|

Weekly Update (09-26 – 10-03): Probabilities Favor Strong Rest of 2023

Hi all –

We hope your September is going well! We wanted to send out an update on what we are seeing in markets as we enter the fourth quarter of 2023.

- As we have been anticipating, in this period of time of low/ no fundamental data, the market has allowed the macro-tail to wag the dog.

- Last week, the Federal Reserve signaled a hawkish pause. They said they were not going to raise interest rates in September, but alluded to the fact that there may be further interest rate increases as soon as November.

- The market reacted negatively to this, and interest rates have continued to increase at the longer end of the curve – with the ten-year treasury pushing above 4.55% in recent trading. Increases in long-term interest rates such as the ten-year can be associated with temporary declines in growth stocks, although the evidence shows over time that stocks can grow and most often do grow through period of Fed interest rate hiking cycles.

- In the Fed Q&A, Chair Powell seemed to signal that a soft-landing was not the objective of Fed policy. He later seemed to walk back this rhetoric and clarify it was still very much an objective, but it was not assured.

- We recognize that the UAW strike and looming government shutdown remain a risk but could actually work to undermine the Fed’s argument that the labor market is tight. If government workers lose their jobs, and if UAW workers are furloughed for some period of time, this might feed into the labor and inflation data in a way that could positively influence the market.

- On the other hand, we are seeing evidence that the writer’s strike in Hollywood might be coming to a close, which provides support for the idea that two sides can negotiate and get to a deal.

- With another earnings season coming up in October, it will be critical to examine the third quarter data for confirmation that earnings did indeed bottom, which would provide evidence that our thesis of a hard-landing or a revisit of the October 2022 lows for equity prices are not in the cards.

- With limited or no hard evidence of increased odds of a recession or stock market meltdown, we must await the more reliable earnings data that is upcoming to provide guidance for where the market could go next, while recognizing that investors still hold huge sums of cash in money markets and in banks, which they are likely waiting to deploy at favorable prices in the stock market.

- Since homeowners remain wealthy with high levels of homeowner’s equity, and limited incentive to leave their homes amid very high mortgage rates, the wealth effect strongly argues for a resumption of the status quo (i.e. no recession and no stock market meltdown).

- The black swan might be eventually in the commercial real-estate market, where the office sector is struggling. We would suggest this will likely be a region by region phenomenon that is highly specific to supply, demand, and absorption data particular to each market, in other words not necessarily a systemic melt down.

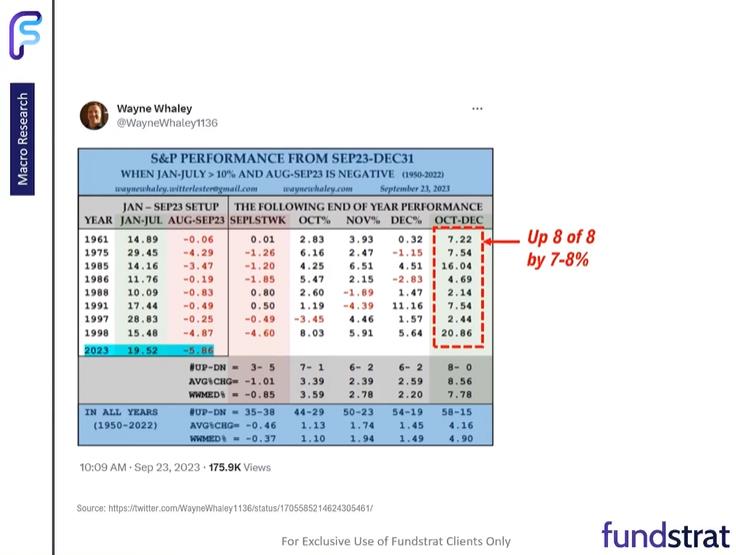

- If we look at all the years in which the stock market was up 10% or more from January to July, and negative August- September, that leaves us with eight data points in the US. The following three months of the year Oct-the end of December were positive in 8 out of 8 years and the average return was 7-8%. This argument based on the pure data science would dovetail nicely with the seasonality argument (weak in the summer).

| |

As always, please do not hesitate to reach out to us with questions. Thank you for your trust and confidence.

| |

John Bay, CFA, UCLA MBA

Chief Market Strategist

| | |

REQUIRED DISCLOSURE:

Investment advisory services provided by NewEdge Advisors, LLC doing business as Marathon Financial Group, as a registered investment adviser. Securities offered through NewEdge Securities, Inc., Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, Inc. are wholly owned subsidiaries of NewEdge Capital Group, LLC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying to this message is strictly prohibited. If you have received this message in error, please immediately delete.

| Marathon Financial Group | 857-201-3420 | 131 Dartmouth St 3rd Floor Boston, MA 02116 | meetmarathon.com

| | | | |