|

Happy New Year! Grains had an overall risk-off day today after a good end of the 2024 year. As mentioned in the midday text, there is a lot coming down the pipeline in January, between the upcoming USDA Report, the upcoming inauguration, and Brazil's looming harvest, the markets seem overall skiddish.

StoneX Brazil this morning raised their 2024/25 soybean production estimate from 166.2 to 171.4 mmt, due to increases in both planted area and yield; first-crop corn output also rose in both categories, with output there rising from 24.6 to 24.9 mmt. Second-crop corn production rose by about 100k tonnes this month to 101.6 MMT on higher plantings there; total corn output was up a bit over 300k tonnes from last month, to 128.6 MMT. 2024/25 soybean exports rose from 103 to 107 million tonnes.

This afternoon’s USDA November soybean crush is expected to come in at 207.2 million bushels, down from the record 215.8 mbu October total, but above 200.1 mbu last November. Estimates ranged from 204.3-210.5 mbu.

Estimated marketing year to date corn use for ethanol totals 1.773 billion bushels, down 28 million or 1.5% from the previous year's pace, but nearly 10 million bushels above the seasonal pace needed to hit USDA's newly revised target.

I was shared an article this morning that I thought has some interesting technical points. "Right now, March (CH25) corn is up +9.26% from August. The Usual/Average rebound is closer to +5%. The Biggest (recent) rebound was 2021. Post COVID Chinese buying with +65% increase. 2022 also saw significant increase – Russia/Ukraine (+24%). Take home? Prices are already up nearly 10% from August... unless something important and unexpected happens (possible!), I feel like upside potential might be somewhat limited above CH 4.60$bu. Ending stocks are lower from last year, demand is good, so price action is consistent with this context".

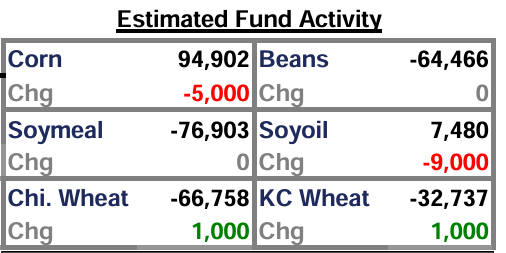

Funds were thought to have been mixed with corn a seller, wheat a buyer and soybeans neutral.

|