainty, interest rate affordability, job security and global events that have combined to flatten out the demand for real estate.

Our current Buyers' market and expanding supply have not translated into a rush of activity but rather has reduced urgency as buyers are able to be more discriminating in their purchase. This compels Sellers to be more realistic in their price expectation if they want to be the best value in their cohort and sell rather than just sitting on the market.

Affordability is what buyers need and well priced homes offering good value are selling. Fewer Buyers are speculating and more are buying for a roof over their heads. Sellers are starting to grasp the idea that value is what is selling and they are adjusting their asking prices accordingly.

Buyer confidence while not lacking for folks needing a roof over their heads, is diminished compared with years gone by and relates to events beyond real estate into global headlines, consumer tariffs and other issues which detract from market momentum.

The years of irrational exuberance and speculative activity in our market have shifted to a more rigorous and rational search process less whipped into a frenzy by the fear of missing out.

This too may all be a cycle but it is not the seasonal cycle we are used to.

This is a buyers' market and a good opportunity to get into the market or to move up in the market. We expect the market to remain slow but we know that can change in an instant.

Sellers need to be the best value in their cohort to attract a buyer so strategic pricing is the key to achieving a sale.

Thinking of Buying or Selling? Let’s Talk!

📞 Call me today to discuss your options and make the most of the upcoming selling season.

Happy St. Paddy's Day! 🌈☘️🍺☁️🌱

Best regards

Stuart ⛳ 🎾

|