Budget Updates from

Mayor Chess

| |

| Budget Options to Decrease the Tax Burden on Homeowners | |

***Please read to the end of this message for examples and

to fully understand the impact these programs could have on your taxes.***

The Town Council and the Mayor‘s Office continue to work together reviewing the budget as presented. This past week, my Administration presented several options to reduce the burden on our taxpayers. You can watch the full budget workshop and see the presentation here.

I am working hard to find and use every tool at my disposal to make it easier for people to continue to afford to live in our beloved town, especially people on fixed incomes.

Below are three options being reviewed to help ease the tax burden.

Urgent action is required this coming week by the Town Council if we are going to be able to implement a program to decrease the tax burden. The second option below is the Homestead Act, which I strongly support and recommended to the Town Council. It has many statutory requirements that will take time to fulfill, which is why we will have to decide next week whether to move forward with this option.

I ask you to please reach out to your Town Council representative and let them know what you're thinking and which option you're in favor of. You can find your representative's contact information here.

Tax Relief Options:

1.) Enhanced Relief Programs

We are discussing expanding Stratford's current tax relief programs to further assist seniors, veterans with low incomes, and people with disabilities.

2.) The Homestead Act

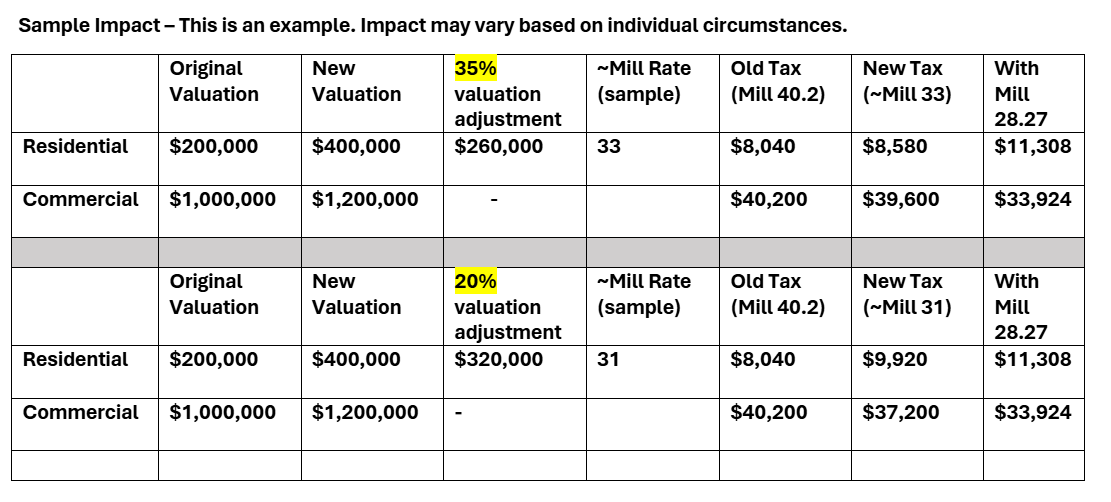

In May 2025, the State Legislature passed the Homestead Act, House Bill 7274. This law gives local governments more control to tailor their property tax relief. The law allows towns to adjust home values by up to 35% if residents own and reside in the home. I am actively working with the Town Council to explore this option and its ramifications. This option would allow the value of our homes to be adjusted down at least until the next revaluation. You can see an example of how this would work below.

3.) The Phase In Scenario

In this scenario, the increase in the tax burden would be phased in over one to three years. Every year, property owners would see an increase. The Phase In option is a tool available to towns in situations such as a revaluation, when property values increase significantly, leading to sudden, steep tax increases. It provides a buffer for taxpayers, particularly people on fixed incomes, such as seniors or low-income households. It can also help homeowners plan for costs over a multi-year period.

| 2025 REVALUATION Homeowner Impact & Mitigation Strategies | | |

When a revaluation occurs, the Tax Assessor establishes the current fair market value of all real estate in order to equalize the tax burden among property owners. Under Connecticut law, the assessment of each parcel of real property represents 70% of its fair market value as of October 1st. Unless there is a physical change to a property (e.g.; new construction, renovations, or demolition), its assessment remains unchanged until the next revaluation.

Revaluation results are put through statistical testing to determine the level of uniformity among properties. The testing standards are set by the Office of Policy and Management to assure new assessments are deemed equitable. Stratford’s measure of equity is considered excellent.

THREE METHODS FOR MITIGATING THE IMPACT OF REVALUATION

1 - Full Implementation – Ad Valorem (at value) taxation of all real property at equitable levels based on October 1, 2025, carried out through Stratford’s next revaluation.

2 - Homestead Act

3 - Phase In

| Full Implementation Option (the usual approach) | |

The mill rate calculation is based on the full 70% assessment as developed through the revaluation process. Under this option, the effects of the revaluation would be completely absorbed in the first year. Future growth would be 100% organic due to new construction and discoveries.

Advantages

- Easiest to explain and understand both the new values and the revaluation process

- New values are defendable using the sales analyzed

- Produces the lowest possible mill rate, which will reduce taxes for most, if not all, motor vehicle and personal property owners, as well as some real estate owners

- Equalizes the tax burden between all classes of property owners (this is exactly the reason why we perform revaluations)

- Provides most tax relief for property owners who have been “relatively” over-assessed

- Increases the taxes for those property owners who have been “relatively” under-assessed

- Reduces court appeals by major taxpayers

- All tax shifts occur in the first year. All future tax increases or decreases would be the result of new construction and the budget process, not revaluation assessment shifts

Disadvantages

- Causes a shift of the tax burden to residential properties

- New construction of any kind cannot be fully assessed and must also be phased-in

| Homestead Act Exemption Analysis | |

Public Act 24-151 Sec. 71 enacted a Local Option for municipalities to allow for a Homestead Exemption on residential dwellings that are the primary residence of their owners. The text of the Statute reads:

“12-81oo. Municipal option to provide exemption for percentage of assessed value of owner-occupied dwellings. Any municipality may, upon approval by its legislative body or, in a municipality where the legislative body is a town meeting, by vote of the board of selectmen, provide an exemption from property tax of not less than five per cent and not more than thirty-five per cent of the assessed value, for owner-occupied dwellings, including condominiums, as defined in section 47-68a, and units in a common interest community, as defined in section 47-202, that are the primary residences of such owners and consist of not more than two units.”

- 14,992 eligible properties in Stratford

- 13,900 single-family homes

- 1,092 two-family or single-family w/ in-law

- Exemptions reflect a reduction in assessed value

| |

What this example shows:

If you live in an eligible home – the above example highlights a home whose value increased from $200,000 to $400,000.

- Without the Homestead Act, the new tax would be over $11,300.

- With a Homestead Act 35% reduction in value, you would only pay $8,580. Almost $3,000 savings.

Of all the options, the Homestead Act has the greatest impact on what homeowners pay. Not the mill rate, but the actual cash.

It shifts costs from the homeowner back to commercial.

It doesn’t increase commercial – it keeps commercial steady.

Disadvantages

Implementation - It requires action by the end of this week (April 17, 2026) in order to get this done.

This program would impact 14,992 residential properties of our total 19,843. If implemented immediately, the required completion date is June 12, 2026, in order to be reflected on the tax bills, which must be mailed before July 1st.

The taxpayer would be required to submit an attestation to the Assessor stating he or she maintains their property as their primary residence. As with any other tax relief program, the Tax Assessor’s Office will review and verify each claim (12-89). After preparing, mailing, collecting back, and verifying said form, a Certificate of Correction would be processed to reflect the exemption amount. Each application will take 15 minutes to process and 5 minutes to issue corrections. This must be done prior to the required completion date of June 12.

Assuming conservative participation rate of 20%, the total administrative effort would require roughly six weeks of uninterrupted processing by 5 staff members, far exceeding normal operational capacity.

In order for completion by June 12, 2026, affidavits would have to be in the mail by April 17. This level of demand would occur during one of the busiest statutory periods of the assessment year. The Board of Assessment Appeals is in session, elderly benefit applications remain open for another month with certified mailings required by 4/30, with more than 600 completed permits must be entered and inspected prior to June 12th. Given the current responsibilities of the Assessor’s Office, all governed by Statute and which cannot be deferred, the addition of a large-scale exemption program within this timeframe would be operationally infeasible between now and the start of the new fiscal year without incurring significant cost.

| |

This allows for the gradual increase of assessments over 3 years of the revaluation cycle. The annual increase for each property would be equal to 1/3 of the difference between their old assessment (2024 GL) and the new 2025 revaluation assessment. Stratford cannot phase-in over 4 years, as it would not meet the statutory requirement of at least 20% per year.

Assessments on properties where the assessment has decreased are not allowed by statute to be phased in. Motor Vehicles and Business Personal Property are also not allowed to be phased in.

| |

Advantages

- Phases in the tax shifts between property classes and subclasses over the years of the revaluation cycle

- Real Estate to Motor Vehicle and Personal Property then back to Real Estate

- Commercial/Industrial real estate to Residential real estate

- Single-family residential to multi-family residential

- Inland to waterfront

- Provides the largest amount of tax relief to those who would receive the greatest tax increase as a result of the revaluation

- Exemptions will gradually lose their value, but not until the later years of the revaluation cycle

Disadvantages

- Difficult to explain and even more so to understand

- Results in an assessment and tax increase every year.

- New construction and other improvements to properties must also be phased-in even if they happen after revaluation.

- Decreases in value cannot be phased and would automatically go into effect

- Each property is assessed at a different percentage of the fair market value. No true equalization

- Public perception of a phase-in viewed as an annual revaluation with our next scheduled for 2029.

- Administrative challenge for Assessor’s Office & Finance Department

- Motor Vehicles and Personal Property carry a disproportionate share of the tax burden until the phase-in is complete

- Properties that have been “relatively” over assessed will not receive their full, deserved tax relief

- Properties that have been “relatively” under assessed will continue to receive a break on their taxes

- Mill rate may not decrease from 2025 to 2026 Grand list year, and will not decrease as much if a full revaluation implementation was implemented

- Difficult to track organic grand list growth YOY

- Even though the Grand List would see an increase over the following 4 years, the mill rate may not decrease proportionately due to budget changes

| |

This allows for the gradual increase of assessments throughout the revaluation cycle with a fixed, equal percentage increase covering all 3 property classes. The percentage is determined by taking the difference between 70% (the statutory assessment rate in the revaluation year) and the overall rate of assessment from the year prior divided by the number of years of the phase in term.

The overall rate of the pre-revaluation is determined using the Aggregate Mean Ratio of all real property sales in the 3 classes (per statute) that occurred. Total pre-revaluation assessment of sales divided by total price sold = aggregate mean ratio. Then, the 70% assessment ratio is subtracted from the AMR, then divided by 4 (if the intent is a 4 year step up).

For example, using the actual sales data from Stratford’s Revaluation:

- The annual increase for residential properties would be 8.627%

- The annual increase for commercial properties would be 6.179%

- The annual increase for vacant land would be 3.328%

| |

Advantages

- Phases in the tax shifts between property classes and subclasses over the remaining 4 years of the revaluation cycle somewhat equally

- Provides some tax relief to most real estate owners

- Exemptions will not lose value until the later years of the revaluation cycle

Disadvantages

- Very difficult to explain and even more so to understand

- Results in an assessment and tax increase every year

- Different property classes will have different assessment percentage increases

- Public perception of a phase -in viewed as an annual revaluation. Reval in 2029 again

- Administratively challenging for Assessor’s Office & Finance Department

- Cost involved for vendor to re-write program (undetermined, but definite). Timing restraints to re-write program for 3 different classes

- Motor Vehicles and Personal Property carry a disproportionate share of the tax burden until year 4

- Properties that have been “relatively” over assessed will not receive their full, deserved tax relief

- Properties that have been “relatively” under assessed will continue to receive a break on their taxes

- Mill rate may not decrease from 2024 to 2025 Grand list year, and will not decrease nearly as much if a full revaluation implementation was put into effect

- Even though the Grand List would see an increase over the following 4 years, the mill rate may not decrease proportionately due to budget changes.

| | Upcoming Meetings Where You Can Get More Involved | | |

1.) April Town Council Meeting - PUBLIC FORUM OPPORTUNITY

- Monday, April 13, at 6:00 PM in Council Chambers. Public Forum starts at 6:00 PM, Community Development Block Grant Funding Public Hearing starts at 6:30 PM, and the Town Council meeting starts at 7:00 PM.

2.) Budget Workshop Session 4

-

Tuesday, April 21, at 5:30 PM in Council Chambers, there will be a review of proposed Town Department budgets (Economic Development: Planning & Zoning, Building Inspection, Health Department, Community Services, Senior Center/GBTA, Sterling House and Library). The recorded YouTube link will be uploaded the next day.

3.) Budget Workshop Session 5

- Monday, April 27, in Council Chambers (start time will follow the initial Ordinance Committee). A review of the Water Pollution Control Authority’s proposed budget. The recorded YouTube link will be uploaded the next day.

4.) Budget Workshop Session 6

-

Wednesday, April 29, at 5:30 PM, in Council Chambers, there will be a review of proposed Town Department budgets (Public Works: Recreation, Parks, Engineering, PW Administration, Highways, Town Garage, Refuse/Recycling, and Building Maintenance). The recorded YouTube link will be uploaded the next day.

5.) May Town Council Meeting - PUBLIC FORUM OPPORTUNITY

- Monday, May 11, Town Council Meeting in Council Chambers, which includes a Public Forum, an opportunity for the community to share their input.

| | | | |

If you have a friend or neighbor who hasn't yet signed up for our newsletter, please feel free to invite them to sign up here.

Please also follow us on Facebook and visit our website for updates (links below!)

In Service,

David

Mayor of Stratford

| | | | | |