Hybrid Workforce

No surprise here. More people are spending more time working from home according to the Wall Street Journal. This is negatively impacting the office sector as companies (tenants) have less need for office space.

Inflation: Construction Costs

This impacts all product sectors, but to different degrees. Each suite in an office building is typically remodeled (tenant improvements) every five to ten years. What used to cost $40 per square foot now can cost $150+ per square foot. Multifamily, retail and industrial are not immune to this, but the impact is much less and is the least for industrial as it has the least amount of office space (typically 5-10% of the total square feet of a suite).

Inflation: Wages

Wage inflation continues. Multifamily has been impacted the most by this due to the significant number of people it takes to operate an apartment community. The income statement of a multifamily investment is structured in a way that these costs directly reduce the net operating income, and therefore value, of a multifamily investment. Not only does industrial not have the onsite staffing, but also Westcore’s industrial leases are structured as triple net (NNN). Cost increases flow through to the tenants in the form of additional rent and do not decrease the NOI as long as the building is leased. Our portfolio is 93% leased as of the end of Q2 2023.

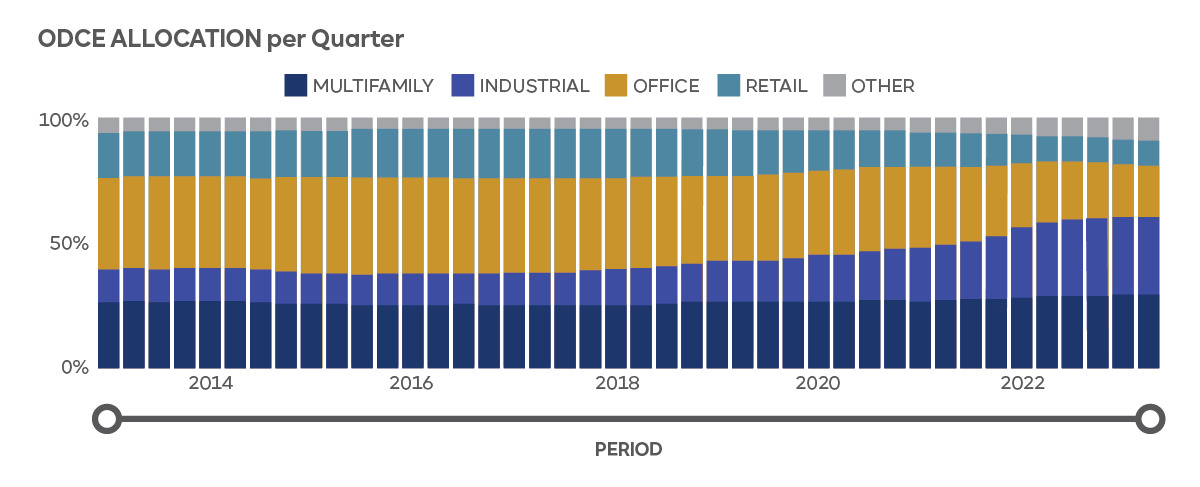

E-Commerce

The pandemic accelerated the adoption of e-commerce. As of Q1 2020, e-commerce retail sales as a percent of total sales were 11.9%. It peaked at 16.9% the following quarter and is 15.1% as of Q1 2023, a 27% increase over three years prior. [

source] This directly benefits industrial.

Onshoring & Inventory Build-Up

The pandemic showed companies the risk of manufacturing overseas and having a just in time inventory management approach. The term “just in case” came to replace “just in time”. Businesses created plans to bring more manufacturing and inventory to the U.S. This is not something that happens overnight. We are now seeing the effects of these changes as one of the drivers to the increase in demand for industrial space.

E-Commerce

There has been widespread adoption of e-commerce because of the pandemic, with online retail sales hitting 15.1% in Q1 2023, marking a 27% increase over three years. This directly benefits industrial.