|

|  |

|

|

Record Supply Met with Strong Demand

According to the latest Newmark U.S. multifamily capital markets report for Q2 2023, a record breaking 198,806 new units have been delivered halfway through this year. On an annualized basis this would be a 51% increase compared to 2022. Despite this incredible amount of new supply, the rental market has responded with an unprecedented surge in demand, absorbing 98,249 units—almost four times the figure from the first half of 2022! This robust demand is expected to continue through mid-2024.

Forecasts suggest even more substantial unit growth beyond 2025, although Newmark warns of a potential slowdown in new unit deliveries in the years 2026-2028 due to capital constraints. They expect that limited debt availability for new construction should begin to normalize deliveries. This could be even more dampened with a possible recession.

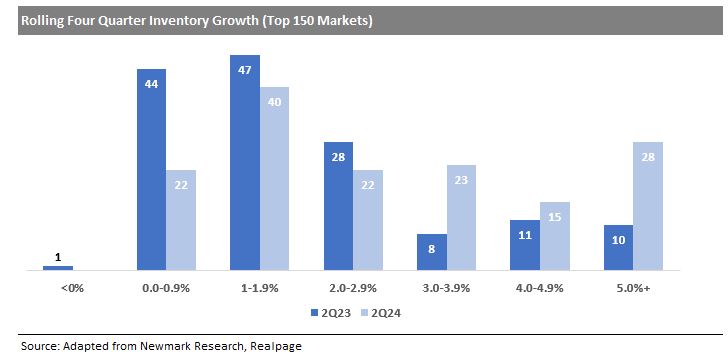

The report projects a 3.2% increase in the median market's inventory over the next 12 months, surpassing the previous year’s 2% growth. Inventory will increase by 5% or more in 28 markets, compared to 10 in the prior year. it's worth noting that while absorbing this influx of new supply may take several years, cities such as Austin, Charlotte, Raleigh-Durham, and Phoenix are poised to absorb the increase two to three times faster than historical norms.

This surge in new apartments has pushed the national vacancy rate to 5.3%, a still relatively stable number but the highest seen since 2014. The report also highlights that multifamily experienced positive effective rent growth in Q2 2023 compared to the previous quarter, albeit slowing, with year-over-year growth remaining below the long-term average. Notably, certain Midwestern markets and lower-income communities bucked this trend and continued to see strong rent growth.

In the face of slowing rent growth, landlords as also facing rising operating costs. Multifamily expenses increased 8.3% year-over-year. This was led by rising Insurance costs which soared 28.6%, with markets like Texas and Florida being particularly impacted. Additional costs, such as management expenses and property taxes, are also on the rise. Despite these headwinds, multifamily net operating income is anticipated to rebound, surpassing its long-term growth average of 2.3% reaching 2.7% in 2027.

| |

|

Edward M. Aloe

Founder and CEO

626-229-9057

| |

|

|

The Real Estate Wealth Podcast with Ed Aloe

We look forward to growing this initiative with your support!

If you’re interested in joining us for an episode, or have feedback, please let us know by replying to this message. We’re eager to hear from you and deliver quality content to satisfy all levels of investors!

| |

|

No sign of relief in housing even as the Fed holds rates steady

Until interest rates come down, affordability challenges will continue to strain the housing market: housing experts

In an elevated rate environment, the lack of inventory continues to be the biggest challenge for many potential buyers, the Mortgage Bankers Association said.

“While homebuilder sentiment is clearly impacted by the recent surge in mortgage rates, permits for single-family homes provide a positive outlook for the pace of construction in the year ahead. If mortgage rates trend down in 2024 as we anticipate, the combination of more homes for sale and somewhat lower rates should support stronger purchase volume,” Mike Fratantoni, SVP and chief economist at the MBA.

The MBA expects mortgage rates should begin to reflect that the Fed’s moves in 2024 will be cuts – not further increases. MBA’s mortgage finance forecast projected the 30-year fixed mortgage rate to decline to 5.4% in 2024 and 5.1% in 2025.

Powell also noted in a press conference that because people locked in “very low rate mortgages, even if they want to move now, that would be hard because the new mortgage would be so expensive.”

Rates are most likely to stay elevated until 2024, said Danielle Hale, chief economist at Realtor.com, thus putting a damper on the number of home sales transactions.

View Article Here

| | | |

|

Multifamily Weighs In on Another Rate Pause

Executives evaluate where it leaves the industry now.

Multifamily deals are still getting done and will continue to do so, executives say.

“Loan assumptions with favorable remaining term are attractive to investors and much easier to execute in the current environment,” Shay said. “I am finding other situations where seller expectations have come back in line with the new market cap rates. There is no shortage of capital waiting to be deployed, but in the higher interest rate environment, buyers need to bring more equity to the table.”

With debt coming due, there are also more workouts and distressed opportunities to be seen over the next 12 months to 18 months, Bordainick explained. “Owners have been hoping for rates to come back down and have been delaying refinancing or sale transactions, possibly buying extensions with their lenders,” he said. “I think owners are realizing rates may stay higher longer than they originally expected, so they are revisiting whether they have the runway to wait longer or whether they should transact now.”

View Article Here

| | | |

|

Multifamily Demand Remains Steady as Rent Growth Slows

According to the latest Yardi Matrix’s multifamily report, asking rents grew $7 on average last month, but year-over-year growth dropped 1.8%.

Down 70 basis points from May, year-over-year growth for multifamily asking rents fell to 1.8% in June, while the average asking rent increased $7 from the month prior to $1,727, according to the Yardi Matrix National Multifamily Report.

“Rents are growing within a normal seasonal pattern, albeit well below the post-pandemic boom and even below pre-pandemic trends,” Yardi Matrix analysts say. Rents were up $20, or 1.2%, in the second quarter and are up $23, or 1.4%, for the first half of the year.

Strong demand for units has kept rents afloat with occupancy rates remaining steady at 95%, Yardi Matrix reports. “Demand has remained strong, driven by the job market, which added 1.5 million jobs during the first half of 2023, and weak home sales, which are presenting a challenge to first-time home buyers,” states the report.

View Article Here

| | | |

|

About CALCAP

California Capital Real Estate Advisors, Inc., and its affiliate entities (CALCAP Asset Management, CALCAP Properties, CALCAP Lending, CALCAP Senior Healthcare, and CALCAP Strategic Opportunities, collectively known as “CALCAP”), is a California-based investment company founded in 2008 and headquartered in Pasadena, California. The Company sponsors alternative real estate investment opportunities focused on demographically driven housing. CALCAP has been able to consistently provide both individual and institutional investors with outstanding returns over the last 14 years. The Company uses a highly selective and disciplined investment approach, focused on delivering superior risk-adjusted returns. CALCAP currently has over $650mm in Assets Under Management. To learn more visit www.calcap.com.

Social Mission

CALCAP CARES is a 501(c)(3) private foundation organized to encourage employees to find a way to give back to the neighborhoods where we invest. CALCAP has created "GiveTime4Autism" as its initial program which gives employees the opportunity to donate unused vacation and sick days for a very worthy cause.

| |

|

LOS ANGELES

The Sanborn House

65 N. Catalina Avenue

Pasadena, CA 91106

SAN DIEGO

12626 High Bluff Drive, Suite 360

San Diego, CA 92130

PHOENIX

740 N. 52nd Street

Phoenix, AZ 85008

SANTA BARBARA

1309 State Street, Suite A

Santa Barbara, CA 93101

| |

|

Edward M. Aloe, Founder & CEO

(626) 229-9057

ed.aloe@calcap.com

Patrick A. Wakeman, Principal

(858) 764-4890

pat.wakeman@calcap.com

Drew Buccino, Principal and COO

(602) 419-3381

drew.buccino@calcap.com

Greg Blix,Dir. of Investor Relations

(805) 896-8500

greg.blix@calcap.com

| |

Mark A. Mozilo, Principal

(626) 229-9056

| | | | |