Santa Cruz Real Estate

Digest,

Ed. 27

|

|

|

|

|

|

November, 2017 - In This Issue:

|

|

|

|

|

|

In This Month's Issue

|

|

In this month's Digest you will find national and local news as well as informational pieces on topics that we have found to be important in today's real estate industry.

With wildfires rearing up in Northern California, including in our beloved Santa Cruz County, we know that many of our homeowner clients and future homeowner friends are asking "What can I do to protect my Santa Cruz Real Estate?". Read below to find out.

Bitcoin

was just

used to purchase a piece of US real estate

. What is bitcoin and can it be used to buy real estate in the Bay Area? Read more below.

Both the Senate and House have released their versions of the "Tax Cuts and Jobs Act". Read this month's Legislative Corner to find out how your

mortgage interest

deduction

, estates tax, and affordable housing

will be affected.

As our article on buying a home with bitcoin illustrates, technology is making it possible to buy a home in novel ways. Read Christine's Corner to learn about a new home-buying assistance app that makes it possible to

crowdfunding your downpayment.

|

|

Real Estate Market Statistics

For Santa Cruz, Santa Clara, and

Monterey

The reports contain median home prices, real estate price statistics, valuable information about mortgage rates and much more.

|

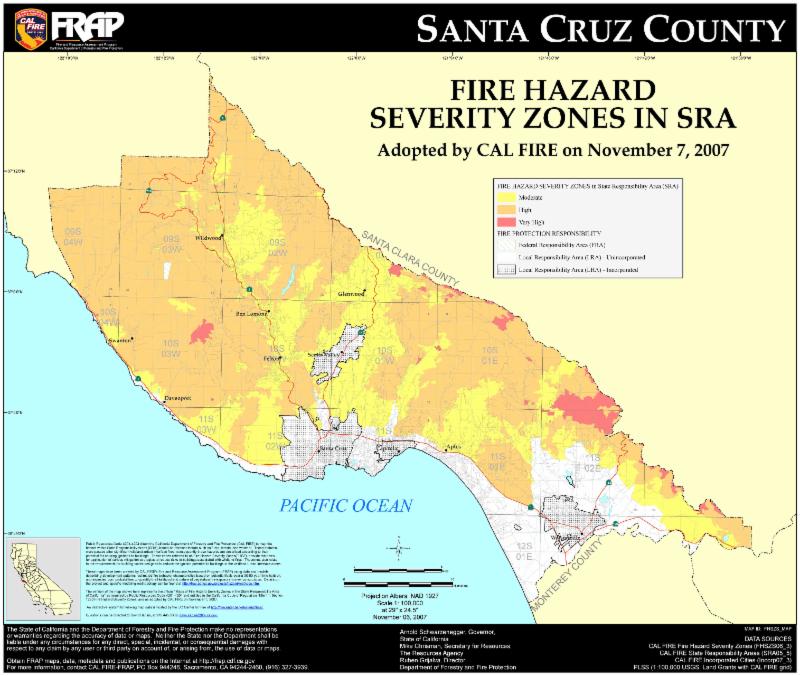

As reported in 2007 by CalFire, a majority of Santa Cruz county is in a moderate to high fire zone (

source

).

(click map for a larger version)

With wildfires rearing up in Northern California, including in our beloved Santa Cruz County, we know that many of our homeowner clients and future homeowner friends are asking "What can I do to protect my Santa Cruz Real Estate?".

This

guide

gives an extensive list of things you can do to prevent your home from catching fire.

This Santa Cruz County resident

serves as a good example of someone who has taken fire-safety very seriously. These kinds of preventative measure may become the norm in the near future. According to Nasa Scientist, Mika Tosca, with just a 1ºC change in global temperatures fires are predicted to increase from

100 to 600 percent

, and according to

projections

the earth is poised to warm another 1 to 6ºC. Unfortunately, no one can be 100% sure that his/her home is safe, but we can push the odds in our favor by taking steps to reduce the likelihood that our homes will catch fire.

Should a disaster strike your home, a key to fire-preparedness is to ensure that you have adequate home insurance. The typical homeowners policy* covers destruction and damage caused by a fire, including wildfires. This means that the insurance company will pay to rebuild or repair your home and remediate smoke damage. Quoted in this

article

, Amy Bach, executive director of United Policyholders suggests doing the following to calculate the right amount of coverage for your home:

"You can take your policy limit and divide it by your home's square footage to get a rough estimate. If the number is less than $200 per square foot, you're probably underinsured and should consider purchasing more coverage". Additionally, "make sure and have 'code upgrade' coverage, which helps cover the cost of bringing your new home up to the latest building standards".

Essentially, you want to estimate what a contractor would charge to rebuild your home from the ground up.

Additionally, this standard policy will usually cover the loss of belongings in a fire. How much insurance is enough when it comes to your personal things? Knowing the answer to this question entails taking and regularly updating an inventory of your present-day belongings and ensuring that your policy covers at least that amount. Taking an inventory will not only help you pick out the right policy, but should a natural disaster strike, it will enable you to prove the value of what you owned, and could speed up the processing of your claim. Furthermore, it will provide documentation for tax deductions that you can claim on your losses.

In today's world, taking an inventory is relatively easy. You can use your smartphone, camera, or video-recorder to record your possessions. In addition, be sure to write down descriptions of the items recorded, including year, make, and model numbers, when appropriate. For valuable items, you may want to have an appraisal to determine the item's worth. Don't forget to store your inventory somewhere where it can be easily accessed and will not be destroyed by a disaster. There are even

home-inventory apps

available, which, if synced with the cloud, will give you peace of mind knowing that your inventory is safe no matter what happens.

Finally, an important question to ask about your insurance company: how will my claim be processed? It's important to know how long you have to file a claim post-fire, the amount of time it will take to process the claim, and what information will be expected of you when you file. Read more about settling insurance claims after a disaster

here

.

*Be sure and check with your insurance provider to verify your coverage. We do not guarantee that these types of coverage are included in all homeowner insurance policies.

|

Bitcoin is a decentralized currency that is used to send money instantly to anyone around the globe with negligible fees. It relies on blockchain technology, which provides a level of transparency and reliability needed to foster trust amongst bitcoin users. To learn more about the basics of bitcoin and blockchain, take a look at this

video

. Why is this relevant? Because bitcoin was just used to purchase a piece of US real estate.

According to

this article

, a texas-based real estate brokerage has completed the first-ever sale of a real estate property in the US using bitcoin. According to the buyer's agent, Sheryl Lowe, the transaction was surprisingly quick and easy compared to transactions which require a middleman to verify and disburse funds. What makes this possible?

Typically when a house is sold there is a third party such as an attorney or escrow company that facilitates payments to all parties. This third party will collect and verify funds before disbursing them. With the blockchain technology that bitcoin relies on, funds are automatically verified before the transaction goes through.

There is a historical issue with bitcoin which may still be deterring sellers from accepting it. Experts note that bitcoin has been historically volatile, and with the time it take to perform inspections, negotiate contract terms, and come to final agreements, the seller is at risk of the value of their future assets (bitcoins) dipping to an unacceptable low.

Even so, we expect the application of blockchain technology will continue to grow, making it more likely that cryptocurrencies will play a role in real estate transactions of the future.

|

Legislative Corner

On Thursday, November 9th, Republicans in the Senate Finance Committee released an outline of their version of the "Tax Cuts and Jobs Act". Just one week earlier, the Republicans' congressional House Ways and Means Committee released the original version. Both pose a threat to homeownership as we know it today. Here is a short summary of how both may affect your real estate.

Mortgage Interest Deduction

The house bill will keep the mortgage deduction, however it will lower the maximum amount you can deduct from $1,000,000 to $500,000. The Senate bill will not change mortgage interest deductions, but both bills may make the mortgage interest deduction irrelevant for many.

The Senate bill changes the standardized deduction to $24,000 for married couples filing jointly and $12,000 for single filers and the House bill raises it to $24,400 for married couples and $12,200 for single filers. Both bills also eliminate nearly all state and local deductions while keeping charitable giving deductions. As a result, it will not make sense for most, besides the very wealthy and the very charitable to itemize deductions. (

source

)

Furthermore, under the House bill, homeowners will no longer be able to deduct the interest they pay on home equity loans, second home loans, nor any loan that is for a home other than their primary residence.

As a result, the incentive to buy and the tax-benefits of owning a home will be greatly reduced. Did you know that congress has been incentivizing homeownership with the tax code for over 100 years, primarily with the mortgage interest deduction? One thing is clear: these changes are poised to cause a major shift in the real estate market.

Estate Tax

The House bill will raise estate tax exemptions for single filers from $5.6 million to $10 million and repeal the tax entirely after six years. The Senate would raise the exemption to $11.2 million. This will largely benefit affluent families. According to the Joint Committee on Taxation, 99.8 percent of estates owe no estate tax at all. Currently, only the estates of the wealthiest 0.2 percent of Americans end up paying this tax because of the tax's high exemption amount, which has jumped from $650,000 per person in 2001 to $5.49 million per person in 2017. (

source

)

The house bill will eliminate the generation-skipping transfer tax after six years, while the Senate bill would leave it as is.

Affordable Housing

According to this

article

, the congressional tax plan will dramatically reduce affordable housing.

Last issue, we wrote about a CA affordable housing package. It consisted of over a dozen affordable-housing bills that were signed into law. These plans were predicated on the assumption that the tax-based federal financing mechanisms related to affordable housing would remain. The congressional bill would call for the elimination of tax-exempt private activity bonds, which developers use to finance construction that benefits low-income buyers. This poses a major threat to both these newly signed bills and pre-existing affordable housing programs.

The Senate's bill would not have as dramatic an effect, however it would reduce the value of low-income tax credits. As Michael Novogradac, managing partner of Novogradac & Company puts it:

"The House bill would drastically reduce the future supply of affordable housing, whereas the Senate bill would only damage it"

Do you agree with these changes? If not, let your representatives know.

|

Christine's Corner

Technology is making it possible to buy a home in novel ways.

Launched by CMG Financial, HomeFundMe is a crowdfunding website that allows family, friends, and others to contribute to your down-payment. One of the main advantages of using the site is that contributions are properly documented to ensure lenders accept the money as legitimate down-payment funds. According to the CEO of CMG Financial, the idea behind the project is not to fund the entire down-payment, but to add to the borrower's existing funds, possibly eliminating their need to pay private mortgage insurance.

There has been

criticism

about this kind of project. It essentially allows individuals and families with less equity to acquire more real estate. This may lead to borrowers who appear more secure than then they are, and increase mortgage-defaults. On the other hand, if borrowers have adequate income, but their savings are low due to high student-debt payments, lower income during the recession, or high rents in their local market (all issues faced by a large number of first time Santa Cruz home buyers), they will likely be strong borrowers who can benefit from this kind of program.

HomeFund Me could result in people, especially millennials, getting into homes sooner. This allows young families to start building wealth sooner and plant roots, both of which can lead to healthier communities. If you have a prospective first-time homebuyer in the family, and are interested in learning more, check out HomeFundMe.com. If you'd like to discuss creative down-payment solutions, give us a call.

|

|

|

|

|