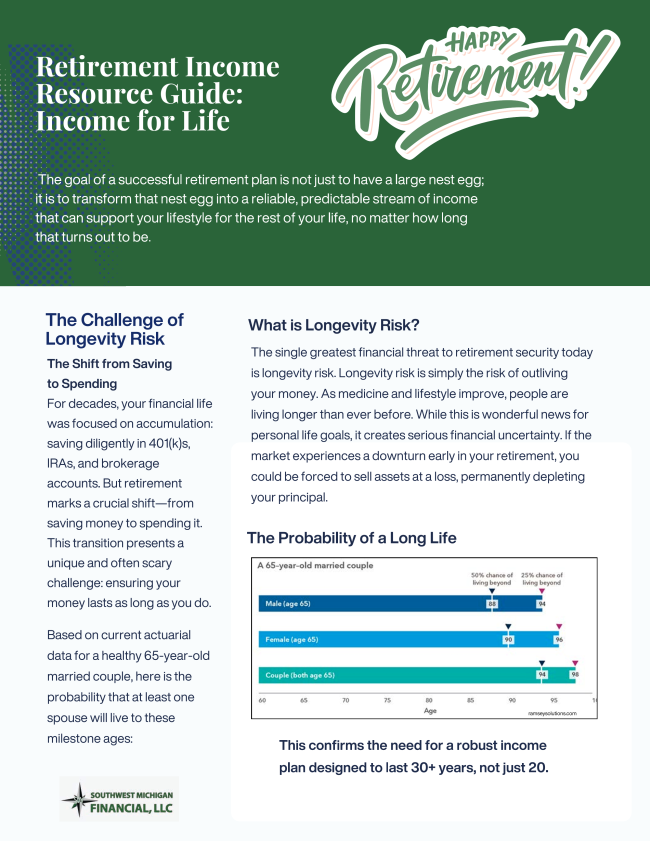

|

Got 15 minutes? Let’s talk Medicare

Medicare isn’t just health insurance—it’s a major variable in your retirement income math.

Here are the three most common questions we hear at the office:

1. “I’m 65 and still working. Do I HAVE to sign up for Part B?”

Justin Says: If your company has 20+ employees, you can usually delay. If you are at a small business with fewer than 20, Medicare typically becomes your primary payer at 65. If you miss this window, you could face a lifelong late-enrollment penalty.

2. “Why is my premium higher than my neighbor’s?”

Justin Says: This is likely IRMAA—a high-income surcharge. If your income from two years ago (like a house sale or a large RMD) was over certain limits, the government charges you more for Parts B and D. We can often appeal these if you have had a qualifying “Life-Changing Event.”

3. “Does Medicare cover my dental and vision?”

Justin Says: Original Medicare (Parts A & B) generally does NOT. To get coverage for things like glasses or dental work, you typically need a specific Medicare Advantage plan or a private supplement. We can help you compare these options to see which fits your budget best.

Still got questions? As fiduciaries, we believe clarity is the antidote to anxiety. Let us help clarify the Medicare enrollment process.

Want a free professional opinion? Call Justin today at (269) 323-7964.

|