Why are the ’23 YTD market gains so disproportionate?

Hi All-

We wanted to touch base with a mid-newsletter-cycle market update, given how much we are all being constantly bombarded with conflicting headlines right now. As usual, most headlines are negative, because ‘if it bleeds, it leads.’ Most of the economic/financial journalism input most of us get every day comes from mainstream journalism. And the most important thing to bear in mind regarding mainstream financial journalism is that it’s a business. It has no interest in whether or not you become a successful investor. Indeed, since so much of lasting investment success attends upon our ability to tune out the noise and continue to work our plan, it might be said that journalism—the ultimate noisemaker—is downright opposed to your success.

So let us share our view, which is rooted in facts and fundamentals. Some of this (if not all of it!), along with sources we reference, may seem quite dull, but that’s the point—we don’t rely on sensationalist mainstream journalism to inform our decisions.

Equity investors have been well-rewarded in early 2023. After a brutal one-in-fifty year in 2022, (bonds and stocks both sell off in any given calendar year, only 2% of the time) bonds have since regained their typical role as portfolio ballast and regained their income-generating properties. In spite of the uncertainty stemming from inflation, the war in Ukraine, and earnings, equity markets have climbed the wall of worry higher. As of today, we are about 8% higher than we were at the beginning of 2023. Believe it or not, such dramatic moves in the face of uncertainty are all too common in the equity markets, which is why we remain fully invested at all times. Markets are known to be the ultimate discounting mechanisms, typically looking out between one year and three years into the future, rather than lingering on the feelings and information of today, which is already been baked into prices.

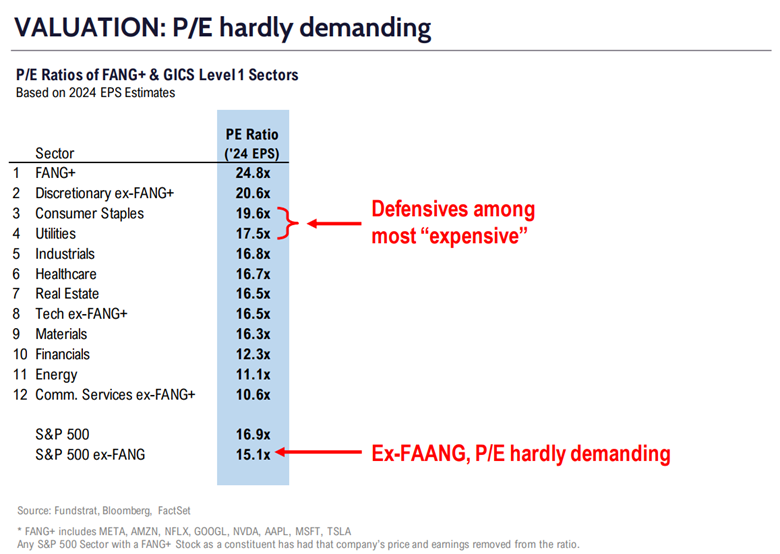

Equity markets are double-edged, they pre-price the good information and the bad, alike. Last year, we were on the other side of this unpleasant double-edged sword. Markets were fiendishly pre-pricing an earnings slowdown. Which, of course, this earnings season is bearing out, though not nearly as dramatically as the bears would have you believe. The “price-earnings pundits” who are so overly focused on the prices of this exact moment, are going haywire about the “valuation” levels of the markets not being supportive of where prices are at. They miss the overall point of the efficiency of markets as discounting mechanisms; and fail to appreciate that simplistic price to earnings valuations are poor intermediate timing tools. As we can see in the chart below – even if we buy into the erroneous assumptions the P-E pundits argue for, P-Es are not expensive, across the board.

|

|

If we pop the hood of the market, we can see there are still areas which have not participated as much as the FAANG (Facebook, Apple, Amazon, Netflix, Google) stocks. For instance, while the market overall is up 8%, quality small caps (vis a vis the S&P 600, VIOO is an ETF representing this basket), are basically still flat on the year. Similarly, large-cap value stocks haven’t performed too well so far, year to date. While it may feel frustrating in the near term that not all stocks are up as much as the S&P 500 (about 20 of the 500 stocks are most of the gain for the year, if not all of the gain—with Facebook/Meta and Nvidia each up ~100% YTD), investors would do well to remember that every stock in their portfolio is not meant to go up at the same time at the beginning of a recovery/new bull market. If all stocks went up exactly the same amount, and did so at the same time, said investor would not be well-diversified, and would lose a lot of money when it came time for these perfectly correlated assets to take a breather.

In this particular case, the characteristic that large-cap value and small and mid-caps share is that they are highly sensitive to the economic cycle. This can be expressed numerically by looking at a stock’s beta. A high-beta stock, suppose one that has a 1.5 beta, might be expected to perform better in a purely risk-on environment. Due to the characteristics of the market, we are in right now, especially given the turmoil in the small-bank segment, but also due to Fed Speak and inflation, we are not purely risk-on. We will not be in a risk-on state until the markets are clear on the direction and ending levels of interest rates, on the fact that the regional banking crisis is over, that the war in Ukraine is dissipating, that the self-inflicted debt-ceiling debacle has been dealt with, and that inflation has been finally conquered. However, since not all of these things will materialize at once, and we have no idea when they will materialize (only that they will, eventually), we find it appropriate to position for that moment now. Hence our allocations to mid & small caps, and large cap value.

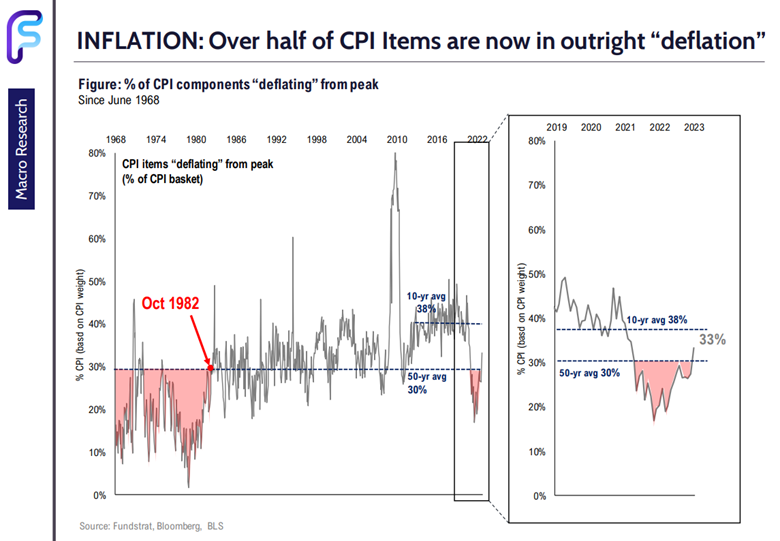

As an example, with JP Morgan’s recent takeover of First Republic, the market breathed a major sigh of relief. Of course, the market may not be 100% confident that the crisis is behind us until, well, it chooses to stop focusing on it, but let’s just say this feels like the best indication yet that the crisis, if we can call it that, is over. On days with lower volatility, where the market is purely focused on fundamentals, small-caps and more cyclical exposures with higher beta can do better. Believe it or not, there will be a day sooner rather than later, when most days go back to being like this. While we don’t think it is prudent to sell our large-cap growth exposure, because most of the stocks in this basket have yet to fully recover from the trauma of 2022, we do want to set our expectations that the other two baskets of US stocks (large value and mid & small cap), at some point, will start to carry the performance baton in a more meaningful way. Said differently, we believe that many of the meters of distance built into the wall of worry are being surpassed by the market climbing higher – and inflation may be the next shoe to drop – this would allow the other two sleeves of stocks we own to start participating in the bull market in a more meaningful way. Evidence is starting to skew decidedly in this direction and would include the fact that now over 50% of CPI (inflation) items are now in outright deflation (going down in price). By that same token, we should not wait until inflation has been dealt with before we invest, because if we look back at the Volcker era, stocks bottomed well before Volcker declared an end to the inflation war. See the charts below.

|

|

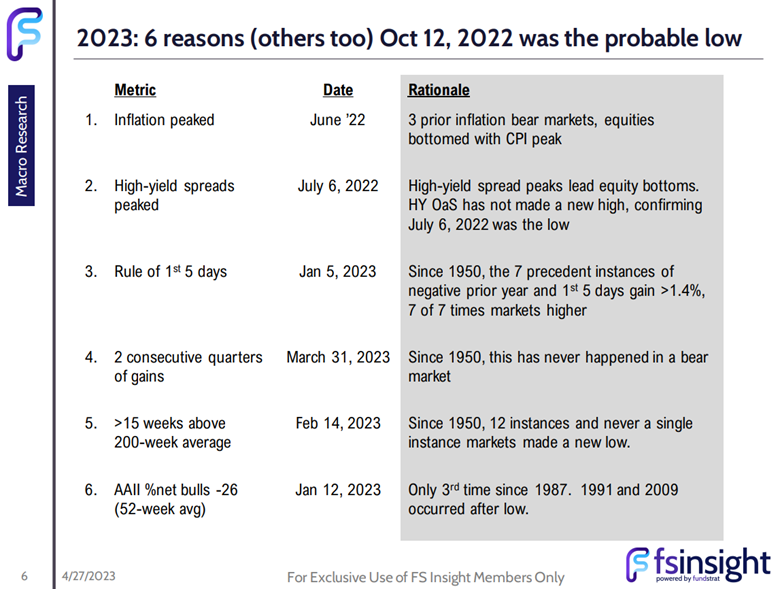

Small and mid-caps can typically do much better in a low-volatility environment, such as during the early and middle innings of a bull market. All of this makes sense, especially given that small and mid-cap stocks have not participated as much in the rally, when compared to their large cap growth counterparts. As we start to see the light at the end of the tunnel on inflation, investors should shift their portfolios incrementally to these fast-growing, but more capital-constrained high-quality stocks. So, what gives us confidence that we are indeed in a new bull market? While it is impossible to be sure, so early, our checklist of the below items provides a very solid dashboard for us to rely on, in terms of data that can help guide us to power through the volatility of last year.

|

|

As always, please do not hesitate to reach out to us with questions. Thank you for your trust and confidence.

|

|

Charles G. Brown

Chief Executive Officer, Financial Advisor

|

|

|

REQUIRED DISCLOSURE:

Investment advisory services provided by NewEdge Advisors, LLC doing business as Marathon Financial Group, as a registered investment adviser. Securities offered through NewEdge Securities, Inc., Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, Inc. are wholly owned subsidiaries of NewEdge Capital Group, LLC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying to this message is strictly prohibited. If you have received this message in error, please immediately delete.

|

Marathon Financial Group | 857-201-3420 | 131 Dartmouth St 3rd Floor Boston, MA 02116 | meetmarathon.com

|

|

|

|

|

|

|