Weekly update from the National Housing Conference | | News from Washington | By Brittany Webb | | |

DOJ scales back disparate impact protections

The Trump administration rescinded critical federal “disparate impact” protections, withdrawing the established regulatory framework that allowed discrimination to be demonstrated through policies with unjustified discriminatory effects. The Department of Justice Department’s action changes its regulations under Title VI of the Civil Rights of 1964, dismantling the prior effects-based standard and replacing it with a substantially narrower test. The new interpretation elevates causation burdens, limits the circumstances under which statistical disparities may constitute evidence of discrimination, and requires claimants to satisfy thresholds that civil rights groups say are nearly impossible to meet without proving intent. Though the focus on Title VI does not gut disparate impact from all fair housing protections, it does impact entities that receive federal funding, impacting housing as well as other areas like education, policing, and environmental protection.

The National Fair Housing Alliance (NFHA) condemned the rollback, warning that eliminating the effects-based framework strips away one of the Fair Housing Act’s most important enforcement mechanisms. NFHA emphasized that disparate impact has been essential to correcting systemic barriers embedded in lending, insurance, zoning, and tenant-screening practices. By removing the established standard and adopting a test that significantly restricts actionable claims, NFHA argues the administration is creating substantial obstacles for identifying discriminatory outcomes and protecting communities that disproportionately bear the burden of inequitable housing policies.

The DOJ seemingly defended its position with the argument that the civil rights law encouraged enforcement of civil rights, negating the fact that discrimination can and does occur without inherent intentionality. “The prior ‘disparate impact’ regulations encouraged people to file lawsuits challenging racially neutral policies, without evidence of intentional discrimination,” said Assistant Attorney General Harmeet Dhillon of the Justice Department’s Civil Rights Division. “Our rejection of this theory will restore true equality under the law by requiring proof of actual discrimination, rather than enforcing race- or sex-based quotas or assumptions.”

NHC criticized the decision in a press release, stating that rescinding disparate impact guidance “creates harm, confusion, and legal risk” for the housing sector. NHC noted that the prior framework provided clear criteria for evaluating potential discriminatory effects, supporting compliance across lenders, insurers, developers, and local governments. By replacing that clarity with a more restrictive and less predictable standard, the change undermines fair housing enforcement at a moment when structural barriers and rising housing costs continue to disproportionately affect marginalized households. A group of over 200 former employees of the Civil Rights Division of the DOJ also released an open letter sharply refuting the decision, stating “America deserves better.”

| |

HUD withdraws contested homelessness policy changes

The U.S. Department of Housing and Urban Development (HUD) withdrew its November FY2025 Continuum of Care (CoC) Program Notice of Funding Opportunity (NOFO) that sparked significant bipartisan concerns across the housing community and prompted legal challenges. The changes would have constituted a significant shift in fund allocation, moving homelessness services focus away from permanent supportive housing toward transitional housing with work or service condition, reportedly risking displacing 170,000 individuals at risk of falling back into homelessness. According to HUD, the withdrawal will allow HUD to “make appropriate revisions to the NOFO, and the Department intends to do so. In the previous FY 24-25 NOFO, the Department reserved the right to make changes to the NOFO instead of processing renewals for a variety of reasons, including to accommodate a new CoC or Youth Homelessness Demonstration Program priority or new funding source. The Department still intends to exercise this discretion and make changes to the previously issued CoC NOFO to account for new priorities. HUD anticipates reissuing a modified NOFO well in advance of the deadline for obligation of available Fiscal Year 2025 fund.” The legal case brought against the Administration is continuing despite the withdrawal.

Multiple letters were sent regarding the NOFO, including one from the U.S. Conference of Mayors. The Conference sent a letter to Congressional leadership detailing their concerns with the proposed changes and asking for full CoC funding in 2026 in order to ensure there are no gaps in funding and offer more time to plan for coordinated changes.

“It is far too late in the year for HUD to initiate a new grant process for funds that will begin to expire in January 2026. Earlier this year, when grant agreements for the last round of funding were delayed, state and local governments had to absorb the gaps to ensure rents were paid to landlords and programs could continue to operate. It is simply not feasible for us to absorb these gaps again in 2026,” the letter reads. “We strongly urge you to take action to direct HUD to renew all existing Continuum of Care grants expiring during calendar year 2026 for one 12-month period. This will ensure there are no unnecessary gaps and delays in resources and provide communities more time to plan accordingly. Such action would have no budgetary impact.”

| |

Housing provisions left out of NDAA; House leaders introduce new bipartisan housing package

Following weeks of negotiations, policymakers and stakeholders alike were disappointed following the exclusion of the ROAD to Housing Act (ROAD) in the must-pass National Defense Authorization Act (NDAA). The Senate, led by Senate Banking Committee Chairman Tim Scott (R-S.C.) and Ranking Member Elizabeth Warren (D-Mass.), worked alongside the White House to include ROAD, or a House-negotiated version of the bill, in the final NDAA. The ROAD to Housing Act advanced earlier this year with broad bipartisan support, passing unanimously out of the Senate Banking Committee in July, and later passing the full Senate as part of its version of the NDAA. Speaker of the House Mike Johnson (R-La.) and House Financial Services Committee Chairman French Hill (R-Ark.), however, could not reach an agreement with Senate leaders, resulting in the final NDAA passing without a housing package.

The House Financial Services Committee has been pursuing its own housing legislation in recent weeks. It held a hearing on a suite of housing bills earlier this month and introduced the bipartisan Housing for the 21st Century Act. The bill was formally introduced on December 11 by Chairman Hill and Ranking Member Waters (D-Calif.), along with Housing & Insurance Subcommittee Chairman Mike Flood (R-Neb.) and Ranking Member Emanuel Cleaver (D-Mo.). The legislation is designed to expand housing production and improve affordability by modernizing outdated programs, removing regulatory barriers, strengthening support for manufactured and factory-built housing, and increasing financing options such as small-dollar mortgages. It also enhances transparency, consumer protections, and federal oversight to ensure programs support stable, affordable housing for households across income levels. The Committee has scheduled a December 17 markup for the bill.

“It is critical that we deliver real solutions that empower Americans and strengthen communities,” committee Chairman Hill said in a statement. “This month, the Financial Services Committee will advance solutions to tackle housing cost and access challenges for American families, homeowners and renters. Next year, we look forward to working with our Senate colleagues to send a bill to the president’s desk that reflects the views of both chambers and leads to more affordable choices for America’s homeowners and renters.”

“The cost of living remains the most urgent challenge facing Americans in every region of the country, and tackling that crisis begins with bipartisan, comprehensive housing reform,” said Ranking Member Cleaver. “Over the past year, Ranking Member Waters, Chairman Flood, Chairman Hill, and I have worked with Committee members on legislation that cuts unnecessary red tape, accelerates the development of affordable housing, and reduces costs for hardworking families. I’m proud of the bipartisan package we are introducing today and look forward to working with the House and Senate to advance critical housing legislation to the president’s desk.”

NHC President and CEO David M. Dworkin released a statement in support of this legislation. “By modernizing outdated housing programs, reducing unnecessary barriers to development, and increasing flexibility for local communities, the Housing for the 21st Century Act helps create the conditions needed to build and preserve more affordable homes across America,” Dworkin said. “Addressing the shortage of affordable housing will require sustained bipartisan action. NHC looks forward to working with Congress to advance bipartisan housing legislation and help ensure it moves forward with the broadest possible support.”

The introduction of this legislation and the planned markup help continue momentum for a bipartisan housing package as the House and Senate are expected to continue to negotiate between their two bills.

|

| | |

FOMC lowers rate by quarter point

The Federal Reserve Board of Governors’ Federal Open Markets Committee (FOMC) lowered the target federal funds rate by a quarter point, bringing the range to 3.5-3.75% and its lowest level since November 2022. The move is the third straight time the FOMC has lowered rates as it contends with a softening labor market alongside persistent inflation. The FOMC’s decision was made based on delayed economic data reports that have yet to become public after the prolonged government shutdown. The Bureau of Labor Statistics also announced that it will skip publication of its producer price index report for October, which informs the Fed’s decision-making as a preferred inflation indicator. The information will be published in January.

The rate change was approved by a vote of 9-3 with dissenting opinions to not cut the rate at all from members Jeffrey Schmid and Austan Goolsbee, and member Stephan Miran who argued for a 50-basis point cut.

Fed Chair Jerome Powell continued to emphasize that mortgage interest rates would not see significant improvement due to ongoing housing supply shortfalls. “Housing is going to be a problem," he stated bluntly.

| | | |

|

Fannie Mae expands MH, ADU flexibilities

Fannie Mae made substantial updates to its Selling Guide, significantly expanding eligibility for accessory dwelling units (ADUs) and manufactured home improvements as part of a broader strategy to increase affordable housing supply. The changes allow a wider range of ADU construction and rehabilitation activities, including attached or detached units, conversions of existing space, and ADUs on single-unit properties where permitted. Fannie Mae also now allows an ADU on single-unit manufactured homes, including single- and multi-section units, and permits multiple ADUs on certain MH Advantage® homes.

Fannie Mae also strengthened renovation pathways for manufactured housing by eliminating the prior $50,000 or 50% as-completed value cap and replacing it with a single cap based solely on 50% of the as-completed value, allowing more substantial updates to aging homes and aligning policy more closely with site-built housing. The release also introduces HomeStyle Refresh, an updated version of Fannie Mae’s energy-efficiency program, which enables borrowers to finance resiliency improvements without an energy report and provides higher allowable loan-to-value ratios for those upgrades. The changes come into effect March 31.

| |

Housing Trust Fund awards released

HUD released its FY2025 Housing Trust Fund (HTF) allocation amounts. The total allocation stands at $223 million, with state allocations ranging from $23.5 million to the small-state minimum of $3 million. Puerto Rico will also receive $688,000. HUD administers the HTF as established by the Federal Housing Enterprises Financial Security and Soundness Act of 1992 and amended by the Housing and Economic Recovery Act of 2008.

|

| | |

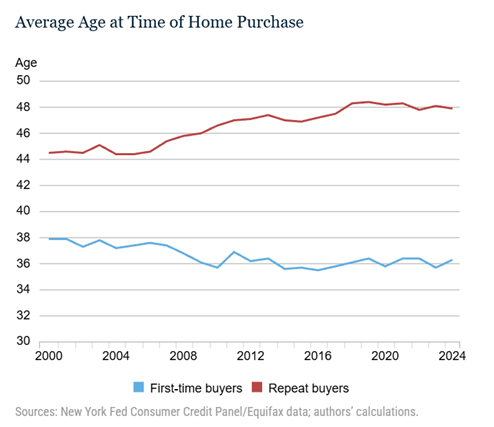

Age of first-time homebuyers may still be mid-30s

Research from New York Fed’s Liberty Street Economics explores characteristics of first-time homebuyers, challenging reports that the average age of first-time buyers is 40. The research shows that elevated home prices and mortgage rates are contributing to slightly later transitions into homeownership-but determines the average age of first-time buyers remains in the mid-30s at 36.3. Credit scores for all buyers have also shown increases, while average incomes have shown notable decreases, suggesting that first-time buyers are seeking homes in lower-income neighborhoods to contend with rising housing costs.

| | |

The Terner Center published a brief on the potential end of Emergency Housing Vouchers (EHVs), warning that allowing the program to lapse would likely push thousands of extremely low-income households, many already formerly homeless, back into housing instability or homelessness, with disproportionate impacts in high-cost, low-vacancy markets. The report underscored that EHV’s have become a critical, time-limited layer in local rehousing systems, helping communities leverage existing coordinated entry and landlord-engagement infrastructure rather than building new capacity from scratch. It recommends that federal policy makers either extend or transition EHVs into ongoing rental assistance, while local jurisdictions prepare contingency plans to prevent mass voucher expirations from undermining recent gains.

A recent report from the Government Accountability Office reveals how technology is fundamentally transforming the mortgage lending process, with automated systems now central to how Americans secure home loans. GAO notes that these advances carry substantial risks that federal oversight has not addressed. In loan evaluation, automated underwriting systems developed by Fannie Mae and Freddie Mac dominate the market, with lenders relying on these tools to assess whether mortgages meet eligibility requirements for purchase by government-sponsored enterprises. However, the “black box” design of AI-driven credit models makes it difficult for lenders to explain denials as required by law and for regulators to detect discriminatory patterns. GAO warns that federal oversight has not kept pace with these technologies, and that recent changes by the Federal Housing Finance Agency impacting fair lending requirements must be clarified.

An analysis published by Moneywise documents rural America’s intensifying housing affordability crisis, where median home prices have surged 61% since pre-pandemic levels to $280,000, far outpacing the 33% rise in median household incomes. A typical home purchase in rural areas now requires a salary of $74,508, a 106% increase from 2019. This concerning disparity is driven by supply constraints, remote work migration patterns, and persistent wage stagnation in rural counties that collectively threaten homeownership accessibility for younger households and families.

| | |

Expanding housing options for communities across the U.S.

Access to safe, stable, and affordable housing is vital for strong communities. Yet, many families across the U.S. continue to face challenges finding affordable housing options, limiting working mobility and economic growth.

JPMorganChase is helping to address this challenge through its business, philanthropy, and policy advocacy. Over the past five years, the firm has supported the creation of more than 400,000 affordable housing units nationwide. Last month, they announced over $40 million in new philanthropic funding to support organizations driving innovative solutions—from new construction models and financing strategies to rental preservation and home improvement loans for low- and moderate-income families.

This commitment builds on their ongoing business efforts, including more than $5 billion in affordable housing financing in the first three quarters of 2025 alone. It also follows their latest policy brief, which highlights state and local strategies to increase housing options.

JPMorganChase remains dedicated to expanding housing options and strengthening communities—partnering nationwide to help build a brighter future for all.

| | |

Monday, December 15

No events posted.

Tuesday, December 16

Ensuring Fair Access to Banking: Policy Levers and Legislative Solutions | Hearings | United States Committee on Banking, Housing, and Urban Affairs, 3:00 PM ET

Wednesday, December 17

Markup of Various Measures | United States House Committee on Financial Services,10:00 AM ET

Unlocking Black Prosperity: Advancing Wealth through Small Businesses, Asset Development, and Community Investment, 12:00 – 1:15 PM ET

Thursday, December 18

How Communities Layer Resources to Prevent Homelessness: Insights from Detroit and the Bay Area, 3:00 PM ET

Friday, December 19

No events posted.

| | The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. | | Defending Our American Home since 1931 | | Copyright © 2024. All Rights Reserved. | | | | |