|

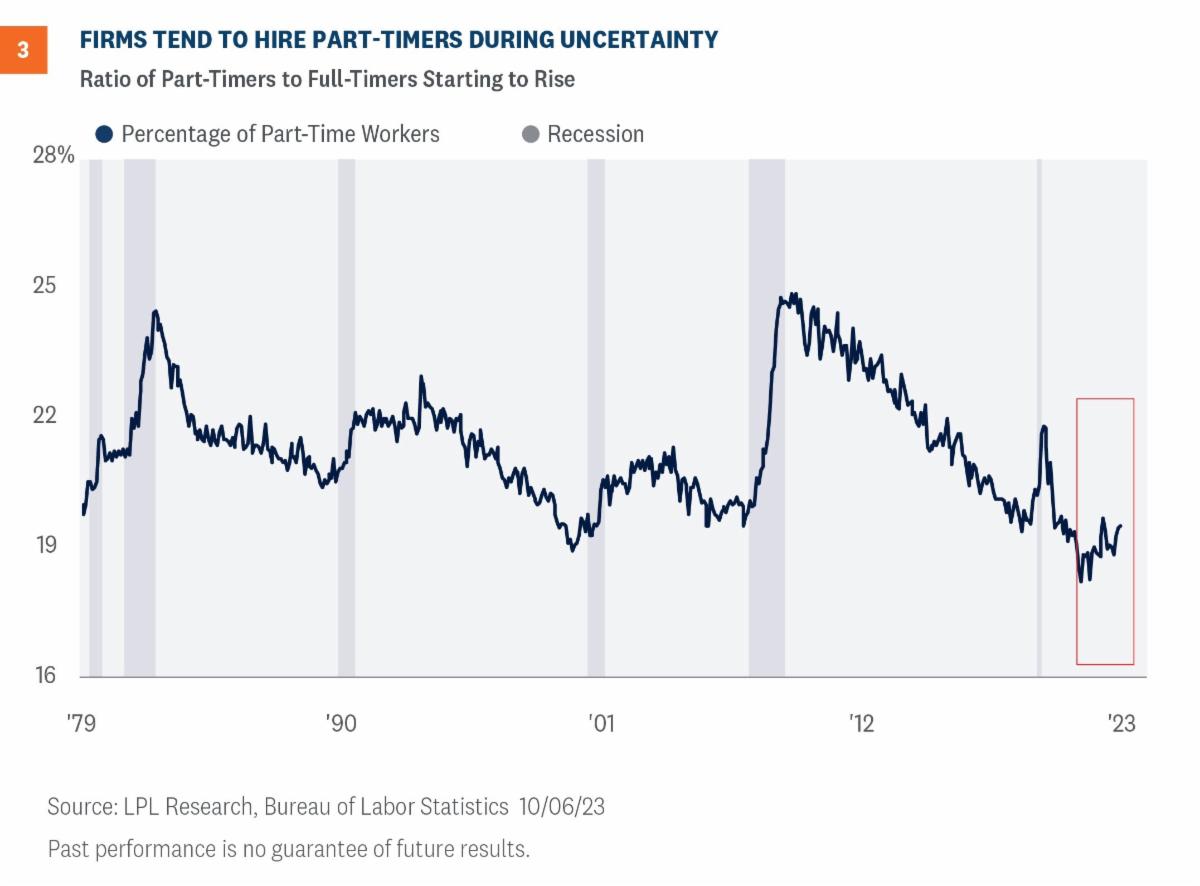

Despite headwinds, the U.S. could experience structural changes in the labor market, residential real estate, and inflation as the post-pandemic economy progresses into the New Year. As markets adjust to a new regime, investors should recognize the economy is becoming less interest rate sensitive and they should focus on leading indicators such as the ratio of part-time workers and not on lagging metrics such as the headline growth stats mostly cited in the media.

SETTING UP FOR A ‘EUCATASTROPHE’

J.R.R. Tolkien, author of the Lord of the Rings and famous member of The Inklings at Oxford University during the 1940s, coined a word—eu·ca·tas·tro·phe—to describe an event that turns out surprisingly better than expected. Frodo’s defeat sets up for an unpredictably successful conclusion.

One could argue that the post-pandemic economy had a few moments when things turned out better than expected. The economy grew faster than expected in recent quarters, unemployment remained historically low, and some sectors such as homebuilders have boosted activity despite the macro headwinds. The tight labor market seems to be a boon for workers, and one could argue that workers have never been in a better position to bargain for better pay and more benefits, but more on that later in this piece.

As investors navigate the final quarter of the year, the Federal Reserve (Fed) has pushed the fed funds target rate up 5.25 percentage points to reach an upper bound of 5.50%. And as inflation pressures ease, the fed funds rate will essentially become more restrictive, enough for the Fed to pivot from a tightening bias to a more wait-and-see approach. The Federal Open Market Committee (FOMC) members are starting to view the risk of overtightening to be in balance with the risk of insufficient tightening. Inflation has become less sticky, especially as services inflation cools. The large rise in shelter costs was a key driver of headline inflation in recent months but its impact will likely wane in the near future. Rent prices are off their peak according to industry reports, and investors should know that there is a sizable lag in time between a reported movement in industry rental data and the official government metrics.

Core inflation excluding shelter is more benign. Clearly, the inflation experience on homeowners is quite different than the experience felt by renters. Looking ahead, investors should carefully watch commodity prices for insight on how the Fed will act in future meetings.

RECESSION OR NO RECESSION?

From an investment standpoint, the “recession call” may end up being irrelevant. A recession could still emerge as consumers buckle under debt burdens and use up their excess savings, but a Fed sensitive to risk management might provide the salve necessary for more risk appetite. Investing is a relative game, meaning the U.S. could experience the 3 Ds of an economic contraction—depth, diffusion, and duration—but at the same time, still outperform other markets and hence, still be an attractive option for investors looking for calculated risk. A shallow recession would likely provide a “eucatastrophe” for the domestic markets, as a recession would bring the labor market into better balance and would increase the odds of the Fed cutting rates. History shows that markets tend to rally as the Fed moves away from a tightening bias.

WHAT WILL INVESTORS LIKELY CONFRONT NEXT YEAR?

First, investors will confront a Fed increasingly committed to the other part of their dual mandate—stable growth. As highlighted above, inflation will still hover above the 2% long-run target and remain a concern, but the Fed will be less laser focused because the trajectory is going in the right direction.

Investors will enter a new era for rates. If the economy slows as predicted, the Fed will likely start discussing plans to cut rates. But those cuts may not come until the second quarter of 2024 and the magnitude of cuts may not be anywhere near as aggressive as markets thought just a year ago. We could see the fed funds target rate approaching 4.50% by the end of 2024, thereby suppressing both mortgage rates and the 10-year Treasury yield.

The mantra of “higher for longer” indicates market expectations that the Fed will avoid the mistake it made in previous periods when the target range bumped down against the zero lower bound. When rates are that low, the Fed could feel restricted if a major financial crisis emerges and policy makers have one less tool at their disposal to create accommodative financial conditions. Despite the potential for a recession, the Fed will not be inclined to aggressively cut rates and should keep rates higher throughout the year.

Second, investors will confront a real estate market reeling from the unintended impacts of hybrid work and high borrowing costs. One unintended consequence of hybrid work is an economy less sensitive to interest rates. Historically, tighter monetary policy translates to higher mortgage rates, slowing the real estate market, and cooling house prices. In 2024, investors will still see a slower real estate market but not much normalization of home prices because of lean inventory and buyers coming to the closing table with cash. As households move from higher cost of living areas to lower, many with home equity use cash to purchase a new home, thereby skirting the credit markets. Perhaps we are in a new era for residential real estate.

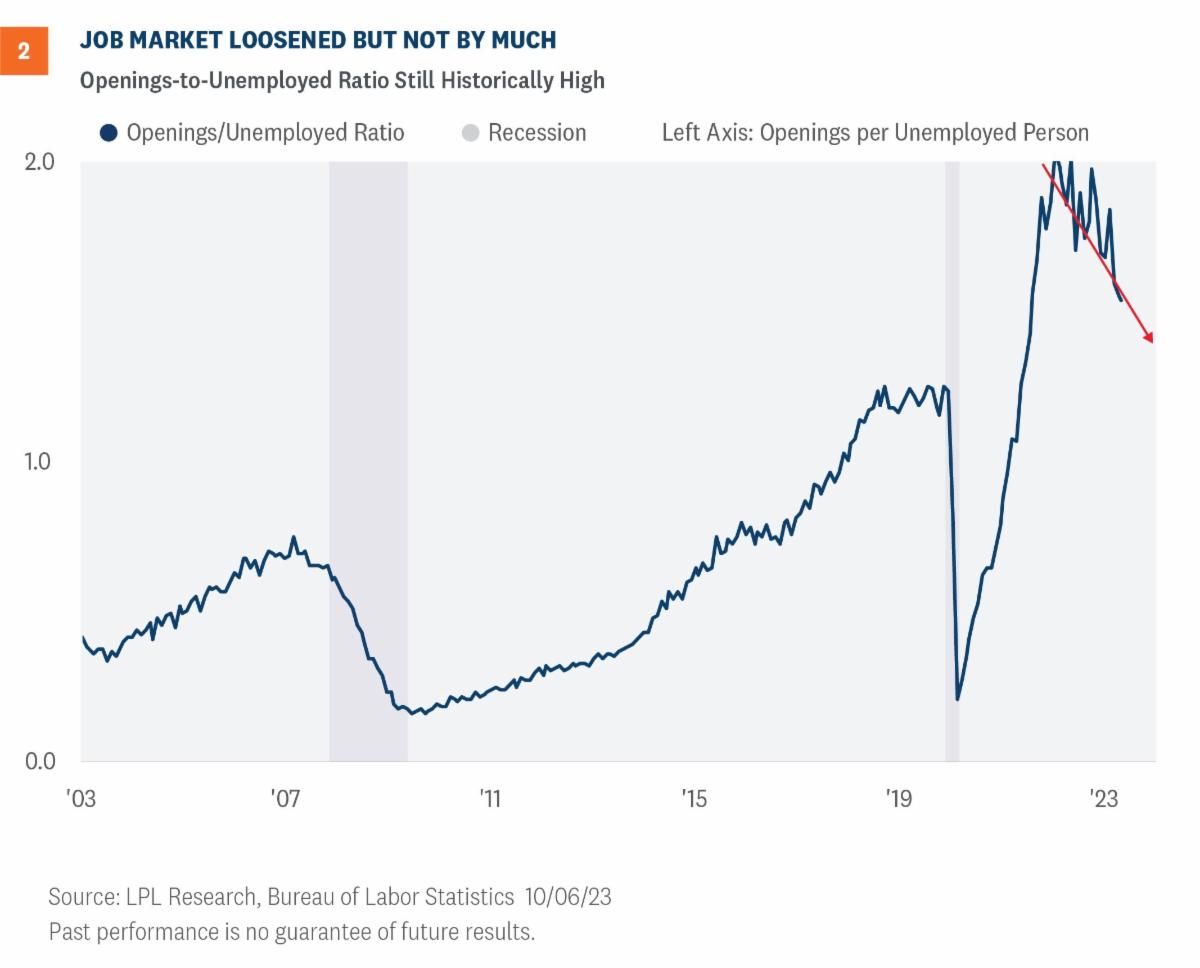

Third, investors will confront a new era for the average worker. Some call this the democratization of the workforce since never before have workers had this much in their favor. As the American worker has had a few years to adjust to the hybrid work model, we should continue to see a fair amount of turnover. Some have seen the fastest way to higher pay is moving to a new job. As shown in Figure 1, the growth rate for job switchers has never been this wide. Of course, the hybrid model can only operate in some sectors.

|