|

Weekly Update (10-11 : 10-18) - Peak Rates

Hi All,

The terrible violence in Israel and Gaza that erupted over Saturday is very worrisome. While it may seem difficult to think about markets during times like this, it helps to understand that ultimately cooler heads are likely to prevail. We do believe that the violence will end eventually (hopefully sooner rather than later), and unless it escalates into a major world war, the regional wars of the past tend not to have a very big or lasting effect on the market. On average, the wars since 1950 have tended to bring the market down 5%, and the drawdown lasts around 47 days until a full recovery is made.

· Post September Fed meeting, the 10-year treasury rate has skyrocketed over 50 bps to the 5% level. Such rapid and unhinging moves in the bond market can cause temporary carnage in stocks. However, there are good reasons to believe that the worst is behind us now.

· Recent Fed Speak, most notably from Raphael Bostic who has mentioned he believes interest rate hikes are no longer necessary, have signaled the Fed’s desire to avoid a dire outcome for the economy (i.e., unnecessarily pushing the economy into a recession.)

· If we compare this period of inflation to other large increases in inflation, most notably Volcker-era inflation, we notice that Paul Volcker ended his war on inflation when inflation got down to 4%, not 2%.

· The arbitrary 2% target was chosen by Ben Bernanke when he decided he wanted to emulate New Zealand’s 2% target. Most research shows that inflationary expectations above 3% are problematic, but the evidence is not clear that 2-3% inflation is so bad.

· Our belief is that the Fed now understands that risks are more “two-sided,” meaning that it would be irresponsible of them to ignore the second part of their mandate, which is full employment. In order to keep achieving their goal of full employment, they will need to avoid an economic hard landing.

· Even if we are skeptical that the Fed is actually done hiking interest rates, run-rate inflation of 3-4% is far below the long-run returns we expect from stocks of 9-10%, meaning now is a great time to be investing new capital into the stock market.

· A recession does not look to be imminent, based on real-time data provided by the Atlanta Fed. Goldman Sachs points out their expectation of a recession in the next 12 months at 15% probability.

· Pepsi recently had a very good earnings report, with the stock rallying 2% on the news. If this is an early indication of how 3rd quarter earnings will be, we remain optimistic that earnings have bottomed out and should increase.

· Earnings will begin next week with the big banks reporting, most big tech companies will report in early November.

· Goldman Sachs has recently raised their earnings guidance to $250 of profit per share on the S&P 500 by 2025, or roughly a 10% increase from today’s level. Our view is that this is a good baseline estimate, and may prove too conservative.

· We believe it is possible that the worsening Federal Budget deficit is at least partially to blame for the “bond vigilantes” rejecting yields on the 10-year treasury in the low 4% range. In our view, Congress needs to work in a bipartisan way to sustainably solve budget deficits through some combination of raising taxes and limiting spending, so that the market stops questioning the creditworthiness of the US government.

· Our base case remains that, based on the data science, in “years like this” in which the market goes up 10% by midyear and with the regular seasonal choppiness in August-September, stocks tend to go up 8-9% by year end. We may have seen the beginning of this rally a few days ago.

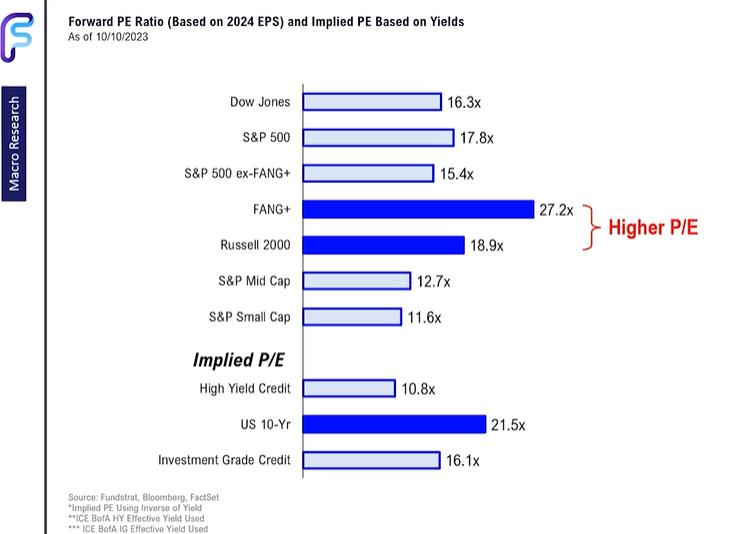

· The major financial news outlets continue to focus on the wrong narrative (high valuations) at the expense of the more nuanced argument that there is still tremendous value in the market. Ex-FAANG, the stock market is reasonably valued, and the FAANG’s deserve their premium multiples:

|