What Your Financial Advisor Won't Tell You About..... Real Estate IRA!

You've heard it before for many years, "Buy low, sell high" The stock market has hit several all- time highs and is now heading towards a possible correction. As a registered investment advisor, I make a part of my living offering financial advise and offer diversified portfolios of stocks, bonds, mutual funds, and ETF's. I have a team of money managers to assist me. Therefore, I can spend the better part of my time on my real estate practice. I believe real estate can be a very solid investment to own over time.

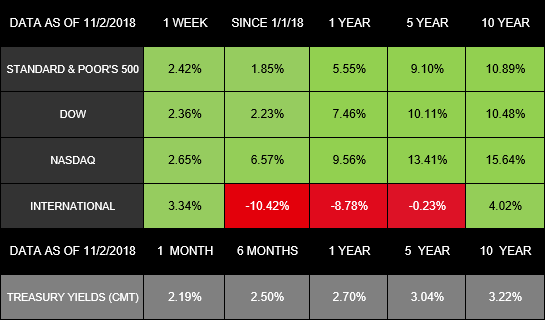

During the last recession, most investors lost a great deal (on paper) of their portfolios and retirement accounts. During this time, the markets continued to spiral downward hitting lows at a rapid pace. The Dow Jones Industrial Average hit 6,443.27 on March 6, 2009, having lost over 54% of its value since the October 9, 2007 high. Most of my investors took my advice during this time to stay the course. Eventually the markets would come back and then some. Today the DOW has topped nearly 27,000, currently just over 25,000.

I had met many investors from 2008-2009, (not my clients) mostly self-money managers, who came to me for advice after they had already sold off their investments at a loss. The stock market is paper money. It is not a tangible. Investing requires two important items diversification and discipline. If anyone of these investors had a part of their IRA invested into a Real Estate IRA, with a tenant paying rent (commercial or residential), most likely would not have sold off during this time. Why? Because they would have an income still coming in, and real estate is not "liquid" like other investments. Ironically, dividend stocks work the same way but some investors panic and sell off when they lose value.

Most brokers and investment advisors will not recommend investing your retirement directly into real estate. This is partially due to the fact that they cannot generate any commissions if your money is invested directly into real estate. Good thing about a self-directed IRA is that is you save on ongoing loads, fees, commissions,etc. on these types of investments. An alternate is a REIT (real estate investment trust) sold through most brokers and advisors. These high commission investments are generally sold with the promise of steady dependable income, steady or increasing value, and with little discussion of the fact that the investment cannot be sold on any conventional exchange. I prefer an investor to be in control of their investments. When setting up a self-directed IRA, you choose the investments. In a REIT, the managers choose this for you.

When investing into a self- directed IRA, you are 100% in total control of your real estate investment. However, the IRS has very strict guidelines that you will need to know and follow. You need to make sure you have the proper custodian holds your IRA funds, (some of the institutions will insure them through FDIC) and you will need to understand how you can generate income with the real estate once your IRA purchases the property. If you would like to know more about a "Real Estate IRA", please feel free to contact me.

*This is not an investment recommendation. You should consult with a registered investment advisor or broker for further information and/or prospectus.

Should I Invest Into A Home Warranty?

A home warranty can be a significant investment if you are purchasing or selling your home. Most home warranties basic packages range between $350 to $500 per year and require an flat service call (approx. $50-$100) fee for each repair, while home repair expenses without a warranty may costs hundreds or even thousands for every repair needed. Home warranties are popular among real estate transactions, as new homeowners want peace of mind that important repairs will be covered in their new investment, and sellers want to assure potential buyers that their home will be taken care of. Some of the home warranty companies will cover your home will it is "actively listed." This allows sellers have their own level of protection.

Buyers are most likely going to hire a home inspector after the purchase price has been negotiated. A typical air conditioning unit in Florida has a life of 10-12 years. If you have an older "functioning" air conditioner, it will most likely give comfort to the buyer knowing that you have offered to pay for the first year's warranty to include the a/c, pool pump, hot water heater, garbage disposal, and much more for $500 buck!

If the seller does not offer this within the purchase, you can negotiate this into the contract of purchase. In the end, if the sellers don't purchase the warranty, it is well worth the money for your protection.

River Strand Community- October Updates

In the month of October, 8 properties were sold in River Strand community ranging from $173,500- $875,000. Currently there are a total of 32 properties available including single family homes, coach homes, villas, and condominiums available to purchase from $185,000 to $879,000 .

If you reside in the River Strand community, be on the lookout for my monthly newsletter, which will provide further details of our beautiful real estate community. It will include market trends, local vendors, and much more!

If you, or you know someone who is looking to buy, sell, or invest into real estate in the near future, please contact us at Keller Williams On The Water. Michelle and I appreciate the opportunity to assist you with all your real estate needs!