Access our research on the Bloomberg Terminal with ERH GXY <GO>

|

|

gm -

as a refresher, the letter from the editor series is a periodic section of the galaxy digital research brief that contains opinion from yours truly on markets and current events. the first one i wrote back in february was on the implications of russia's invasion of ukraine on the international monetary order and cryptocurrencies. you can read that essay in full here. my latest entry, which you will find by scrolling to the bottom of today's newsletter, highlights the three key regulatory issues around crypto being discussed by policy makers and lobbied by industry stakeholders on capital hill. read it in full below.

in addition, episode 12 of galaxy brains is live and includes a conversation on the crypto markets with beimnet abebe from galaxy's principal trading team, as well as extended commentary about my trip to washington with tyler williams from galaxy digital's legislative and regulatory affairs team. we also discuss the optimism team officially airdropping the first batch of OP tokens to users and galaxy digital research's most recent report on the solana blockchain. be sure to catch the episode on apple, spotify, amazon, youtube, or wherever you get your pods.

plus in today's newsletter, we demystify the hype around goblintown nfts and analyze the latest data around btc miner flows.

have a great weekend,

alex

|

|

NEW: Ethereum All Core Developers Call #139 & Consensus Layer Call #88 Writeup |

|

Ethereum core developers concluded their 139th bi-weekly Zoom meeting on Friday, May 27th. Unlike the Consensus Layer calls, which occur every other Thursday at 14:00 UTC and are attended primarily by developers building the consensus layer software of Ethereum, the All Core Developers (ACD) calls are attended by developers building either the consensus or execution layer of Ethereum. On Friday, developers discussed:

- the status of Merge testing,

- the difficulty bomb schedule,

- and two Ethereum Improvement Proposals related to sharding and Boneh–Lynn–Shacham (BLS) signatures.

- the forthcoming Ropsten hard fork

-

outcomes from the 6th mainnet Merge shadow fork

- the 7-block reorg incident on Wednesday, May 25

|

|

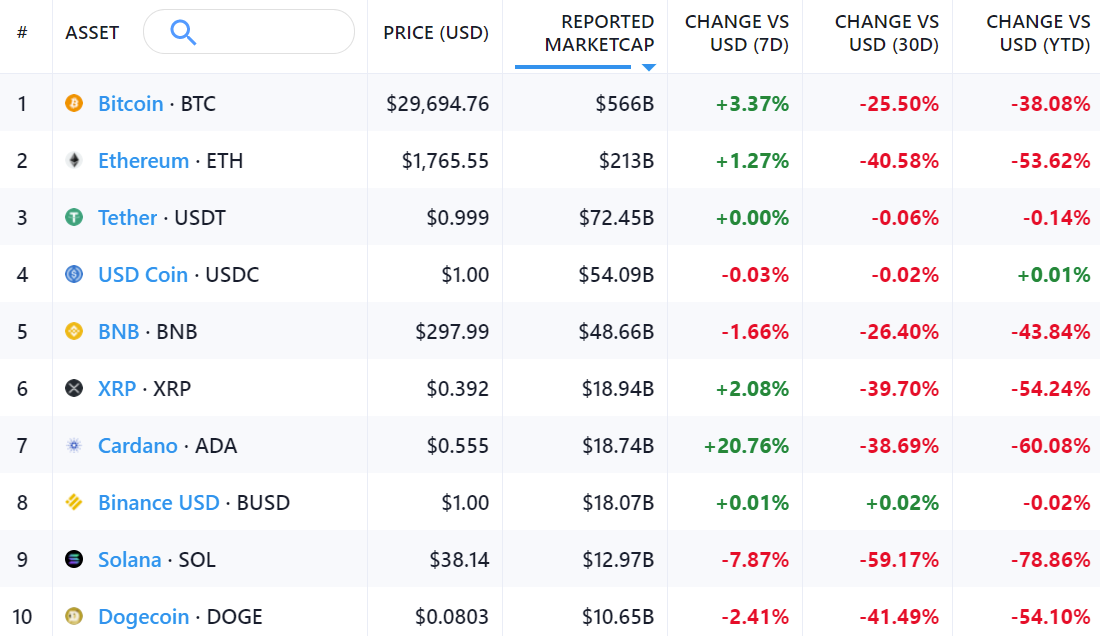

The total implied network value (market cap) of the digital assets market stands at $1.21tn, up 1.7% from last week (when it stood at $1.19tn). Bitcoin’s network value is 4.6% of gold’s market cap. Over the last 7 days, BTC is up 3.37%. ETH is up 1.27%, ADA is up 20.76%, and SOL is down 7.87%. Bitcoin dominance is 46.67%, practically unchanged from last week. |

|

Data current as of 9:33 AM ET on June 3, 2022. Prices and data via Messari.

|

|

☀️Solana Bug Triggers 4-Hour Network Outage

|

|

On Wednesday, Solana endured another full network outage for a period of 4 hours and 10 minutes. This is the third day this year it has suffered a full network outage. While initial rumors on Twitter assumed the outage was driven by spam transactions and/or Solana’s recent clock drift, thedriver wasunrelated to either of these theories. Instead, the reason for this latest outage stems from a relatively obscure feature frequently used by exchanges to send SOL tokens (usually from cold storage or with a multisig setup) without a recent blockhash. This niche transaction type is referred to as Durable Nonces according to Solana’s documentation.

Essentially, Durable Nonces are a feature that allow users to pre-sign transactions offline. Durable Nonces are most commonly used in situations where users want to sign a transaction long before the transaction is actually executed. Instead of storing the transaction signature in a block hash, which has a ~2 minute timeout, these signatures are stored in accounts. This allows the signature to persist beyond the typical 2-minute timeout and be referenced at a later time for execution. Exchanges, such as Binance, utilize the Durable Nonce feature of Solana (most likely for their cold storage setups, though this is unconfirmed).

The Solana team stated that the outage “…was caused by a bug in the Durable Nonces feature that led to nondeterminism when nodes generated different results for the same block, which prevented the network from advancing”. Anatoly tweeted on Wednesday afternoon that a temporary fix of simply disabling the Durable Nonce feature was out, and a more permanent fix is in the works. Binance stated in a recent tweet that withdrawal failures may be more commonplace until a long-term fix to this feature is released.

|

|

OUR TAKE: Many folks on Twitter were quick to criticize Solana for being offline once again, and this knee-jerk reaction is somewhat misguided. This outage does not really signal anything concerning about Solana’s design decisions in terms of scalability. However, the outage does underscore some centralization concerns that we highlighted in our recent Ready Layer One installment Surveying Solana.

Namely, Solana still has aspects of a centralized chain with a super-minority of ~19 validators able to halt the network at any given time. Solana’s “Mainnet beta” is aptly named — they once called for validators to congregate in a centralized Discord channel in order to prepare for a restart. The fact that a couple dozen validators on Solana’s PoS chain can band together to remedy a full network outage signals the high degree of Solana’s network centralization. In the long run, this centralization may be a concern as it runs counter to the ethos of crypto’s mission to decentralize the global economy. In the short-term, however, centralization may be a good thing as it allows for developmental agility. Instead of being stalled for months, Solana was able to shrug off its latest outage in a few hours.

This latest outage does not change our underlying views on Solana (discussed in detail in our latest episode of Galaxy Brains and in our report Surveying Solana). While outages and centralization may continue to be Solana’s biggest existential threats, the fact of the matter is that Solana has materialized into the most complete alternative to the Ethereum network. Solana’s strategy to prioritize usability and speed in a race to acquire users and developers while ironing-out protocol-level kinks on-the-fly makes it a compelling protocol for use. -SQ

|

|

👹Down, Down to Goblintown |

|

The most popular non-fungible token (NFT) collection being traded on the internet right now are profile picture-style images of grotesque goblins. These goblin PFPs have clocked $26.7mn in trade volume over the past week, surpassing that of any other NFT collection including the incumbent Bored Ape Yacht Club (BYAC) collection which reached a volume of roughly $18.2mn this past week, according to data from DappRadar. The highest sale for a goblin in this collection sold for 77.75 ETH (roughly $144,600) on NFT marketplace LooksRare this past Wednesday, though it is worth noting that wash trading on LooksRare is a common occurrence. On average, these misshapen goblin heads have sold for nearly $8,000 on various NFT marketplaces including LooksRare and OpenSea.

The meteoric rise in popularity and hype for Goblintown NFTs began two weeks ago on Wednesday, May 19th when an unknown group of creators launched mining for the Goblintown collection on Ethereum. The NFTs were free to mint and only required users to pay for the transaction fee associated with the mint. By Thursday, May 20th, all 8,999 goblin NFTs had been minted with an additional 1,000 of them purposefully held back for the collection’s creators. When it comes to information about the purpose and meaning behind this NFT collection, there’s little to be gathered. The official website for Goblintown reads: “No roadmap. No Discord. No utility. [Creative Commons Zero]. [Smart] contract wasn’t actually written by goblins.”

The mystery around the origin of the Goblintown project as well as the rationale for its wild success as of late has been a source of significant controversy on crypto Twitter. The smart contract design for Goblintown, the artwork, and the execution of the launch all suggest that the creators behind the collection are crypto NFT veterans. In addition, the high royalty rate of the project, meaning the percentage of the sale price that is rewarded to the original creators of the NFT every time it is sold on a marketplace, suggest an intentional profit-focused strategy at play behind-the-scenes by the creators. As background, most NFT collections charge a royalty rate of roughly 5%. The royalty rate for Goblintown NFTs is 7.5%, which means the creators have made upwards of $2.7mn from Goblintown NFT trading activity thus far.

|

|

OUR TAKE: Against the backdrop of a depressed crypto market, the meteoric rise of the Goblintown NFT collection stands apart as a one of the few NFT collections that have been gaining rather than declining in value and adoption as of late. More than the price, volume, and general market activity of these goblin NFTs, the impact of Goblintown as a viral meme on the culture and sentiment of the crypto industry has been most noteworthy. While there are many competing definitions for what exactly the term “goblintown” even means, the general understanding is that goblintown is a colloquialism for being in a bear market and going “goblinmode” refers to entering a state of mind that is raw, dirty, and unabashed. These terms, along with the countless memes depicting goblins urinating, speaking an unintelligible language, and generally personifying a degenerate state of mind, have become part of the new vernacular of crypto Twitter and crypto culture at large.

For some, Goblintown’s success is a new low for the crypto industry reaffirming their view that the fundamentals of the NFT projects in the cryptocurrency industry are broken and simply based on “pure luck.” However, in our view, Goblintown’s success is a testament to the use of NFTs to mark a cultural moment in history, in this case the crypto bear market downturn of 2022. During times of negative market movements and industry developments, self-deprecating memes and doomposting have traditionally been popular means of self-expression in the crypto community and especially on crypto Twitter. In this case, individuals and even mainstream companies are latching on to an NFT collection and community of NFT holders for comic relief; and that alone is a pretty wild and funny concept. -CK

|

|

⛏️BTC Miner Flows to Exchanges Surge Under Bearish Market Conditions

|

|

Bitcoin miners are liquidating more of their BTC holdings due to a depressed Bitcoin price and bearish market conditions. As bitcoin price trends lower, mining becomes less profitable, forcing competitive miners to react in a fiscally responsible manner to protect their profit margins. Some miners have decided to shut down mining rigs altogether, illustrated by the falling in mining difficulty adjustment, which most recently fell by 4%. Data from Coin Metrics shows a rapid increase in miner flows to exchanges, with the 30-day average reaching as high as $200 million. Canadian mining company Cathedra Bitcoin announced that it had sold 235 Bitcoin throughout May in recent quarterly filings. The company stated, “With these sales, the Company insulates itself from additional declines in the price of bitcoin and maintains its liquidity position.” Other prominent miners join Cathedra in offloading BTC, such as Riot, who reportedly sold 200 BTC in March and 250 BTC in May.

|

|

OUR TAKE: Bitcoin miners are forced sellers at a foundation level, meaning they must sell BTC into the open market to fund operations. Many private companies and small-scale miners are forced to do this to cover the cost of energy inputs and labor, especially in the current energy landscape, which sees energy costs at decade highs. However, this system has been disrupted in recent years due to the growing adoption and acceptance of Bitcoin in the broader capital markets. Many miners have IPO’d over the past two years taking advantage of the bullish euphoria in public markets. With the title of a public company comes more accessible financing and debt-raising opportunities, allowing mining firms to circumvent selling BTC by funding operations with debt.

Cathedra Bitcoin utilized this tactic, announcing “the closing of a non-brokered private placement offering with Kingsway Capital and Ten31 consisting of the sale of 17,916,667 units at a purchase price of $0.36 per unit, for gross proceeds of $6,450,000.” However, now the Fed is vacuuming liquidity from the global markets, thus depressing the share price of publicly-traded miners and reducing the effectiveness of public offerings. In the recent bull market, remaining a profitable Bitcoin miner was akin to simply flipping a switch, but as the crypto market cools, it’s the savvy and fiscally prudent miners who will prevail. As macro-financial conditions continue to deteriorate ability to raise debt goes with it, one can expect to see further announcements from firms selling their mined BTC.

Not all institutional miners are created equal; miners such as RIOT maintain strong cash positions and free cash flow and thus have more flexibility to HODL their mined coins. RIOT mined 466 BTC in May but only sold 250 in the month, making the firm significantly positive in net holdings. Cathedra is in a very different situation, with just 3.69 BTC held at the time of Q1 2022 filing. As a small cap miner, they will have a lot of work to do with these market conditions. Fiscally formidable miners, like RIOT, may be selling BTC to take advantage of distressed opportunities via M&A through growing a cash moat. RIOT announced the hiring of an M&A banker from Nomura to head corporate development for the company. Current market conditions within crypto and in the broader market are leading miners to sell Bitcoin, but their motives are not one-sided; some are selling opportunistically, and some to survive. -LM

|

|

-

The New York State Senate passed a bill imposing a two-year moratorium on any new bitcoin mining projects powered by carbon-based fuel early Friday morning.

-

Immutable X activates protocol fees ahead of planned release of $IMX staking

-

Zcash eliminates trusted setup with major network upgrade NU5

-

Optimism network sees performance issues with launch of the OP airdrop

-

Tether provides update on reserve composition; says CP has been reduced by 20% since 3/31

-

Gemini cuts 10% of workforce, says “turbulent market conditions” likely to persist

-

Binance Labs raises $500m for web3-focused investment fund

-

Opensea’s former product chief charged in first NFT insider trading scheme

|

|

Access our research on the Bloomberg Terminal with ERH GXY <GO>

|

|

|

|

Ethereum All Core Developers Call #139 & Consensus Layer Call #88 Writeup |

Christine Kim breaks down what was discussed in the latest two Ethereum core developers meetings.

|

|

|

|

NEW REPORT: Ready Layer One, Solana |

Sal Qadir evaluates Solana in-depth and uncovers how well-positioned it is to capture and retain market share in the Layer 1 blockchain landscape.

|

|

|

|

Galaxy Digital Research Podcast |

In this week's episode, we discuss crypto markets with Beimnet Abebe, regulatory issues on the top of U.S. policy makers' minds with Tyler Williams, the Optimism team officially airdropping the first batch of OP tokens to users with Charles Yu, and Galaxy Digital Research's most recent report on the Solana blockchain with Sal Qadir.

|

|

The Letter from the Editor is a section in our weekly research brief that will appear periodically and contain opinion about current events. The views expressed here are solely those of the author and do not necessarily reflect the views of Galaxy Digital. |

|

Mr. Thorn Goes to Washington |

|

Last week, I went to Washington, DC for a conference on digital assets and American policy along with Galaxy Digital’s head of legislative & regulatory affairs, Tyler Williams. Along the way, I met with many policymakers and stakeholders both on and off Capitol Hill. We met with policymakers from House and Senate staffs, representatives from existing industry trade groups, former regulators, and other industry participants. While education level varied, the sheer number of these folks that are interested in, talking about, and reckoning with bitcoin, digital assets, and blockchain technology is staggering. There are dozens of bills floating around in Congress, either already introduced or in drafting stages. Some of them are targeted to specific issues, while others are more comprehensive.

|

|

When I first became interested in Bitcoin, and when my previous employer began working on it in earnest, we were called crazy, dangerous, utopian, or purely misguided. Bitcoin couldn’t ever really be adopted outside of criminal uses they said. Bitcoin wasn’t money, Bitcoin was dead. Not only were they wrong about Bitcoin, but other major pieces of today’s digital assets ecosystem didn’t even exist yet. DeFi wasn’t a thing. Ethereum had only just launched. Stablecoins were too nascent to matter. Non-fungible tokens were more concept than reality. And the prevailing wisdom outside of early adopters was that if any of it was to be useful at all, it was blockchain, the underlying technology. Every financial services firm and many corporations devoted innovation spending to developing a strategy for “enterprise blockchain.” But the skeptics were wrong. Over the next several years, Bitcoin became a household name—perhaps the most widely known brand with zero marketing spend. DeFi has become a large economy in its own right. Stablecoins have become so large that they have the eye of every major government and central bank on earth. Every major sports league on the planet is releasing NFTs. An what about enterprise blockchain? It’s never really delivered. I’m not putting the “nail in the coffin” for “blockchain,” but I’m also not holding my breath.

So, we’ve come a long way over the years. If you’re reading this, you probably already know that. But I was struck last week, as we shuffled between the Hay Adams hotel and Capitol Hill, with the magnitude of Bitcoin’s impact and the growth of the digital assets industry around it—not just the reality of it’s wide and growing adoption, but the impact of its narratives on the broader world.

It's clear from my meetings with policymakers this week is that there is significant support for bitcoin and digital assets more broadly. There is support because of its potential to make our monetary and financial systems more innovative, competitive, and inclusive. On the other hand, there is worry and urgency around several issues, including from our industry’s supporters. Specific issues where I’m seeing significant movement:

Stablecoins. This was already an area of significant interest among regulators, policymakers, and other stakeholders, beginning in earnest from Facebook’s failed attempt to launch Libra. That effort raised awareness about the dollar’s role in the world and what a privately issued money might mean, even outside of Bitcoin. Many of our conversations centered on the stability of stablecoins, with a recent focus on the impact of algorithmic stablecoins. The attempt to financially engineer stable value without underlying collateral has been tried many times (including outside crypto) but never meaningfully succeeded (perhaps outside of the US dollar itself), as most recently exhibited with Terra USD’s collapse, and that reality is crystallizing in Washington. The quality of stablecoin collateral was already a focus of policymakers before UST, and it continues to be. I think most industry participants agree that centrally issued stablecoins should be backed by verifiably healthy collateral. When discussing this issue with various policymakers, though, I stressed the need to ensure that any stablecoin ordained as “legal” by a regulatory regime must allow for the transfer of issued tokens between unknown parties. Said differently, holders of REGUSD must be able to send to any address—including addresses that have not been previously whitelisted by any authority, including the issuer. This cash-like experience is what stablecoin users expect, and without it, regulation will result in pushing users out on the risk curve back to offshore and/or algorithmic stablecoins. Similarly, if our policymakers want to compete with digital currencies issued by foreign nations, they need to offer a competitive alternative. Specifically, China’s “digital yuan” has features that make it incompatible with American values, and to compete with China on a fiat-backed stablecoin (should policymakers decide that is necessary), the United States should enshrine a stablecoin that reflects our values, including privacy, transferability, transparency, security, and liberty. It’s important that any regulated United States dollar stablecoin is feature-competitive with riskier alternatives and those offered by foreign adversaries.

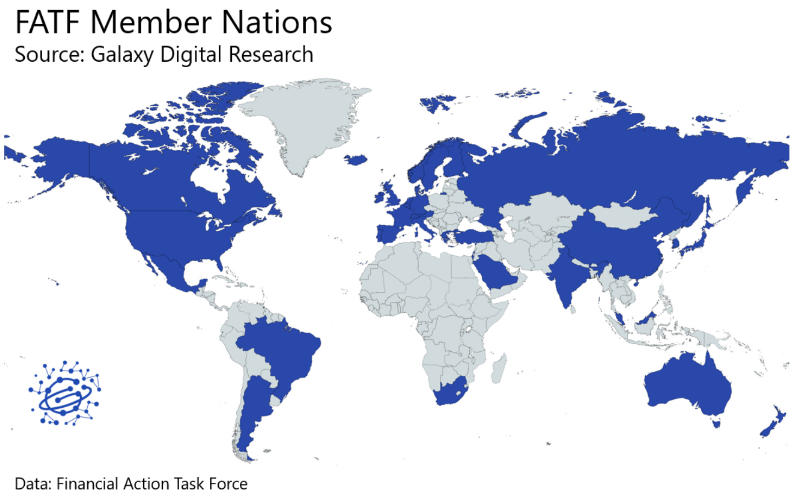

“Un-hosted” wallets. While this issue was not top of mind for most policymakers we met, I think it remains and extremely important one for Bitcoin and the broader digital assets ecosystem. The Financial Action Task Force (FATF) initially created this term, which is essentially a political marketing term. To be clear, there’s no such thing as an “un-hosted wallet.” There are only “wallets,” and this term was created to make those individuals who choose to use their own wallet, rather than rely on a custodian’s wallet, seem to be engaging in irregular behavior. The reality is that the ability to custody one’s own digital assets is a central feature of Bitcoin (and some argue a human right) and, without it, the peer-to-peer nature of digital assets is lost and the core innovation is severely degraded. FATF has cast doubt on the existence of individuals’ ability to hold their own cryptographic keys, suggesting that this allowance raises counter-terrorism financing (CTF) and anti-money laundering (AML) concerns. While FATF’s guidance is non-binding, it tends to shape how member nations approach financial regulation due to the body’s ability to put nations on the “grey list” or “black list,” making it difficult for their financial systems to access the global economy. Read more about FATF’s guidance for virtual asset service providers (VASPs) in this Galaxy Digital Research report.

|

|

In December 2020, in the twilight hours of the Trump administration, FinCEN proposed a rule that would impose significant reporting requirements on cryptocurrency exchanges that allow withdrawals to such “un-hosted wallets.” The industry, including heavyweights like Fidelity Investments, responded forcefully on both substance and process (the rule was proposed with an aggressive timetable during the holidays), and ultimately the rulemaking was delayed and then suspended. But many view that rule, which isn’t formally dead at FinCEN, as a first step towards an ultimate attempt to outright ban self-custody of digital assets by individuals. In Washington last week, I stressed to policymakers that any attempt to ban or degrade the ability of users to hold their own cryptographic keys would not only be devastating for the adoption of digital assets broadly but also would fail on a practical level, as these assets are highly resistant to confiscation. Furthermore, the global nature of the internet and thus digital assets makes it trivial for users to acquire digital assets from foreign entities, and so any such rule would simply push the growing industry into the arms of competitor nations.

Market Structure. Policymakers are also grappling with issues surrounding the general regulatory framework to oversee digital assets markets. Today, both Bitcoin and Ether are essentially treated as commodities in a formal way, with the CFTC allowing listed futures for BTC and ETH. But even Ethereum’s regulatory status here is somewhat tenuous and mostly based on comments in a 2018 speech given by William Hinman, then Director of the SEC’s Division of Corporate Finance, in which he said that he believed Ethereum was “sufficiently decentralized” and thus “current offers and sales of Ether are not securities transactions.” This opening came after years of jostling behind the scenes between SEC and CFTC over who would have regulatory oversight of the platforms that offer cryptocurrency exchange services, and it opened the door for CFTC to allow listed Ether futures. Furthermore, it also led cryptocurrency exchanges to make their judgment of the decentralization of cryptocurrency projects a major factor in determining whether or not other coins should be considered securities. While BTC, and ETH to a slightly lesser but still significant extent, feel settled as commodities rather than securities, former CFTC Chairman and current SEC Chairman Gary Gensler reiterated last month that “most crypto tokens are investment contracts under the Supreme Court’s Howey Test.” There is a behind-the-scenes jurisdictional fight between agencies, which has long existed, and that dispute extends into Congress, with commodities and securities regulated by two different agencies and overseen by two different committee structures (financial services/banking v. agriculture). The United States is the only major economy that separates the regulation of securities and commodities. So, particularly with an interest in creating a more comprehensive framework for digital assets, policymakers are grappling with how and where to assign supervisory responsibility for digital assets markets, and which resulting committee structures will oversee that supervision. (Incidentally, the issue of regulatory jurisdiction also exists for stablecoins). From my perspective, this issue is far from settled, but it’s clear that it must be settled in some way if and when we get to a comprehensive regulatory framework for digital assets.

Other issues raised included criminal use of cryptocurrencies for ransomware and illicit financing; developing a clear taxonomy for digital assets that clearly defines what is a security, commodity, utility, or something else; changing and formalizing accounting standards; providing a de minimus exemption for capital gains taxes to stop disincentivizing the use of digital assets like Bitcoin for payments, and a few other issues.

A key takeaway for me was that there was very little discussion of Bitcoin generally. I don’t see a lot on the agenda that would materially affect Bitcoin, although opposition to Bitcoin mining due to its electricity usage is still simmering. The “un-hosted wallets” issue is certainly quite important for Bitcoin, but I didn’t hear from my conversations that there’s any concerted effort to act on the issue in the near term one way or another. Rep. Warren Davidson (R-OH) introduced a bill in February called the “Keep Your Coins Act” which would specifically prevent any agency from prohibiting or restricting the ability to self-custody or conduct peer-to-peer payments. Ultimately, it’s hard for me to envision a future where humanity is highly successful that doesn’t include the ability of people to hold their own assets and conduct transactions directly without a rent-seeking intermediary. Stakeholders must be forceful in their defense of this right if we are to have any chance of making the world a better place with digital assets.

There is still a lot of education to be done, but there is more interest in and support for Bitcoin and digital assets than ever. We met with interested and supportive policymakers on both sides of the aisle, which is fitting and great to see because we don’t believe that digital assets are a partisan issue. Digital assets can be a force for financial and monetary innovation, inclusion, transparency, security, growth, and competitiveness. I was very encouraged with what I saw, and while I don’t think we’ll ultimately see much action on these issues until after the November mid-term election (or much else even outside of crypto, generally), it’s clear that, when we do, advocates for Bitcoin and digital assets will have a strong voice.

Alex Thorn

Head of Firmwide Research, Galaxy Digital

|

|

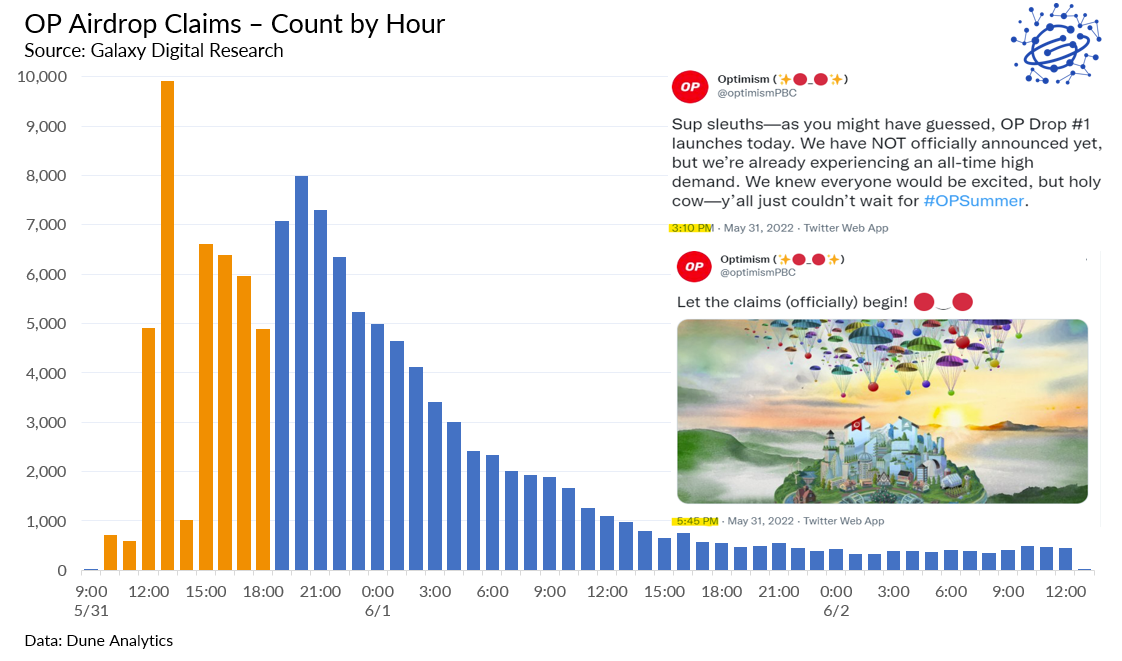

OP airdrop launched Tuesday - so far, 121k addresses (~49% of the 248k eligible addresses) claimed 135m OP tokens (~63% of Airdrop #1), averaging ~1100 OP/address (~ $1.4k at current price of $1.30). Many eligible addresses were able to access the airdrop before the official announcement came from the Optimism team, which led to network performance issues as the public RPC was overloaded. |

|

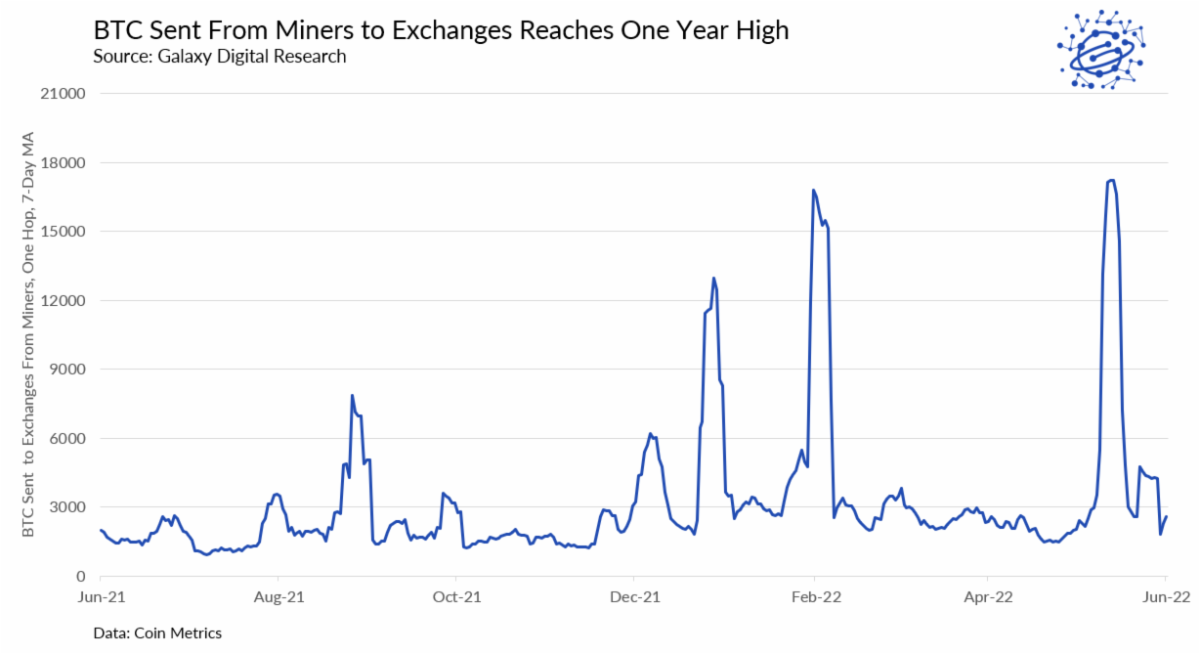

Bitcoin miner flows to cryptocurrency exchange have reached their highest point in the last 12 months, suggesting the ongoing crypto market downturn is causing bitcoin mining profitability to drop and forcing more miners to sell rather than hold on to their BTC earnings. |

|

Thanks for reading this week. Have a great weekend.

|

|

Alex Thorn

Head of Firmwide Research, Galaxy Digital

|

|

|

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. The foregoing does not constitute a "research report" as defined by FINRA Rule 2241 or a "debt research report" as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2022. All rights reserved.

|

|

|

|

|

|

|