June 2020 Newsletter Vol.1

=+=+=+=+=+=+=+=+=+=

02 July 2020

Covering northeast railroads and ports, and their related operational, technical, legal, and government environments.

©2020 Rails & Ports Media

|

|

Contents

02.July.2020

PAR: For Sale!

CN: Looking to revive eastern traffic

FGLK: Rebuffs latest efforts to push Massena lines sale through

MCR: Current operator Coastal Rail wins ownership in auction

G&U: Completes main line connection to CSX Milford Secondary

CN: Port de Quebec Laurentia container terminal wins shipper support

CN: Heavyweights request STB reconsideration of Massena condition

MBTA: Signs Keolis to Commuter duty through 2026

MCR: Major track work in the midst of auction

CSX/CN: Petition STB to back off of Massena approval condition

MBTA: East-West Passenger Study being dispatched south?

CP: Full details of CMQ integration

|

|

28 June, Billerica MA -

PAN AM SYSTEMS ENGAGES BANK OF MONTREAL (BMO) TO FIND A BUYER FOR ITS RAILROAD BUSINESS. MANY BIDDERS EXPECTED TO MAKE OFFERS FOR ALL OR PARTS OF THE ~1700 MILES OF TRACK AND RELATED ASSETS RANGING FROM MATTAWAMKEAG ME TO DERBY CT TO ROTTERDAM JCT. NY.

|

|

Pan Am Southern (PAS)/Patriot Corridor partner Norfolk Southern has often been touted as an imminent buyer. WATCO reportedly reached an agreement to purchase PAR several years ago, only for the prospect to whither away. Canadian Pacific’s primordial interest in (PAR’s formative lines) Boston & Maine (B&M) and Maine Central (MEC) has fed the rumor mill from time to time.

What’s changed?

It’s been a tough year for all of the region’s railroads, apart from the industry’s nationwide malaise. The northeastern network has been impacted by the CN strike, a wintery Spring, First Nations blockades, and the Covid-19 pandemic. Pan Am’s own special 2020 event was the partial cave-in of the Hoosac Tunnel. The bill for repairs and detours reportedly amounted to $10 - $20 million.

|

|

Umpteen million Pan-Am sale rumors have circulated through the years, and several quietly contrived deals have only narrowly failed, but this is the first time that the “For Sale” sign has been put in the window.

|

|

Speculation has also flown for years that PAR majority owner Timothy Mellon, 78 years-old (and perfectly spry by all accounts), has long been considering his exit from the Guilford/Pan Am adventure. His ferment may have turned recently, when the Washington Post reported on certain unpleasant ideas promulgated in Mellon’s 2015 self-published autobiography,

panam.captain

. (Lesson of Life: If you are the reclusive sort, don’t publish an autobiography.)

Perhaps, with so much of the region’s network already in play, this is just the moment Pan Am ownership has been waiting for to make their exit.

|

|

What’s it worth?

Between 1981 and 1984, Tim Mellon bought B&M, MEC and Delaware & Hudson (D&H) for a total of $40 million, forming the Guilford System {panam.captain}. Essentially, that was net liquidation value. Insiders have suggested Mellon promptly got the money back by selling rights to fiber-optic lines.

The recent $8.4 billion sale of Genesee & Wyoming was at a 40% market premium over G&W’s public market value at the time. In 2012, the core assets were acquired from RailAmerica for about $2.5 billion. At the closing of the Brookfield acquisition, G&W had over 15,000 miles, yielding a per-mile value of ~$560,000. At that rate, Pan-Am’s ~1700 miles would fetch $952 million.

In November, Canadian Pacific agreed to purchase the 481-mile Central Maine & Quebec railroad for a reported $135 million, equating to ~$281,000 per mile, half of the G&W price.

Establishing a given railroad’s value is a little more complicated, as it must rationalize the value of assets, and the value of an income stream. Because Pan-Am is privately held we do not know its profit, but Tim Mellon is reported to have said that the company has never lost money.

Railroads have a wide spectrum for valuation. At one end is the net liquidation value – the expected return on sale of the assets. The premium over that base is calculated on traffic volume, revenue, operating and maintenance performance, and track condition. The first one may raise Pan Am’s stock as its mainline traffic density is higher than most shortlines; the last one may hurt the valuation, as much of Pan Am’s track mileage is in mediocre condition. Other factors such as port access or the ability to save costs by combining operations will influence the valuation.

Two major kinks in valuing Pan Am are the Massachusetts state-owned track mileage, over which Pan Am has the rights to operate for free. Also the Pan Am Southern line, jointly owned with Norfolk Southern, is the very spine of the Pan Am System.

|

|

Who are the real bidders?

(The following is based on exclusive information and educated speculation:)

|

|

Norfolk Southern

- Has a long interest and partnership in Pan-Am Southern. But in a PSR world Pan-Am’s lower margin paper traffic and low density network are less attractive.

- A well-placed NS source claims NS is not interested.

- The company currently does not appear to have the financial or management resources to take on such a project.

- BUT wouldn’t they have done it by now?

|

|

WATCO

- Has demonstrated its interest in Pan Am during a near-miss acquisition.

- Very familiar with PAR operations and management.

- Has made quiet inroads into New England, handling switching at PAR Maine paper customers.

- Has an ongoing relationship with NS.

- Known as a quality operator, respected by customers and employees.

- Loads lots of Western produce traffic; Pan Am runs adjacent to many Eastern grocery and food service warehouses.

- Has particular expertise in developing trans-load operations, of which Pan-Am has few; potential new channel of business.

|

|

Canadian Pacific

- Their public comments show interest in expanding.

- They have free cash to make a purchase, and have just shown by their CMQ purchase a willingness to pay the current valuations.

- They already connect with Pan-Am at both ends, Mechanicville NY and Mattawamkeag ME

- Haulage Rights over Vermont Rail System provide additional links from Whitehall NY and Newport VT.

- There isn’t much current CP - PAR interchange, though there has been historically, with both B&M (at Wells River) and MEC (at St. Johnsbury).

- One could imagine autos, intermodal, grain, ethanol and containers from Port of Saint John NB flowing to Pan-Am points.

- BUT would the STB approve a CP purchase of Pan-Am in light of the earlier purchase of CMQ? Irving would loose choice in routing to NS and CSX (although presumably CSX could provide that).

|

|

Canadian National

- Long track record of purchasing neighboring regionals.

- Reportedly been visiting strategic PAR customers.

- Has cash available.

- Looking for port access in the east, and has stated an interest in acquiring more track and linking to additional population centers.

- Naugatuck CT to Halifax NS would make a nice intermodal route.

- BUT CN does not connect with Pan-Am at any point. Unless New ENECR and SL&A were purchased from G&W is addition, then Pan-Am improves the value of NECR and SL&A by feeding additional traffic, offering a shortcut to Worcester and adding access to the port of Portland ME.

|

|

CSX

- Runs a high-density parallel mainline in Massachusetts, and a cluster of southeast MA lines

- Selkirk regional gateway

- Outflank NS with superior service on both corners of the eastern seaboard

- BUT would the transaction wouldn’t pass STB muster?

|

|

Brookfield Asset Management (G&W)

- Brookfield and G&W both have their own histories of strategic acquisitions.

- PAR is a natural fit with G&W owned NECR, CSOR, P&W and StL&A. It would give Canada – Worcester traffic off the NECR a significant short cut.

- Shop facilities at Worcester, Saint Albans, and Waterville could be combined.

- There is plenty of money to fund an acquisition.

- Brookfield, BMO, and CN are all members of a very small club in Montreal.

- Would a PAR purchase be folded into G&W, or “loaned” to CN — or remain independent?

- BUT would the STB allow a combination of PAR and NECR/CSOR/P&W/SL&A dominating New England? It would reduce competition in Southern Maine and the Connecticut River Valley (neither of which represents a lot of traffic).

|

|

Fortress Investment Group

- Highly-regarded former CMQ management is coincidentally available for their next project (Maybe. Ryan Ratledge has relocated to Texas)

- Pan-Am comes with property and passenger train opportunities that may be uniquely attractive to Fortress. Fortress has expertise developing property and implementing innovative ideas.

- Fortress likes to buy properties they can fix up and increase value – Pan-Am can certainly use fixing up, BUT can its value go any higher?

|

|

New Brunswick & Maine (J.D. Irving Ltd.)

- Irving is expanding in Maine and New England. PAR lines would fit well with JDI paper and wood products Boston and New York markets.

- Has expressed interest in expanding its rail business.

- Not known for paying high prices.

Patriot Rail, International Rail Partners, R. J. Corman, OmniTrax

- These shortline holding companies are in the market to expand and might pay high prices.

|

|

Split It Up?

Pan-Am might well be worth more, and would attract a wider array of shoppers, if two or more buyers could just bid for the parts they want. Energetic local railroads might be able to digest some of the spur lines, which would benefit from shortline-style attention to customer service. The States of Maine, Massachusetts, Connecticut, and even New Hampshire might take the opportunity to secure certain lines in support of long-term transportation objectives. The STB might more readily indulge Class I mainline ambitions if it felt that spur lines wouldn’t be left to whither, or that a reliable in-yard switching contractor would handle the customer service.

Hail Mary?

Who's to say that a western road isn't looking at ways to reach across the continent? While PAR is port-poor, its grasp of inland New England might eventually coax/force a merger with an Albany - Chicago routier.

Editor's note: ANRP will be covering the Pan Am sale in full detail through its conclusion. Hang on!

|

|

CN: EASTERN LINES GROWTH A PRIORITY

|

|

19.June, Montreal QC — Canadian National Railway is banking on growth in consumer products and supply-chain diversification in Asia to revive traffic on its underutilized eastern Canadian rail lines, according to CEO Jean-Jacques Ruest.

In an interview with Reuters, Ruest said that leading suppliers are turning to alternative (non-Chinese) Asian manufacturing sites. “The tariff war and coronavirus have intensified and accelerated these trends,” said Ruest.

A shift in the business mix, combined with container expansion projects planned for ports in Montreal, Quebec City and Halifax are key to reviving eastern traffic. “CN is very focused to repurpose that network, which is in great shape and only running at 50% capacity,” Ruest said.

The company is betting on more consumer freight shipping through the Suez Canal to North America’s east coast. Thirty percent of CN’s 2018 revenues were from consumer products; CN’s consumer franchise has grown nearly 28% between 2014 and 2018, double the rise in the company’s commodity and resource business during those years. Commodities generated 65% of CN’s revenue in 2018. {Reuters}

|

|

CSX: FGLK KEEPS UP PRESSURE TO UPHOLD MASSENA CONDITION

|

|

25.June, Washington DC -

FINGER LAKES DEFENDS STB'S HONOR FROM CSX AND CN'S GASLIGHT PETITIONS TO ABATE CONDITION OF APPROVAL.

|

|

Finger Lakes Railroad filed a Reply to B&LE (CN) and CSX's Petitions, requesting the Board to abate its own demand to modify the Massena Lines Purchase and Sale Agreement's (PSA) section 5.14(b), which has been deemed anticompetitive. The Board's Decision No.4, issued 06.April, imposes a Condition of Approval, requiring CSX and CN to modify the section that precludes the Buyer (CN) from

ever

contracting for access to FGLK or NYSW.

Despite their "best" efforts to negotiate a compromise since then, CSX and CN have announced that they are unable to devise an agreeable modification, and on 05.June filed Petitions for the Board to drop its objection to section 5.14(b) as originally composed. If the Condition of Approval is not abated, the Principals warn that the transaction will be cancelled.

In its 25.June Reply to [CN and CSX Petitions], FGLK asserts that the Board must reject the Petitions on procedural and purview grounds, arguing:

[Neither] Petition meets the Board’s standard for granting reconsideration under 49 CFR §1115.3(b), which specifies, "a petition for reconsideration will be granted “only upon a showing of one or more of the following points: (1) The prior action will be affected materially because of new evidence or changed circumstances. (2) The prior action involves material error.”

Neither B&LE nor CSXT has presented any new evidence or changed circumstance that would suggest that the Board’s prior analysis of the anticompetitive effects of Section 5.14(b) was materially wrong ...

What has changed?

Re item 1, concerning new evidence or changed circumstances, the Reply cites the B&LE Petition's assertion that the proceedings are affected by "changed circumstances and new evidence of the parties’ inability to propose a response to the Board’s Condition ..."

To which FGLK replies:

By choosing not to comply with the Board’s Condition, B&LE and CSXT have left the Board with the same PSA that it analyzed previously ...

[Their lack of response] to the Condition cannot be considered new evidence or changed circumstances justifying reexamination of the Condition.

Re item 2, concerning material error, the Reply cites the CSX Petition's assertion that, “[i]t would be material error for the Board to withhold approval of the Massena Lines sale,” based on the Board’s concern for long-term future competitive impacts.

FGLK rests its reply on the Board's "extraordinarily broad authority," the possession of which the Board itself explicitly reminded everyone in Decision No.4:

[The] Board has long exercised its conditioning authority to resolve competitive concerns caused by minor transactions,

and that in this case,

Section 5.14(b) is a provision “of the type that the Board has cautioned requires heighted scrutiny” because it is a “total ban” that “extends into perpetuity.

|

|

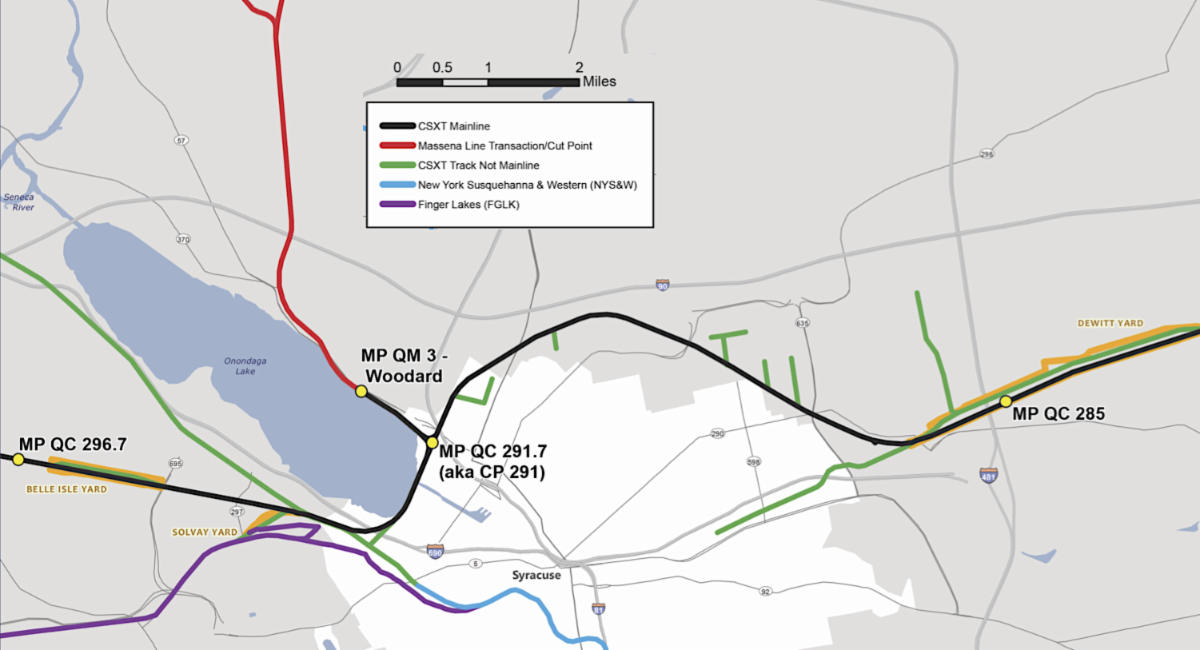

Syracuse brings together

CSX, FGLK, and NYSW. The two shrtlines connect on their southern ends with NS, offering a good alternative route south for Massena lines, as well as access to the Fulton and Baldwinville tracks to Port of Oswego on Lake Ontario. Section 5.14(b) of the Massena Lines Purchase and Sale Agreement between CSX (Seller) and B&LE/CN (Purchaser) from ever establishing an interchange with FGLK or NYSW.

|

|

MCR: SPIRITED AUCTION ENDS WITH COASTAL RAIL OWNERSHIP

|

|

19.June, Denver CO —

INCUMBENT OPERATOR COASTAL RAIL WINS 61-ROUND BIDDING WAR OVER (G&U OWNER) FIRST COLONY

19.June, Denver CO —The Mass Coastal Railroad property was acquired by an affiliate of its current operator, following a 61-round bidding war. The gavel was dropped after First Colony Development and Rail Holdings Company declined to counter Coastal Rail LLC’s final $2 million bid. First Colony’s final bid was $1,985,000.

On 17.June, William A. Brandt, Jr., Chapter 11 Trustee, for the San Luis & Rio Grande Railroad, Inc. (a/k/a, Iowa Pacific Holdings) accepted Coastal Rail and First Colony submissions as the only qualified bids ($1,046,309), following his review of several bids submitted by the 2359 hrs MST 16.June (0159 hrs EST 17.June) deadline.

The auction

At 0900 hrs MST 19.June (1100 hrs EST) Trustee Brandt commenced the auction to award the San Luis & Rio Grande Railroad, Inc. 100% LLC membership interest in the Massachusetts Coastal Railroad. The auction was held at the Denver offices of Markus Williams Young & Hunsicker LLC, with the participants appearing via Zoom conference call.

The sixty-first bid ($2 million) was submitted by Coastal Rail and accepted as the Purchase Price. In the absence of a timely response from First Colony, the Trustee selected the final bid by Coastal Rail as the highest and best bid.

Sale to conclude 01.July

At 1232 hrs, the Trustee filed his Report of Auction with the U.S. Bankruptcy Court for the District of Colorado, stating that he will seek the approval of the sale of the 100% membership interests in Mass Coastal to Coastal Rail LLC at the hearing scheduled for 01.July.2020 at 1400 hrs MST (1600 hrs EST).

The Trustee has selected First Colony as the Back-Up Bidder at a Purchase Price of $1,985,000.00. In the event Coastal Rail fails to close in conformity with the Sale Order and the Bidding Procedures, the Trustee will seek at the 01.July sale hearing schedule to approve the sale of the 100% membership interests in Mass Coastal to First Colony {Trustee’s Report of Auction, Case# 19-18905-TBM, 19.June.2020}.

|

|

G&U: COMPLETES LINE REBUILD, CONNECTS SOUTH WITH CSX

|

|

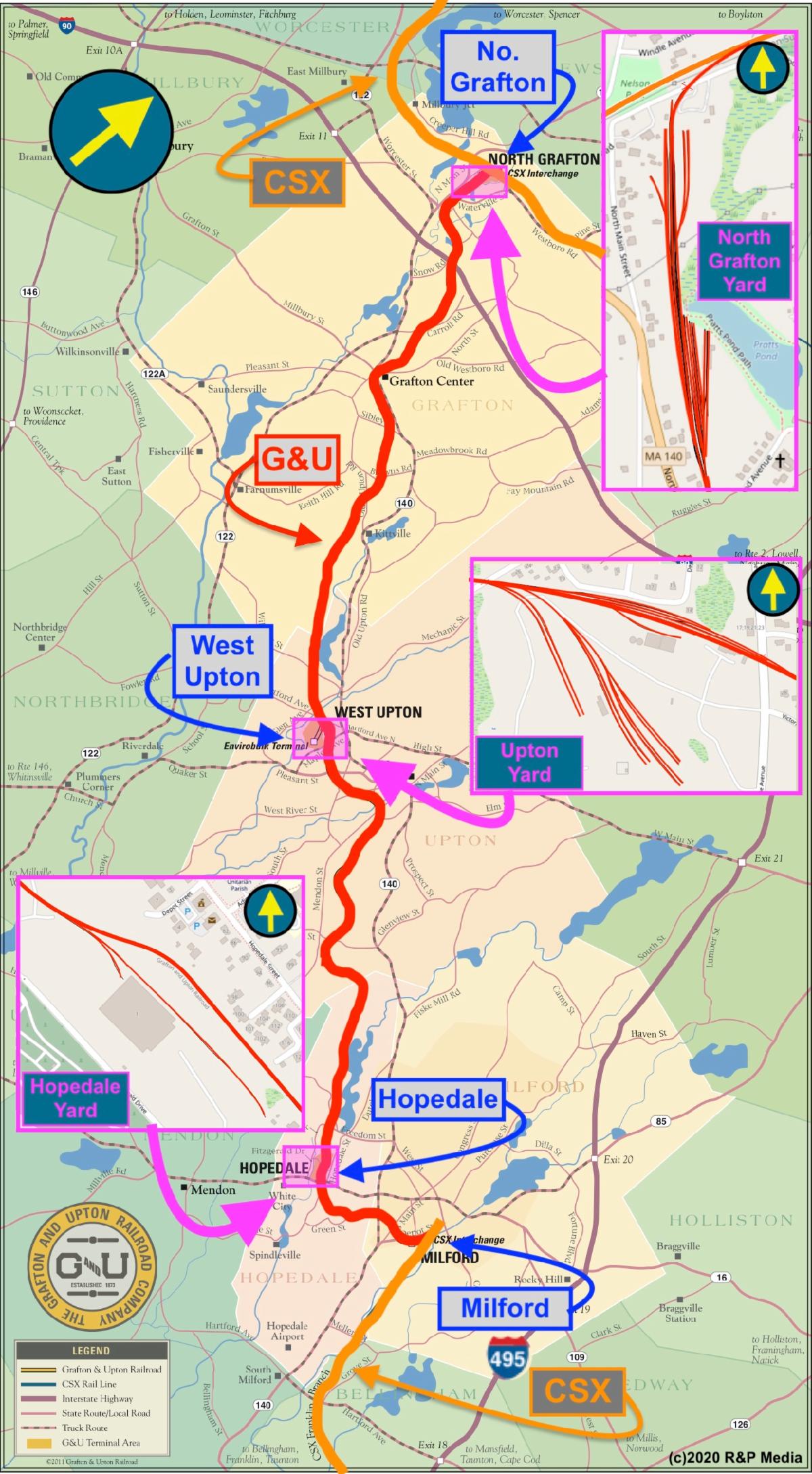

18.June, Hopedale MA —

GRAFTON & UPTON DRIVES GOLDEN SPIKE TO CELEBRATE RECONNECTION WITH CSX/MBTA MILFORD/FRANKLIN SECONDARY, WITH PLANS TO LEASE AND DEVELOP THE 16-MILE STRETCH.

Hopedale MA G&U celebrated the completion of track building on its entire historical ROW, with a Golden Spike ceremony connecting the south end of its line to CSX and MBTA. The ~8,000 ft of Class III mainline track from Hopedale to Milford (

completed 12.June - Ed.

) restores a segment of railroad last saw service in the early 1980’s, and the track was mostly removed after 2009 to rehabilitate the roadbed.

|

|

Golden spike marks return

of rail service between Hopedale and Milford via G&U main line. In 2009, G&U was acauired by First Colony Development, initiating a rebuild of the line between Grafton to Hopedale. The condition of the Hopedale - Milford stretch precluded completing the rebuild at the time. G&U pulled most of the ~two miles of track (85# rail), and started by rehabilitating the roadbed. The new track is 115#, and rated at 286K {Jennifer Al-Beik}.

|

|

Planning and preparation

In his management report on the Milford project, G&U General Manager John DeWaele wrote, “During the Q4 2019 project planning phase, GU coordinated all materials, equipment, and services needed to undertake construction of the Hopedale to Milford segment [in the Spring 2020, including seven] thousand tons of stone, nearly 1,000 relay ties, and other GU materials reclaimed from other locations. These were delivered to the site by GU’s own equipment. Vendors delivered 4,800 additional ties. Also in the past year, GU reconstructed the Hopedale St. steel bridge to 286K capacity (with outside help).

The Milford project kicked-off on 2.March.2020 after more than a year of planning and engineering. Preliminary work in the Fall of 2019 included construction and installation of two 115# No. 10 turnouts, realignment of the main, and laying of a 1,600 ft run-around in Hopedale, to serve as a staging area for the Milford project, due to the narrow ROW in Milford. The run-around will support future switching.

After completion of the run-around track, GU started its 8,000 ft march to Milford. Cropped and drilled rail was arrayed along the ROW; ties were set; rail was spiked; ballast was dumped and spread. GU used their own equipment and manpower to perform all job functions associated with building the new track.

First and goal

Reaching Milford, GU rebuilt a two-track grade crossing, timing the asphalt contractors to minimize delays to crossing traffic. Another 115# No. 10 switch was installed off the interchange, in order to maintain prospects for the Milford yard. Finally, in coordination with Keolis Commuter Services, the GU mainline was tied into a switch on the Milford Secondary (owned by CSX, leased to MBTA for Franklin line commuter service).

This connection, completing the nearly 2 miles of new construction, reopened freight service beyond Hopedale for the GU to lease freight rights to 16 miles of CSX track from Milford to Franklin, giving GU more customers and land to develop for new railroad customers.

Building customers, teams, partnerships

In the midst of the Milford reach, GU landed Ciment Quebec to the Hopedale facility as a railroad customer. This included building 700 ft of new track, installing a new switch, all which was done by GU staff and equipment within a three-week period. GU completed this work and was able to refocus on the Hopedale to Milford segment. GU has also secured Charah fly ash and a glass recycler as new customers.

At the Golden Spike ceremony, DeWaele emphasized that the accomplishment was a true team effort by the entire G&U community: “The project was made possible through our dedicated staff of railroad maintenance of way and construction employees. Further, GU’s project manager and Roadmaster with over three (3) decades of construction experience as well as equipment operators; not only for this project, but the future projects GU intends to complete in coming years. We’ve developed a diversified staff of highly experienced individuals.”

On 23.June, with Worcester line service suspended for signal work, the new G&U track carried two MBTA trainsets to/from Boston for maintenance.

Once at Milford the train entered the lightly used former New Haven line, and proceeded to Boston via the Franklin Line.

{G&U Manager's Notice of Completion, John DeWaele,12.June.2020; editor's correspondence with G&U President Michael Milanoski, 25.June.2020.}

|

|

CN: LAURENTIA CONTAINER TERMINAL TO BE READY IN 2024

|

|

12.June, Quebec QC —

QUEBEC SHIPPERS SUPPORT NEW CONTAINER TERMINAL. ADVANTAGEOUS LOCATION PROMISES TO PROVIDE FASTEST SERVICE TO MIDWEST VIA CN.

Port de Québec, CN, and Hutchison Port Holdings (HPH) have won support of dozens of shippers for their Laurentia container terminal project, which promises to open in 2024 as the most efficient facility for delivering Atlantic container traffic into the continental heartland.

Shippers who have publicly announced their intent to utilize the Laurentia site include Congebec, Resolute Forest Products and Breton Tradition 1944, and the Association Québécoise de L’industrie de la Pêche (AQIP), whose 54 members represent more than 90 percent of the marine product volume processed in Quebec {insidelogistics.ca, 15. June.2020}. Other supporting shippers have demurred from publicizing their support.

|

|

Laurentia will expand upon the existing Port de Quebec

facilities, adding substantial container capacity to efficiently serve ~13,000+ teu vessels. From cranes to straddle-loaders, all container-handling equipment at the terminal is expected to be operated automatically. Five on-dock loading tracks will feed a shunting yard designed to dispatch 12,000 ft. trains. {Port de Quebec; annotated by R&P.

|

|

Big vessels need a big terminal

Port Laurentia and the Quebec Container Terminal is a planned expansion of the PdQ’s existing Beauport facility. Lengthening the wharf line by 610 meters will enable docking 13,000 teu Neopanamax container ships, and processing up to 500,000 teu/yr. Container handling will be entirely automated from quay to railcar or truck chassis. Loaded rail strings will be assembled into road trains up to 12,000 ft long.

The terminal will leverage the PdQ’s existing 16-meter depth, year-round open water, and CN’s efficient routes to midwestern cities.

The Laurentia project is squarely targeting existing container traffic flowing through Halifax NS, Norfolk VA, and the Port of New York/New Jersey. Closer to home, the Port of Montreal is concerned about the impact the new port will have on its current volume. One report estimates that Quebec could take around 190,000 containers from Montreal. “We fear the creation of overcapacity in container handling on the St. Lawrence. We would end up with underused facilities. No one would be a winner in [such a] situation,” said Sophie Roux, Port of Montreal VP-Public Affairs.

The growth of Atlantic container traffic should however mitigate this impact. In the last several years, trans-Atlantic container volume has been growing at the expense of Pacific traffic, due largely to the U.S. - China trade war. If that trend were to continue, North Atlantic trade would absorb Laurentia’s added capacity. But with the radical slowdown in the wake of the Coronavirus pandemic, all ports will be struggling to regain their previous traffic levels, and competition will be fierce.

|

|

CN: OCEAN CARRIERS AND TERMINALS URGE STB TO OK MASSENA

|

|

29

.June, Washington DC -

TEN

MAJOR SHIPPING LINES, TERMINAL OPERATORS,

AND A COC

REQUEST STB TO RECONSIDER THE COMPETITION CONDITION IMPOSED ON THE MASSENA SALE.

American Container Lines (ACL), Hapag-Lloyd, Evergreen Shipping, CMA-CGM, Maersk,

MSC

shipping lines, Holt Logistics, Maher Terminals, General Container Terminals (GCT) port operators,

and the North Country Chamber of Commerce

sent Letters of Support for the CN/CSX Massena Lines sale to proceed, without the approval condition imposed by the STB in its 06.April Decision of Conditional Approval. The letters urge that the Board reconsider the condition for approval it placed on CN's acquisition of the Massena lines from CSX, requiring the parties to propose a modification or elimination of Section 5.14(b) in the parties’ executed Purchase and Sale Agreement.

All of the letters were composed as follows, or used very similar language:

Dear Ms. Brown,

We are writing today in support of the Bessemer and Lake Erie Railroad Company’s (“CN”) request for partial reconsideration of Decision No. 4, served on April 6, 2020 to the Surface Transportation Board (STB). As a customer using the new joint-line CN-CSX service between New York/New Jersey/Philadelphia and Canada announced in August 2019, we respectfully ask the Board to approve this request so the transaction can move forward.

We were excited about the STB’s approval of the Transaction on April 6. The new interline CN-CSX intermodal service has created an opportunity to move containers over the Massena Lines to Canada. We understand after the Transaction, the interchange between CN and CSX on the Massena Lines will move from Huntingdon, QC to Woodard, NY with an opportunity to improve transit times over the Massena Lines by 24 hours. We are concerned that these anticipated benefits will not be achieved if the Transaction is not able to move forward.

We respectfully ask the Board to approve this partial reconsideration request. We look forward to working with B&LE/CN and CSX to grow intermodal traffic moving by rail and thus remove trucks moving over highways. Thank you for your time and consideration.

Respectfully,

(Signed)

|

|

MBTA: EXTENDS KEOLIS COMMUTER PACT TO 2026

|

|

15.June, Boston MA -

MBTA BUYS STABILITY TO 2026 WITH PRE-EMPTIVE DOUBLE EXTENSION OF KEOLIS CONTRACT, WITH MODIFICATIONS. COMMUTER TRANSFORMATION PROJECT SAFE FROM POTENTIAL PROCUREMENT PITFALLS.

|

|

MBTA’s Fiscal and Management Control Board approved a 4-year extension of the Commuter Rail Operating contract between the MBTA and Keolis Commuter Services, LLC, through June 30, 2026. The current contract expires in 2022, and includes two two-year renewal options. The parties have agreed to both options, and to apply the terms of the extension to the remainder of the existing contract. All tolled, the new agreement will pay Keolis up to $2.56 billion in operating costs and $97 million in capital costs through June.2026.

Keolis has been the MBTA’s contracted Commuter Rail operating partner, providing all mechanical, transportation, and engineering services, according to the terms of an eight-year contract signed 01.July.2014, and due to expire 30.June.2022. The contract included options for two two-year extensions through 2024 and 2026. The MBTA’s contract with Keolis is performance-based with the contract including a fixed price for a certain level of service and penalties related to on-time performance and passenger comfort.

Stability paramount

Among other significant benefits, the extension provides cost certainty in a challenging market with the MBTA paying less than the current market price for the contract, and avoids a potentially disruptive transition that might come with a re-procurement and a new operator.

MBTA General Manager Steve Poftak explained the decision as meeting the MBTA’s “[Main] goals … to provide continuity and the best possible service for our Commuter Rail customers, as well as provide adequate time to plan for a future transformational procurement.” Poftak detailed additional system improvement incentives incorporated into the extension agreement (detailed below - Ed.).

David Scorey, CEO and GM of Keolis Commuter Services said that the “extension balances taxpayer and passenger needs as it keeps costs low while also enhancing the passenger experience.”

Transformation looms

In addition to weathering the dramatic drop in ridership during the CVD-19 pandemic, and maintaining the pace of two major route expansions (Green Line Extension and South Coast Rail), the T is preparing to transform its underlying commuter rail business model to run much more frequent service.

Transformation will bring major changes in the operating arrangement, perhaps adopting characteristics of European franchise agreements, in which the operator takes the lead in initiating service changes and benefiting from increased ridership, (or losing, if plans fail).

New incentives

This 4-year extension now also includes a number of additional incentive benefits that include:

- Additional performance payment incentives for improved on-time performance, train crew staffing, and seating capacity. These performance incentives are worth a potential total of $5 million per year in fiscal years 2021-2026.

- Additional measures to address fare evasion/non-collection, including the installation of automated fare gates that will significantly reduce ticketless travel. Staffing incentives expand the number of conductors onboard to check tickets.

- Incentives to accelerate capital investments in MBTA railroad infrastructure and assets that include early phases of Rail Transformation.

- Increased fleet availability and reliability through improved management of Mechanical Parts in fiscal years 2022-2026;

- Flexibility and time to develop transformational successor contract, with the possibility of re-procurement as early as 2025.

Momentum

Since the start of the contract, Keolis has added 10,000 more trains per year, including new weekend train service, piloted routes, and other services; has deployed customer technology that enables passengers to pay for tickets onboard with credit and debit cards; and has reinforced safety management protocols that include an expanded and updated Safety Department.

{mbta,com, 15.June.2020}

|

|

MCR: WORKING ON THE RAILROAD, DESPITE DISTRACTIONS

|

|

14.June, E. Wareham MA —

COO PODGURSKI DETAILS TRACK WORK UNDERWAY, THOUGHTS ON IMPENDING SALE, CAPE COD EXCURSION AND DINING TRAIN PLANS.

Cape Rail LLC head Chris Podgurski submitted these responses to ANRP questions:

ANRP: Are Cape Rail crews and equipment keeping busy during the shut down?

CP: MassDOT-Rail currently has several projects underway on the Mass Coastal Lines.

- Crosstie Replacement Program on the Cape Main along Buzzards Bay. The program also includes the Falmouth Secondary, and a small stretch on the Middleboro Secondary.

- Eleven Crossing Safety Systems upgrade by Saratoga Signal nearly finished.

- Twenty-two Grade Crossing surface replacement being performed by Manafort Transit.

- CWR Change Out-Upgrade on the Framingham Secondary which begins this month.

Currently the MC is conducting its system-wide vegetative maintenance program. We will also be doing some brush cutting on the lower Cape Main. We’ve also made some timber & tie replacements on “Otis Branch” leading into the Mass Military Reservation.

ANRP: Is the impending sale affecting operations?

CP: With regard to the impending sale, it’s obviously an ongoing process. And to be completely transparent, the MC doesn’t really have any actual assets to speak of. And it curiously exists on 100% State-owned properties. To make it even more “risky” is the fact that it currently operates on what remains of a L&OA Extension which expires September of 2021. Then the owner of the MC faces the ever-popular RFR Process.

ANRP: How are the non-freight operations preparing for this all-bets-off summer?

CP: With regard to the Cape Cod Central (wholly owned subsidiary of Cape Rail LLC) , Director of CCCRR Passenger Operations, Kaylene Jablecki is attempting to pull off an “Alchemy Process” of 2020 Season. Our start date has been illusory! Currently we’re trying to discern the ok to operate between food service trains and our excursion trains. As mentioned previously we’ve treated the equipment and facilities with Anti-Microbial “Perma-Safe”. Please check out www.capetrain.com for our latest updates.

|

|

CSX/CN: BOTH ASK STB TO WITHDRAW MASSENA SALE CONDITION

|

|

05.June, Washington DC —

CSX AND CN FILE SEPARATE PETITIONS WITH STB, ASKING BOARD TO SAVE MASSENA DEAL BY REMOVING THE INTERCHANGE CONDITION IMPOSED ON THE SALE'S APPROVAL.

CSXT and CN submitted separate Petitions for Reconsideration of the STB’s 06.April conditional decision on the sale of the CSX’s Massena Lines to CN subsidiary Bessemer & Lake Erie Railroad. The Petitions request the Board to remove the condition relating to Section 5.14(b) of the P&S. In May, CN and CSX jointly announced that they were unable to modify their agreement to suit the Board’s condition.

The CSXT Petition notes that, in its 06.April decision, “The Board did not find any evidence of current competitive harm from such an end-to-end line sale…” and that the Board “recognized the public benefits that would result from the sale.” The Petition asserts that based on those findings, 49 U.S.C. 11324(d) mandates Board approval of the sale as agreed between the parties. Based on this analysis, the Board should have approved the line sale without the condition relating to Sn. 5.14(b).

They've got a point

“[The] Condition … is inconsistent with both the law and policy … [in that] the mere possibility of unknown and unidentifiable future competitive impacts does not justify withholding approval of a transaction that will bring concrete and immediate benefits … It would be material error for the Board to withhold approval of the Massena Line sale based only on such speculative future effects.

“[Perhaps] the Board intended to instruct the parties to see if they could reach an agreement on changes to Section 5.14(b) … [It] is now clear (

since the May joint announcement suspending negotiations - Ed.

) that the transaction will not proceed without removal of the Condition.

“As CSXT and CN/B&LE pointed out in their prior comments, the restrictions in that PSA provision only apply to “Buyer” (B&LE and CNR). Section 5.14(b) does not preclude a direct connection between B&LE and shortline railroads in the Syracuse area; it only precludes Buyer from seeking such a connection. If market conditions lead shippers or other railroads to desire a direct connection with B&LE in the future, nothing in Sn 5.14(b) prevents them from pursuing such a connection.”

The CSX Petition further asserts: “[The Board’s] Condition is premised on protecting a sophisticated buyer, B&LE, from voluntarily negotiating away its own rights … But [according to the statute] the Board … should focus on potential harms to competition, not harm to particular competitors.

CN won't concede, but wants the sale

B&LE’s filing states that the parties have been unable to agree on a proposed response to the Board’s Condition, and the Transaction is in jeopardy unless the Condition is removed, and that work toward integrating the Massena Lines into the CN system has halted. Likewise, B&LE’s proactive efforts to hire employees and work with Rail Labor have ceased.

“B&LE/CNR agreed to Sn 5.14(b) because absent doing so, they would have no Transaction at all.”

Beyond the labor protection requested by the parties and imposed by the Board, the Transaction as structured by the parties would have additional benefits for CSXT employees on the U.S. Massena Lines.

At this point, unless the STB reverses its position on the condition, the transaction will be negated and CSXT will continue to hold ownership and operations of the Massena Lines. {STB Docket No. FD 36347}

|

|

MBTA: EAST WEST STUDY OUTREACH GENERATES OUTRAGE

|

|

Commentaries on the MBTA's handling of the East West Passenger Rail project.

10.June, Boston MA -

MBTA OUTREACH PRESENTATION SPARKS PUSHBACK ON LOW RIDERSHIP AND HIGH COST PROJECTIONS.

Following the release of an insiders' presentation, numerous advocates and interestd individuals have bombarded MBTA with incredulous looks at its calculation of dismal ridership numbers and exorbitant construction costs.

Christopher Parker analyzes the background of the prospective East West Passenger Rail project:

Western Massachusetts has felt little benefit

from the red-hot Boston economy. Expanding Springfield — Boston rail service appears a logical way to mitigate the diparity: link underemployed communities to economic opportunity, open up affordable housing options for professionals priced out of the Boston market, and provide an asset to spark locally grown economic growth for Western Massachusetts.

The state has been aware of the urge to expand public transportation westward, but a poor relationship with CSX has been considered an insurmountable obstacle. CSX has made it clear it does not want MBTA trains on its freight mainline west of Worcester. In recent times, CSX ran 4 intermodal and 5 merchandise trains each way; that frequency has been considerably reduced by precision scheduled railroading (PSR).

Existing Conditions

The circa 1830s Boston & Albany route is “tough railroading,” according to an experienced railroad man, and not fit for high speed. Top historical speed was 70mph; it is 60 mph today. Historically, passenger trains took four hours between Albany and Boston. Now, Amtrak’s Lake Shore Limited 448/449 takes six hours to meander through Wellesley, Natick, and Framingham, up the Worcester Hills to Brookfield, and over the Berkshires to Pittsfield.

Studies

Intercity travel markets were estimated in 1995 by the American Travel Survey which found significant travel between Albany and Boston, Hartford and Boston and New York and Worcester, but relatively less Springfield — Boston travel.

The 2016 Northern New England Intercity Rail Initiative (NNEIRI) regional service conceptual planning study included the route relative to a New York to Montreal route. The study projected that eight daily round trips between Connecticut, Springfield and Boston would generate 107,200 riders from western to eastern Massachusetts; establishing Springfield — Boston service would cost $273-309 million, primarily to double-track Springfield — Worcester, and make capacity improvements at Worcester Union Station.

The state’s study

In 2018, MBTA commissioned the $1 million dollar East West Passenger Rail study to evaluate six alternatives for improved Pittsfield — Boston service, ranging from a new high speed end-to-end line, to a hybrid route with connecting Springfield — Pittsfield bus service.

In February of this year, the study authors released ridership projections that are much lower than those anticipated by multiple advocate organizations. The study’s projections yield an exorbitant cost-benefit ratio that makes the project untenable. Advocates protested: former Commonwealth Transporation Secretary Jim Aloisi tweeted, “The East West Rail report contains such questionable modeling that it's being viewed as wholly unreliable & deliberately negative".

The study team returned last week with higher revised numbers, primarily the result of extending their estimated 20-mile radius of ridership for each station to include the City of Northampton and U-Mass Amherst, two obvious wells of ridership that had been counted out on the first pass. Estimates of induced ridership were also changed. Those changes multiplied the ridership projections to more realistic levels.

Advocates also question the study’s cost estimates, which are dramatically higher than the NNEIRI study and other independent estimates. Much of the expanded estimated cost increase reflects acceptance of CSX’s expected demand that any higher speed tracks be built much further from the existing line than the original second track was, promulgating property acquisition, earthmoving, wetlands mitigation, and new bridges. The study makes no suggestion of challenging the CSX demand, despite there being numerous current, valid precedents of similar projects utilizing standard 14-16 ft wide ROWs.

|

|

J

oshua Coran analyzes the veracity of the Study's evidence:

The Massachusetts East West Passenger Rail Study: Analysis of Proposed Infrastructure Costs

By Joshua Coran

Rail Users’ Network, and

Director of Product Development and Compliance, Talgo, Inc.

Infrastructure

The fundamental problem [with the MBTA East-West concept] is that the existing infrastructure dates from 1831 - 1833. At that time “high speed rail” meant 15 mph. The presentation on 06.February identified nine “key constraints” as follows.

1. Complex at-grade crossings near Framingham

There are only four road crossings in Framingham on the Boston Subdivision main line. Six CSX freight trains and 54 MBTA passenger trains cross two of them every week day; 42 trains of them also use the latter pair. They are protected with flashers and gates. It is unlikely that the twelve or fourteen additional trains proposed will be sufficient to trigger the need for additional protection.

2. Capacity Constraints Worcester to Springfield

This issue will be the most difficult. CSX is an enthusiastic participant in “precision scheduled railroading,” [meaning that the schedule of] a very long, slow and heavy freight train [will impact MBTA’s schedule]. [It] is not clear why this constraint is limited to east of Springfield. In the case of Alternative Three, CSX will certainly insist on capacity improvements on the Springfield – Pittsfield segment as well. [Replacing] the 47 miles of second main track that Conrail removed will increase capacity more than enough to compensate for that consumed by the proposed passenger trains. Eight additional universal crossovers (and related signals) will be required. Quandel Consultants, a small but long standing and well respected firm, has provided estimates for this work (including upgrading to 90mph) of $191.8 million

3. Heavy passenger and freight use poses capacity constraints to new services

The graphic presenting this constraint pointed to the segment east of Worcester. There is little freight in this stretch (and none at all east of Framingham). West of Framingham there is always at least 25 minutes between MBTA passenger trains, even during peak hours; the existing infrastructure could easily handle twice the service plus any freight now on the rails or anticipated. East of Framingham one time each weekday two MBTA trains are only ten minutes apart, and another pair are twelve minutes apart, but the average headway during the peak is more than 18 minutes, again allowing for a doubling of the service with the existing infrastructure. [There] is a proposal to add (back) 10 miles of third main track east of Framingham, further increasing capacity. Quandel’s numbers show [this project’s] cost to be $29.6 million. Allowing $1 million for each of the three station platforms that will have to be relocated brings the total to $32.6 million. As this railroad was once four tracks wide, it is no surprise that all four railroad bridges over roadways and all thirteen road bridges over the railroad can accommodate this additional track. I am adding $35.3 million to upgrade it to Class 5 (90mph), bringing the total cost here to $67.9 million

4. Large number of private at grade crossings between Springfield and Pittsfield

[There] are twelve; [at] $408,000 per crossing, the cost of protecting all twelve comes to less than $4.9 million.

”Significant grade and ROW constraints between Springfield and Pittsfield”, and “Steeper vertical grades and greater curvature reduce operating speeds through Leicester[sic]”

The negative effects of gradient can be mitigated by means of modern light weight equipment and high power locomotives. The lower power requirement of the very light Talgo sets currently in use on the Amtrak Cascades (Eugene Oregon – Vancouver, BC) corridor is currently saving time by enabling faster acceleration [and substantially reducing fuel costs, and GHG emissions]. On the ascending mountain grades of the MBTA route, [Talgo equipment] will result in significantly higher train speeds with no civil work needed.

5. Greater curvature affects rail speeds at several locations between Worcester and Springfield, […] and at several locations between Boston and Worcester.”

This problem can also be mitigated by equipment designed for that purpose. The Talgo sets in use in the Pacific Northwest have a suspension geometry that tilts the cars towards the low (inside) rail in a curve, reducing the lateral force experienced by passengers (and coffee cups, etc.). Conventional equipment will tilt in the opposite direction, magnifying that force. In addition, a low center of gravity allows Talgo equipment to operate safely through curves at higher speeds than can conventional cars. Because this 1830s vintage railroad alignment is highly curved this feature is very helpful and will eliminate the immediate need for expensive realignment of the railroad.

6. Long term capacity constraints at South Station

This service will require occasional use of one station track in Boston. The capacity issue at South Station already exists [though only during rush hour], and any solution can provide sufficient space for the new service at negligible incremental cost.

7. Rolling Stock

The necessary locomotives, passenger cars and maintenance facility were not specifically addressed at the February 6 meeting. The estimates presented there for each alternative did have a line for “vehicles + supporting facilities”. At $192.4 million for Alternative 2 and $206.7 million for Alternative 3, the numbers appear a bit low. I have estimated $87 million for a maintenance facility and $27 million for each train consist. Thus for Alternative 2, which requires three consists, the total is $168 million. I added an allowance for contingency and program management, bringing the total to $206.7 million, 7.4% above the consultant’s figure. Alternative 3 requires five consists making the total $273.0 million, 32% above what was presented at the February meeting.

8. Total Capital

Adding it all up, the cost of Alternative 2 is $385.0 million, 18% of that projected by consultants. Alternative 3 will cost $537.6 million, less than 17% of the projection.

9. Benefits

Under this low budget approach one might assume benefits would be significantly less than those produced by spending nearly $2 billion more (for Alternate 2) or in excess of $2.5 billion more (Alternate 3). To see what just a half billion would buy I ran a simulation of the proposed consist, a ten unit Talgo pulled by a Siemens Charger chosen to approximate the capacity and features of a Down Easter. The results are shown in this table – The talgo train with low-budget second track upgrade of the existing line is shown on the first line with the consultant’s proposed alternatives below:

Predicted Schedule Times (minutes)

Thus this proposal should save not only billions of dollars, but also nearly a half hour to (or from) Springfield compared to Alternative 2 and more than 20 minutes to Pittsfield compared to the even more expensive Alternative 3.

This remarkable result might produce some skepticism; however, the Talgo times are quite achievable. The simulation that generated these results included many conservative assumptions, some of which were:

Maximum speed is 80 mph (on track built and maintained for 90).

Schedule padding is included to reduce overall average speed by more than 5 mph.

The Siemens specified power is assumed to be at the main generator, with 85% available at the rail. Train resistance is given by the Davis equation, which is known to be conservative. Intermediate stops are made at Chester, Palmer, Worcester, Framingham and Back Bay.

Passenger load is always 100%. (Over 23 tons of “live” load)

Speed is reduced 264 ft. prior to all restrictions (due to PTC inefficiencies, which should ultimately be resolved)

Before power is applied to begin increasing speed out of any restriction, the rear of the train is 236 feet clear.

Average braking rate on level track is less than 2.2 mph/sec. (compared to the 3 mph/sec. normally achievable).

Where a grade change is unfavorable, its effect is immediate (as soon as the front of the train reaches it, the simulation assumes the entire train is on the new grade). If it is favorable no advantage is taken until nearly the entire train (all but the last 28 ft.) is on it.

Super-elevation (banking in curves) is limited to 5” on the passenger-only MBTA-owned track east of Framingham and to 4” (current practice) west of that point. (Six inches has long been the accepted maximum.)

Super-elevation of the numerous reverse curves is limited to an additional 0.5” above the current figure.

Cant deficiency is limited to 5” (compared to the 7.2” for which the Talgo equipment is designed).

Summary

We propose using available technology and modestly improved existing infrastructure to produce a better result (higher average speeds) at a much lower capital cost than that proposed by the consultants.

All that is needed is to:

- Restore the second main track and, for ten miles east of Framingham, one more track,

- Upgrade all track to FRA Class to 5 (90 mph),

- Increase super-elevation to 4 inches where needed (5 inches east of Framingham),

- Improve a few road crossings and

- Use tilting train sets with Siemens locomotives.

Excerpts reprinted with permission from the Rail Users’ Network and RUN Newsletter - Summer 2020 issue. If you enjoyed this article, and would like to see others, please consider becoming a member of the Rail Users’ Network, at

railusers.net

.

|

|

CP: GATHERS CMQ ASSETS AND OPERATIONS

|

|

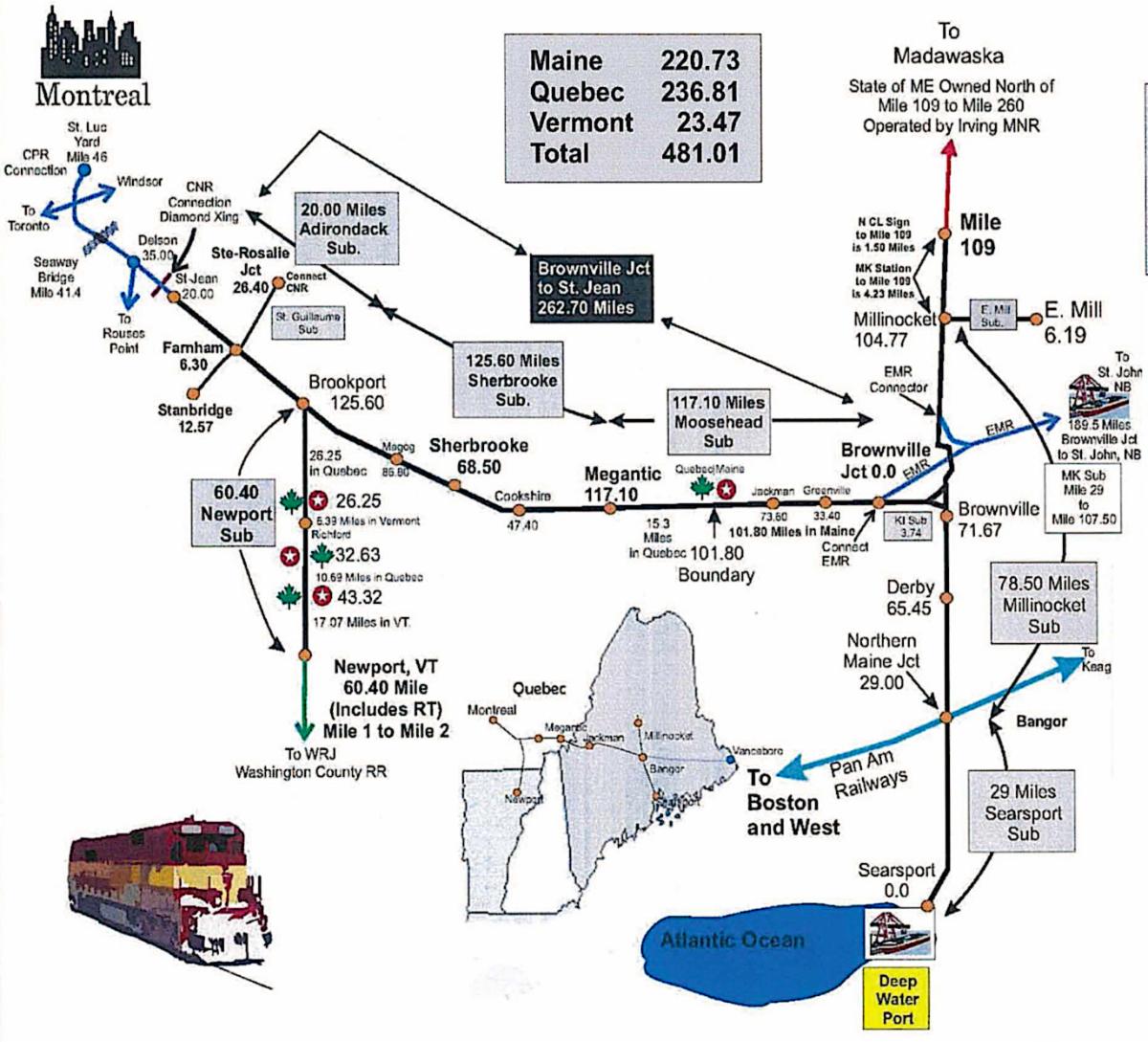

04 June, Bangor ME -

CP TAKES THE CAB AT CMQ, TOPPING 13,000 ROUTE MILES AND GETTING FIRST-EVER GLIMPSE OF SUNRISE OVER THE ATLANTIC. THIRTEEN NEW TRAINS ASSIGNED (BUT WHAT ABOUT A SEARSPORT LOCAL?). MOST CMQ HOURLY WORKERS RETAINED; MANAGEMENT GIVEN A ONE-WAY TICKET. SEARSPORT BRANCH TO BE UPGRADED FOR UNIT TRAINS.

by Kevin Burkholder, Associate Editor

Canadian Pacific completed its acquisition of the Central Maine & Quebec Railway US Inc. (CMQ US), 30 days after the Surface Transportation Board’s 04.May approval of CP’s Exemption for control of CMQUS's rail lines in Maine and Vermont.

Taking ownership of the CMQ’s 481 owned route-miles (Canada and U.S., combined) makes CP a 13,000-mile rail network, connecting the Atlantic, Pacific, and Gulf coasts across six Canadian provinces and 11 U.S. states. CMQ's enlarged network links CP to Port Saint John (PSJ) NB via EMR and NBSR connections, and directly to the Atlantic Ocean port of Searsport ME. CP plans to invest as much as

CA

$90 million over the next three years to bring CMQ's rail infrastructure up to Federal Railroad Administration Class 3 standards.

|

|

CP now controls the entire 481-mile CMQ network from St. Jean QC to Searsport ME,

as CMQUS's 244.2 miles of track rejoins CMQCA's 236.81 route-miles, which had been integrated with CP soon after the transaction was completed. In addition, CP assumes the lease on the 57.3-mile Rockland Branch, owned by the State of Maine. CMQ US and CMQ Canada will continue to operate in the U.S. and Canada, respectively, as subsidiaries of CP (

CMQUS is also considered subsidiary to CP’s U.S. Soo Line subsidiary - Ed.

). The acquisition agreement was struck in November.2019, for a reported

US

$130 million.

|

|

CMQ Jobs 1, 2, 400 pull out for good; CP 250 arrives

CMQ dispatched the last pair of road trains on its US trackage on Tuesday, 02.June, and a final Job 400 train round trip from Brownville Jct. to Millinocket, ME on 03.June. The return to Brownville Yard concluded the 28-year era of independent railroads operating on a line that CP relinquished in 1992.

|

|

Last CMQ-dispatched trains were all business

, with diverse, heavy loads.

Top:

Westbound CMQ Job 1 train at Harford Point ME, 02.June.2020. The two CMQ SD40-2Fs, 9022 and 9023, made that last westbound trip and were shut down at Farnham QC. The pair of CP GE AC44CWs trailing the CMQ power will be around for years to come.

Center:

Last eastbound CMQ Job 2 train at Long Pond, ME en route from Farnham to Brownville Jct. ME, 02.June.2020. Two leased CEFX AC44CWs 1006 and 1002 wearing CMQ paint lead, backed up by CMQ SD40-2F 9010, and leased CEFX GP38-3 3803.

Bottom:

The last train running on CMQ was Job 400 on 03.June.2020, here at Twin Lakes, Millinocket ME, returning to Brownville Jct. on the backhaul of a round-trip run.

{Steel Wheels Photography}

|

|

Orderly transition

At 0001 hrs on Thursday, 04.June, CP employed a six-hour transitional stand-down for inventory and dispatcher cutover, the latter planned to shift from the RailTerm offices in Rutland, VT to CP’s Minneapolis, MN offices under Soo Line oversight. However, civil disturbances in Minneapolis had temporarily closed the dispatch location, and CMQ instead would be dispatched from CP’s Battle Creek Yard (Saint Paul MN) backup dispatch “bunker,” until further notice.

At 0601 hrs, Canada-U.S. integrated operations resumed as a Soo Line/CP subsidiary. A new CP 250 train departed at Montreal QC to Brownville Jct. ME, and the counterpart CP 251 train returned (05.June), reasserting CP ownership and operation of its prodigal Atlantic region property, augmented by the thing CP has never had before — direct Atlantic Ocean access at Searsport, ME.

|

|

First CP 250-03

rolls over the East Outlet of the Kennebec River as fly fisherman work the water below {Steel Wheels Photography}.

|

|

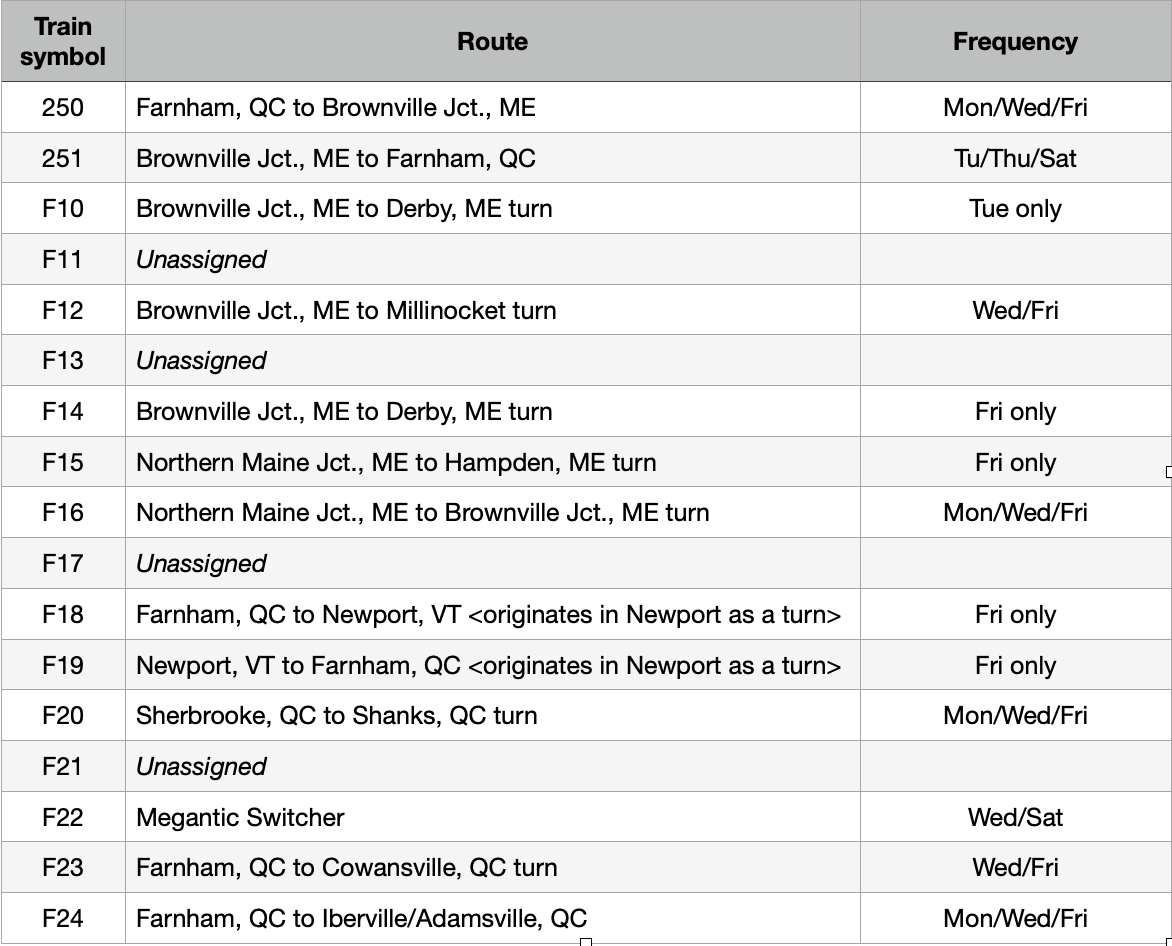

New CP/Soo/CMQ train schedule

|

|

Sunrise in Searsport

While CP is eyeing PSJ as a key terminal for autos, intermodal, and certain bulk commodities, Searsport will be developed to specialize in potash exports. PSJ has a potash terminal that is contracted exclusively to CN. Searsport will require additional upgrades to bring the plan to fruition. CMQ had tried for several years to maximize potash movement at Searsport, but had only minimal success.

In anticipation of carrying regular, longer trains, the Searsport Subdivision is being reinforced by a rail anchor program to manage the additional pressures of six-axle locomotives, which CP plans on using on any unit train operations to Searsport.

|

|

Searsport puts CP right on the Atlantic

for the first time. The Penobscot Bay commercial port has been a vital conduit for fuel and commodities to Central and Northern Maine and Eastern Quebec. Penobscot Bay Pilots and Fournier Brothers Towing have upgraded waterside capacity with highly capable vessels.

|

|

Most hourly employees retained; new management structure

CP will retain all of the CMQ US and Canada engineering and transportation hourly employees, as well as eight mechanical workers. CP will place the CMQ property workers under the CMQ US or CMQ Canada employee umbrellas. However the CMQ management structure and executive staff will not be joining CP.

Corporate-wise, an Assistant Superintendent will oversee the CMQ, reporting to the same Montreal office as the Delaware & Hudson. Reporting to the Asst. Supt. will be a General Manager, and train masters for US and Canada.

New opportunities already emerging

"This transaction is a generational business opportunity for CP," reiterated CP President and CEO Keith Creel. "It enables us to serve customers through a larger coast-to-coast network across Canada and brings a direct Class 1 freight-rail service to the State of Maine for the first time in decades. It is with great pride that I formally welcome CMQ's U.S. employees and customers to the CP family” {CP press release, 04.June.2020}.

Some new customers have already been won in anticipation of CP’s Atlantic reach. Creel mentioned to investors that they had been fulfilling new LPG business that originates and terminates in Maine on the CMQ. CMQ and CP had also won new Hyundai automotive business, though commencement has been delayed by the pandemic. Creel has also strongly implied that CP is hot on the trail of multiple other lucrative traffic opportunities {CP Investor Call}.

|

|

Word all around northern Maine

is that CP is planning to extend its 2020 US Holiday train to Bangor, ME, passing through other Maine locations on the CMQUS, including Jackman, Greenville, and Brownville Jct. While there is no definitive plan for that, it would be a great opportunity for CP to make its new the territory feel like part of the family

.

{Steel Wheels Photography}

|

|

|

|

Atlantic Northeast Rails & Ports

|

Corresponding on rail and port traffic throughout New England, the Hudson, Lehigh, and Delaware Valleys, the Canadian Maritimes, and eastern Quebec.

|

|

BCLR

- Bay Colony RR,

BLE

– Bessemer & Lake Erie (CN).

BM

– Boston & Maine

Corp.

CPA

– Connecticut Port Auth'ty

CBNS

- Cape Breton and Central Nova Scotia Ry, (GWI)

CCCR

- Cape Cod Central RR,

CLP

- Clarendon & Pittsford RR (VRS)

CMAQ

- congestion-mitigation or air quality (money from the US federal government for these purposes),

CMQ

– Central Maine & Quebec Ry,

CN

- Canadian National Ry,

CNZR

- Central New England RR,

ConnDOT

- Connecticut Department of Transportation,

CP

- Canadian Pacific Ry,

CSO

- Connecticut South’n RR, (GWI)

CSRX

- Conway Scenic RR,

CSX

- CSX Transportation,

EMRY

- see NBSR,

FHWA

- Federal Highway Admin.,

FRA

- Federal Rail Admin.,

FGLK

– Finger Lakes Ry. Co.,

FRTC

- Fore River Transp’on Co.,

FTA

- Federal Transit Admin,

GJRT

– Grand Jct. Running Track

GLX

- MBTA Green Line Extension project

GMR

– Green Mountain RR (VRS)

GU

- Grafton & Upton RR,

GWI

- Genesee & Wyoming Inc,

HRRC

- Housatonic RR,

IPH

– Iowa Pacific Holdings

ITHR

– Ithaca Central Railroad

JOC

– Journal of Commerce

JRAR

– Jones Runaround Ry

MassDOT

- Massachusetts Department of Transportation,

|

|

MBRX

- Milford-Bennington RR,

MBTA

- Mass. Bay Transportation Authority,

MC

- Massachusetts Coastal RR,

MCER

- Mass. Central RR,

MEC

– Maine Central RR (PAR),

MEDOT

- Maine Department of Transportation,

MMA

- Montréal, Maine & Atlantic Ry,

MNRY

- see NB&M,

MPO

- Metropolitan Planning Organization,

MTQ

- Québec Ministry of Transport,

NAUG

- Naugatuck RR,

NBDOT -

New Brunswick Department of Transportation,

NB&M

– New Brunswick & Maine Railways, system of

NBSR

- New Brunswick Southern Ry;

MNRC

- Maine Northern Ry; and

EMRY

- Eastern Maine Ry,

NECR*

- New England Central RR

NEGS

- New England Southern RR,

NET

– New England Transload

NHCR

- New Hampshire Central RR,

NHDOT

- NH Dept of Trans,

NHN

- NH Northcoast RR,

NNEPRA

- Northern New England Passenger Rail Authority,

NS

- Norfolk Southern Ry,

NSDOT

- Nova Scotia Department of Transportation,

NYA

- New York & Atlantic Ry,

NYNJ

- New York New Jersey Railroad (PANYNJ subsidiary,

formerly

Cross-Harbor),

NYSDOT

– NY State Dept. of Transportation

|

|

Pan Am

– refers to operator of PAS and PAR,

PAR -

Pan Am Railways - parent of MEC, PTM, BM, ST

PANYNJ

- Port Authority of New York and New Jersey,

PAS

- Pan Am Southern Railway,

PTM

– Portlsnd Terminal RR

PVRR

- Pioneer Valley RR,

PW*

- Providence & Worcester RR, (GWI)

QCR

- Quebec Central Ry,

RIDOT

- Rhode Island Dept. of Transportation,

RJC

– RJ Corman

Seaview -

Seaview Transport’n Co.,

SLQ*

- St. Lawrence & Atlantic Ry (Québec), (GWI)

SLR*

- St. Lawrence & Atlantic RR, (GWI)

SNC

– Saratoga & North Creek Ry,

ST

- Springfield Terminal Ry,

see

PAR,

TIRR -

Turner’s Island LLC,

TEU

- twenty-foot equivalent unit (measure of container traffic, equal to a 20x8x8 foot box),

UR

– United Rail, Inc.

USWX

– Waste Management, Inc.

VAOT

- Vermont Agency of Transportation,

VRS

-Vermont Rail System (Green Mt. RR Company,

comprised of

GMR, VTR, CLP, WAC

VTR

- Vermont Ry (VRS)

WACR

- Washington County RR (VRS)

WHRC

- Windsor and Hantsport Ry.

* These railroads are part of the GWI short-line holding company.

|

|

Atlantic Northeast Rails & Ports

Holden, MA 01520

(617) 877-5741

Joshua Davidson, publisher and editor

editor@railsandports.com www.railsandports.com

Coverage

The newsletter covers the operating freight railroads and ports in New England, the Maritimes, and eastern Québec, as well as the government environment they function within. Coverage includes passenger rail and ships when relevant to freight operations.

Copyright notice

All contents Copyright 2020 Joshua Davidson (and) Rails & Ports Media. All rights reserved.

PLEASE DO NOT COPY THIS NEWSLETTER, or forward it in e-mail format, in whole or in part. You receive it as a paying subscriber, or a potential subscriber. Passing it on without explicit permission of the editor violates copyright law, and diminishes the likelihood of our staying in business. However, anyone may quote bits of articles, with attribution, under the fair use doctrine. Notification required to share via social media, email, or print.

|

|

|

|

|

|

|